Part 1: Midstream Energy

Summary

- Comparing equity yields in midstream energy with fixed income can be challenging given its added risk and growth components. Metrics such as dividend yield and free cash flow yield do not provide a full picture and we walk through two approaches for analyzing yield.

- The midstream sector is often viewed negatively by investors given a history of highly complex structures, extreme price volatility and high betas to energy. However, names with large and diverse portfolios, highly contracted cash flows and improving fundamentals are becoming more bond-like, in our view, which should cause valuations to rise and volatility to decline.

- We highlight 6 names offering attractive spreads and valuations relative to history where 11-12% total returns appear reasonable.

Introduction

Our goal in this multi-part series is to create a framework for analyzing equity sectors with a significant yield component to compare relative value across asset classes. Comparing equity yields to bond yields can be challenging given the added risk of being at the bottom of the capital structure plus the variability of yield growth. Often dividend yield is used, but this metric is flawed as companies can choose how much free cash to payout and consequently does not incorporate risk and/or growth.

Midstream energy is the first sector in our series and arguably the most difficult. Traditionally, these companies were structured as Master Limited Partnerships (“MLPs”), which carried a tax advantage for investors and the MLP but required the dreaded K1 paperwork. Many have converted to C Corporations which appeal to a broader investor set.

There is tremendous nuance within midstream energy companies and the focus here is on the largest, most diversified names with limited commodity exposure. We think these names are the most “bond-like” and while there may be more upside in companies focused on specific basins or carrying more commodity exposure, we view those situations as more “equity-like.”

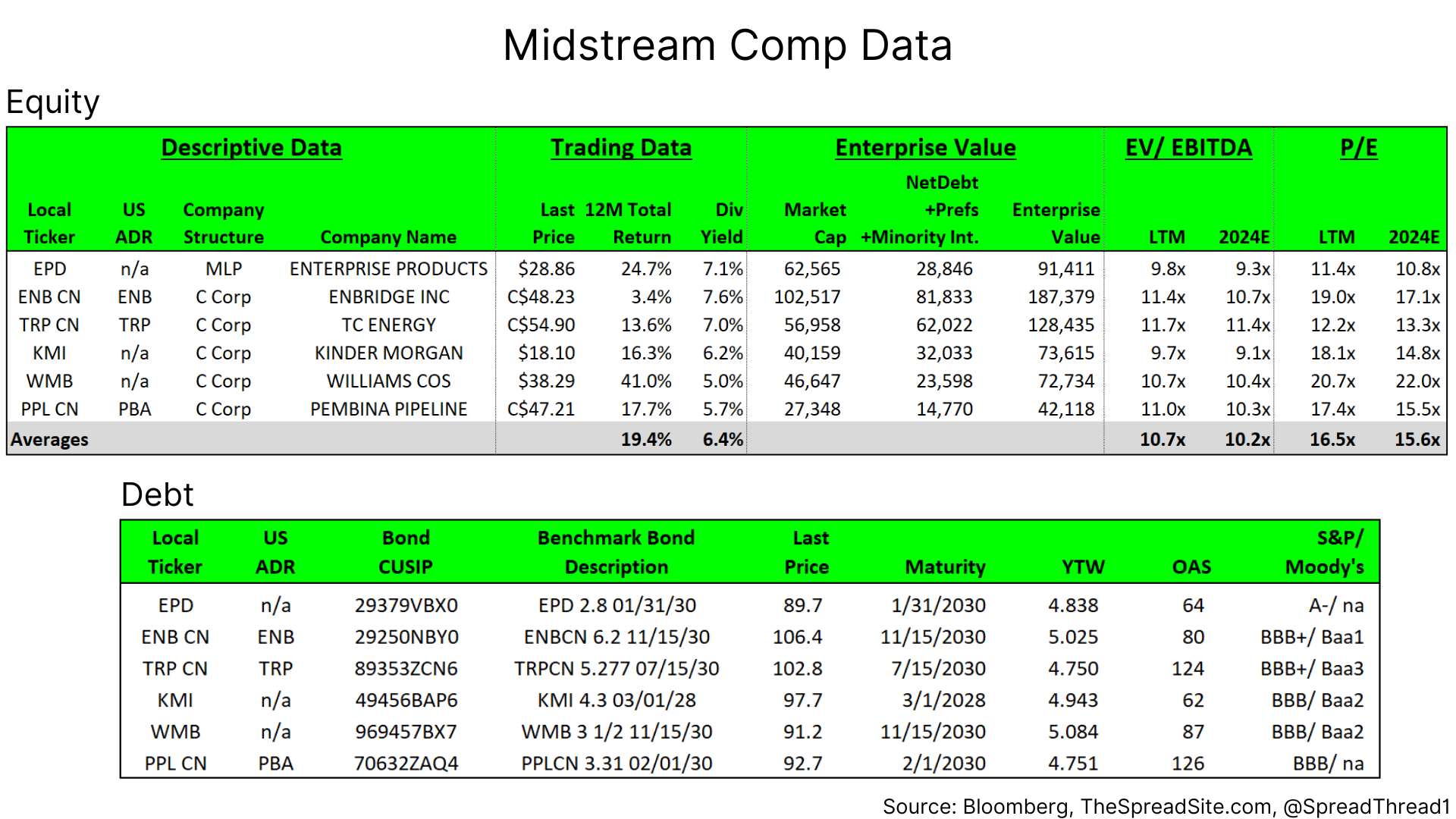

The 6 names discussed include; Enterprise Products (“EPD”), Enbridge (“ENB CN” | “ENB”), TC Energy (“TRP CN” | “TRP”), Kinder Morgan (“KMI”), Williams (“WMB”), and Pembina Pipeline (“PPL CN” | “PBA”) and offer favorable total returns relative to Treasuries ("USTs") and High Hield ("HY"), in our view.

