An Update After 4Q23 Gold Miner Earnings

Gold Moving Sideways

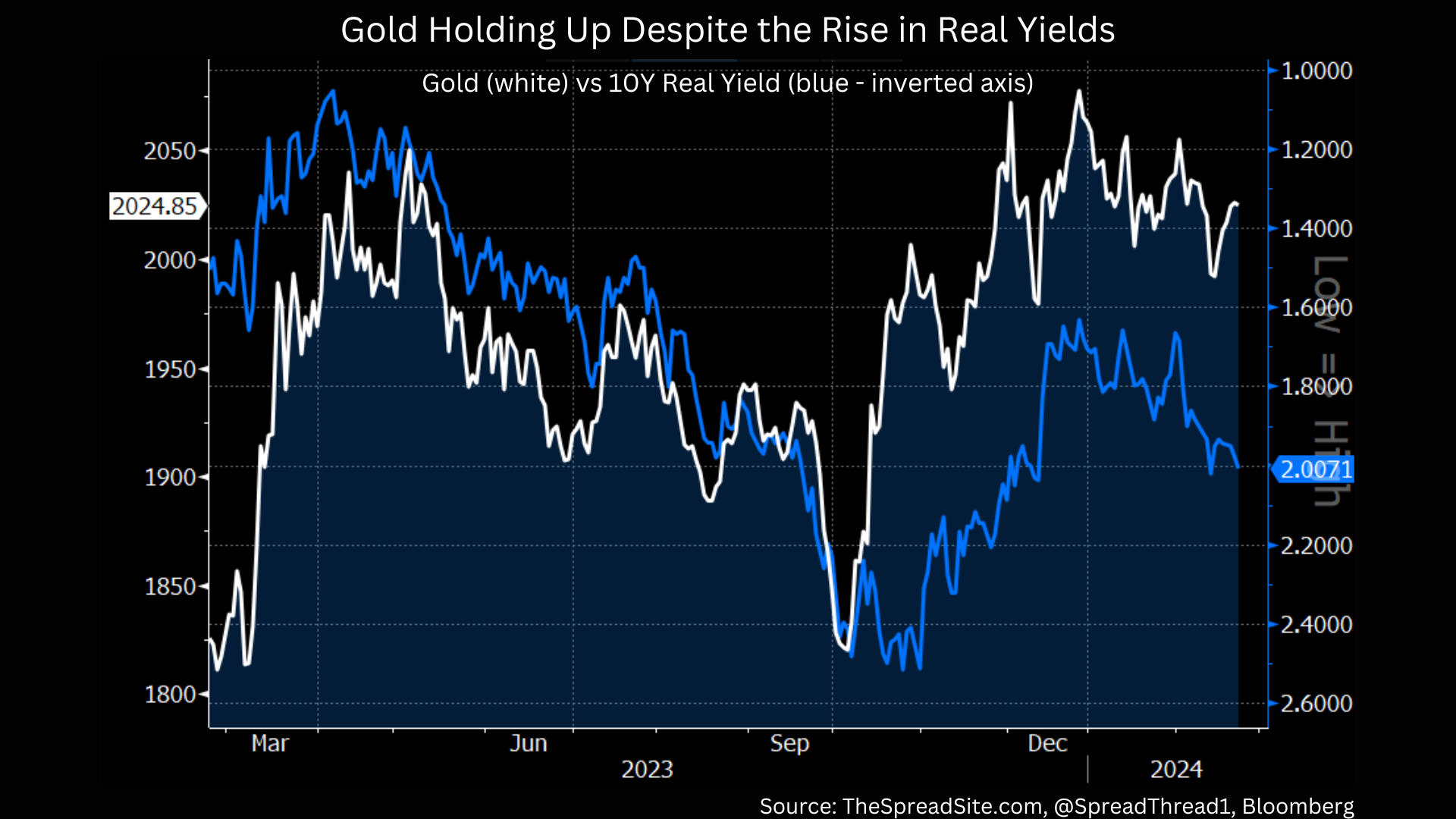

So far to start the year, gold has bounced around in a fairly tight range ($2000 - $2050). We are actually somewhat encouraged by the price action. First, over the same time period, 10Y real yields have risen by around 30bp. This selloff in bonds should have taken gold prices down more than it has, as we show in the chart below. Additionally, risk assets are melting up with ‘Goldilocks’ in full force, also a headwind for safe-havens. Yet, gold has managed to hold up, consolidating around $2,000, a level it has bumped up against multiple times over the past few years. We think the medium-term tailwinds for gold are still very much in place, and this resistance will eventually break.

The Bad

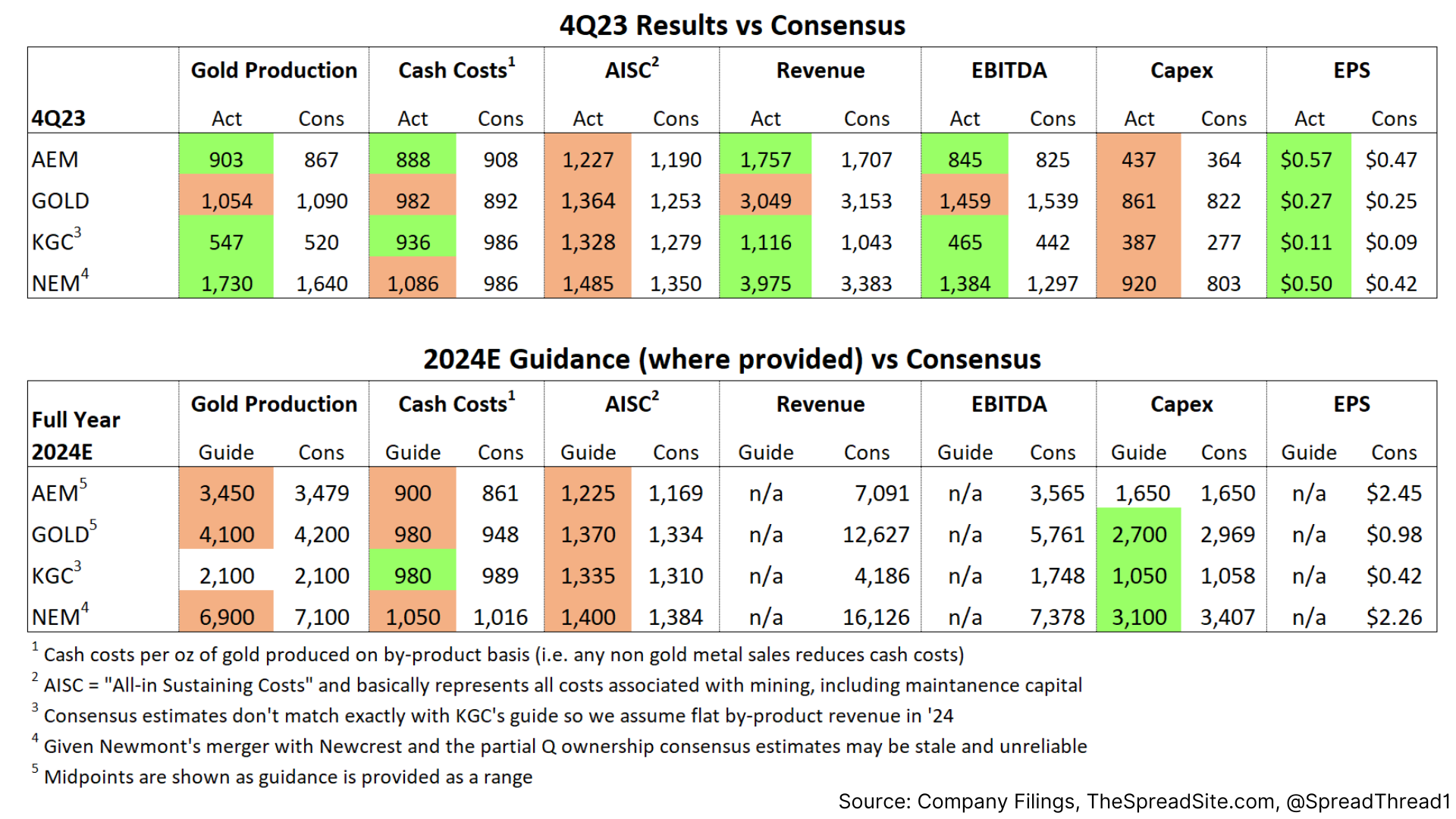

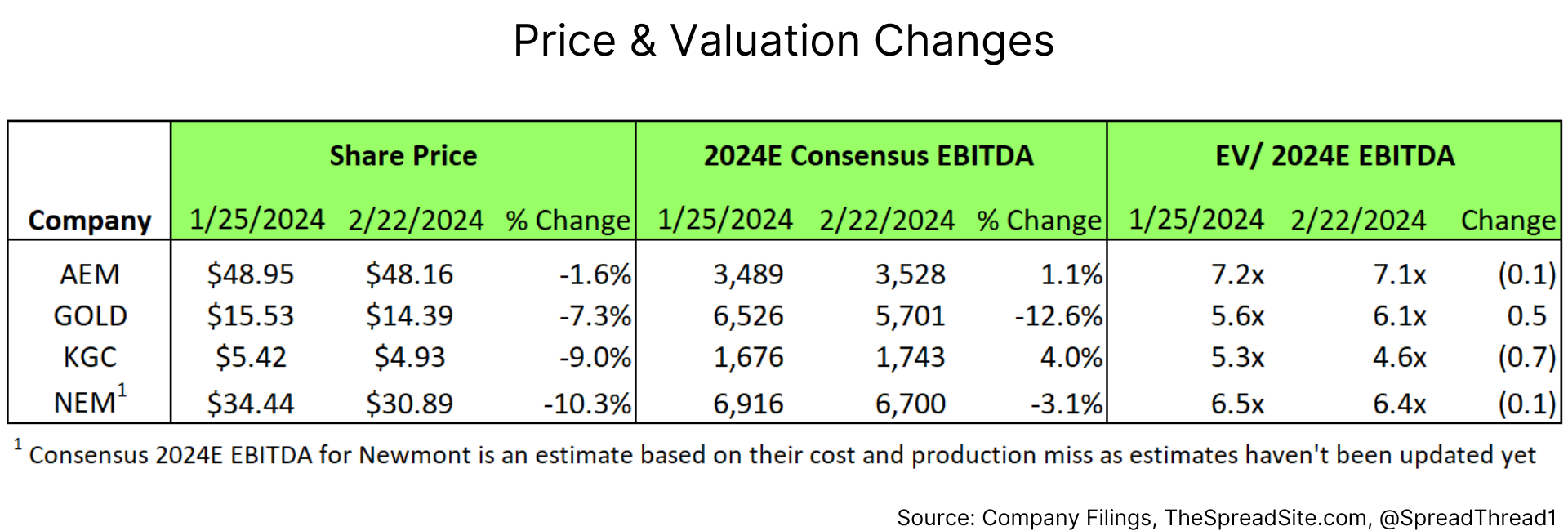

The 4 names we mentioned in our initial report “The Case for Gold Miners in 2024” are down an average of 7.1% since our publication on 1/25/24 (NEM -10.3%, GOLD -7.3%, AEM -1.6% and KGC -9.0%). We highlighted caution heading into 4Q earnings given a soft pre-announcement from Barrick and what was likely to be a very messy quarter out of Newmont (they did not disappoint).

Almost across the board, 2024 guidance for production and costs missed expectations but we think some of this was priced in approaching earnings.

The Good

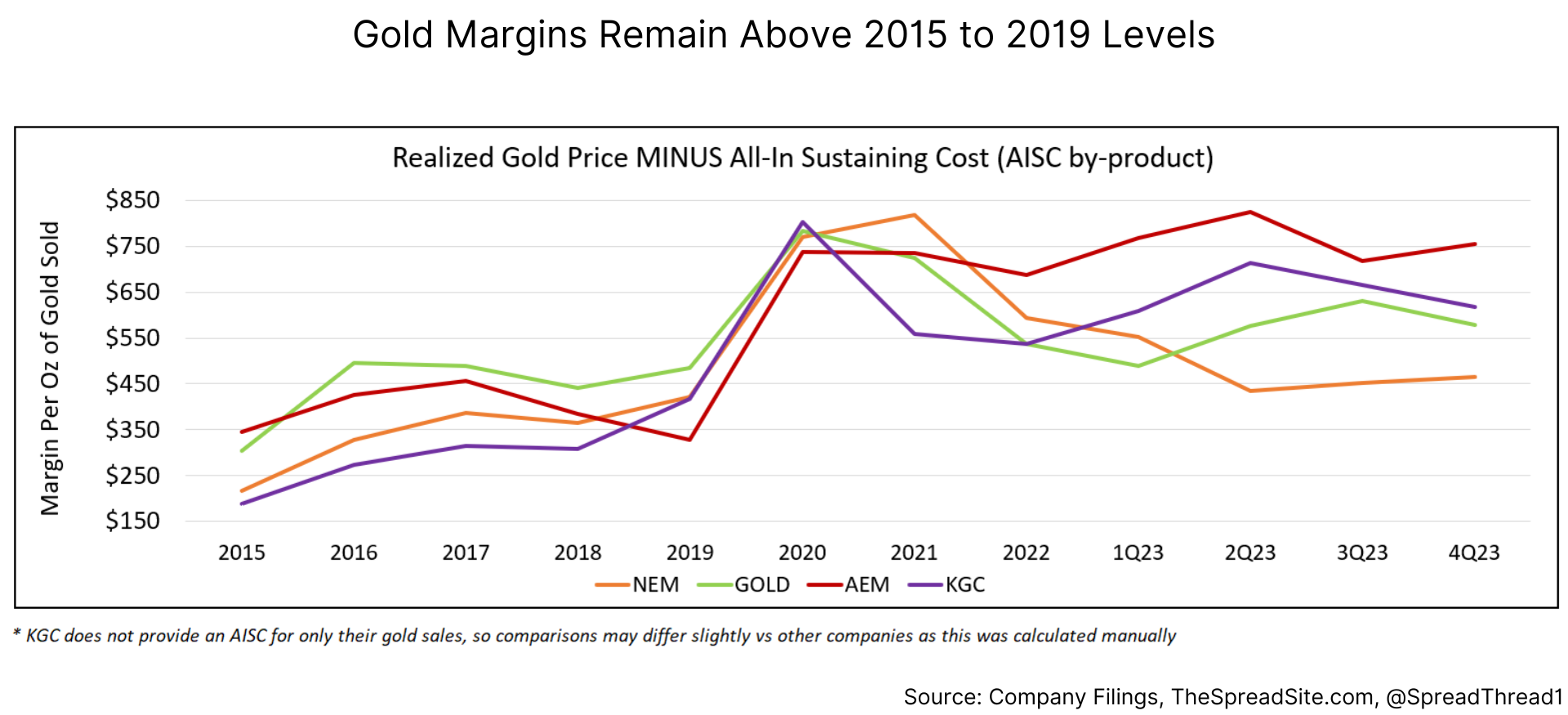

While 2024E AISC guidance did miss vs consensus, relative to 4Q23, costs are leveling out with labor remaining slightly higher, but energy expected to be slightly lower (AEM and KGC mentioned cost inflation of ~4% relative to 2023).

With revised consensus estimates (the reduction in consensus EBITDA for NEM is an estimate as they just reported), the equites are now cheaper than on 1/25 (GOLD being the exception), although margins will be lower given cost guidance higher than consensus.

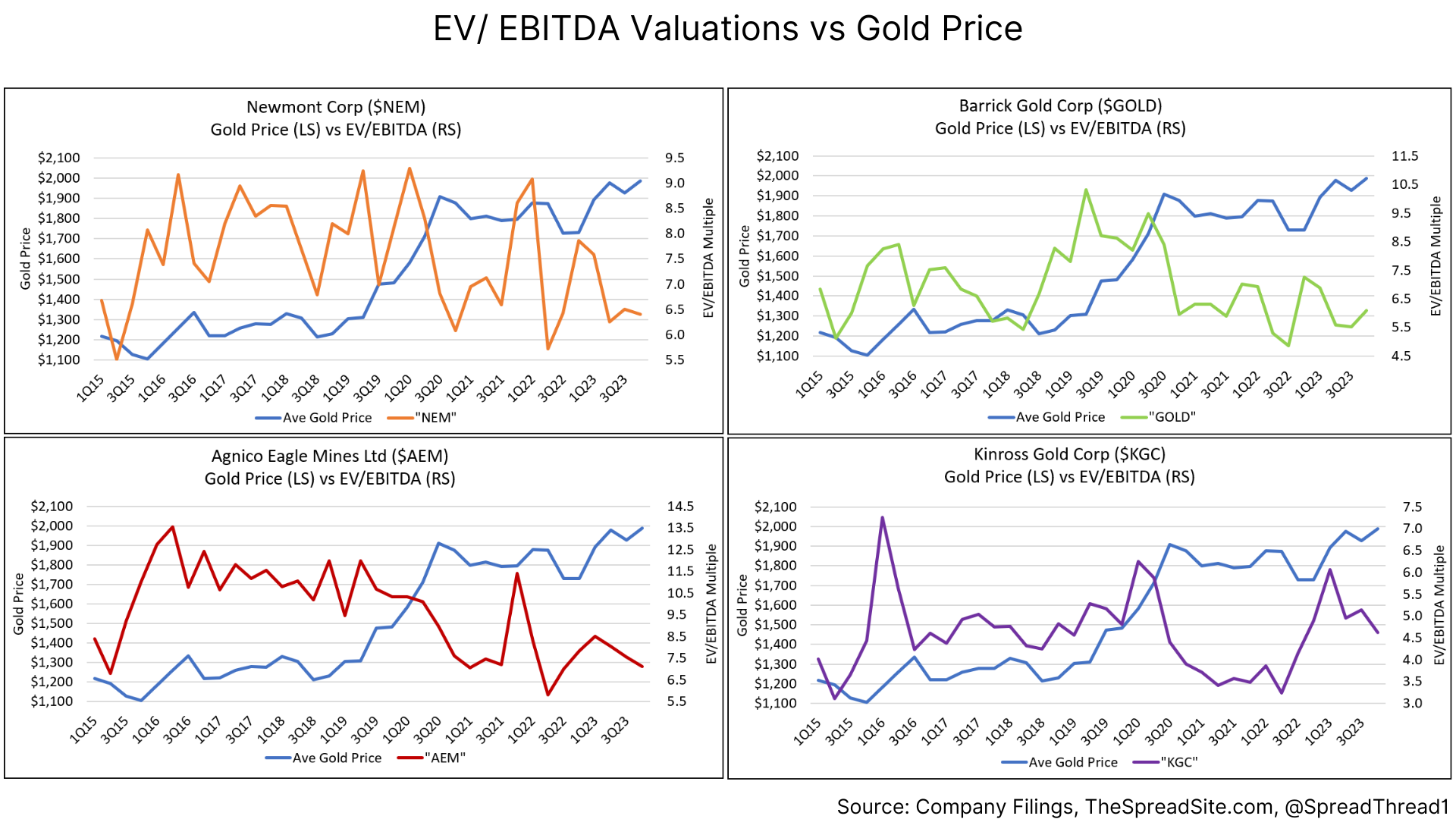

After weak 4Q23 earnings we are sticking with our call. If cost inflation continues slowing (or flatlines) and gold rises, we believe these names offer asymmetric upside given a starting point of historically low valuations.

As already described, these are not companies you want to hold long-term, but post 4Q23, we believe our initial thesis holds. We like doing this trade as a basket, equally weighted across all 4, as they all have different advantages and disadvantages.

4Q23 Conference Call Notes

Lastly, we included a few comments from each company from their respective earnings calls.

Disclosures

Please click here to see our standard legal disclosures.

The Spread Site Research

Receive our latest publications directly to your inbox. Its Free!.

{kind=link}