Midstream Background

Historically, midstream companies could be viewed as complex and risky investments with skewed incentives between investors and management.

With respect to complexity, they faced three main issues:

- The MLP Structure: This offers favorable tax treatment as the businesses does not pay corporate tax, and cash flow to investors is not taxed until the investment is sold. EPD is the only MLP we discuss so we won’t go into detail, but for more information on tax consequences the article found here is helpful

- Incentive Distribution Rights (“IDRs”): None of the companies we discuss have this structure, but generally it incentivizes an MLP to grow its cash flow in order to receive a “split” of up to 50% (in other words, as the MLP grows, investors get less of the cash flow).

- Multiple Company Holdings: MLPs could own equity stakes in other MLPs making them very difficult to analyze in terms of pro-rata debt and cash flow.

Since the energy meltdown in 2014 there has been a trend of MLPs becoming more investor friendly by reducing complexity, converting to C Corps, eliminating IDRs and focusing on stable, fee-based cash flows. We think this trend continues and will reduce equity volatility while raising valuation multiples.

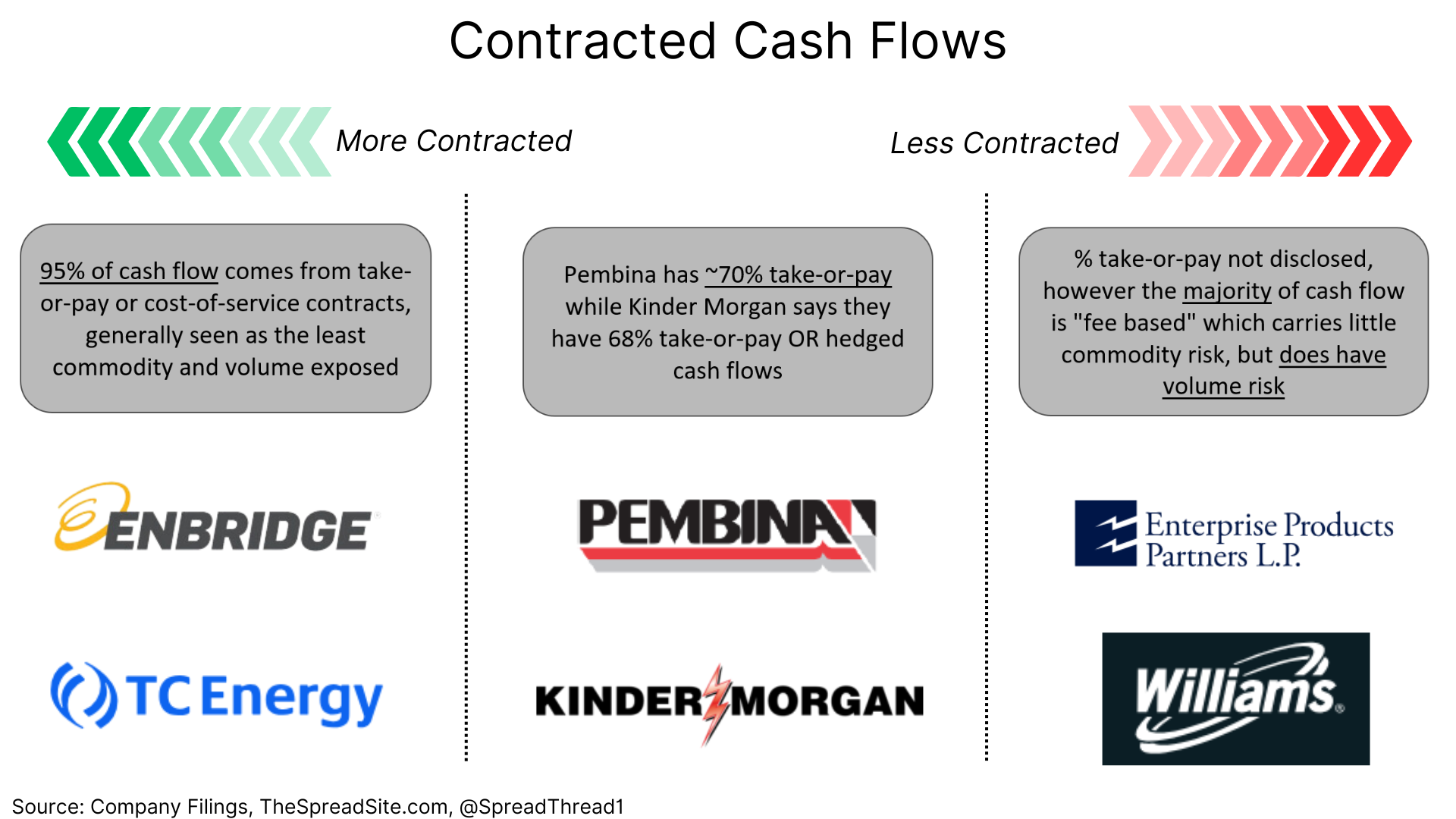

Midstream contracts & cash flows can vary in addition to asset types owned. Some of the broad categories are as follows (in order of least to most commodity exposed):

Contract Types & Commodity Exposure:

- Take-or-Pay: The asset owner contracts with the customer for a specific amount of usage and gets paid regardless of commodity price over the life of the contract. There is essentially zero commodity risk here.

- Cost of Service: More common in regulated pipelines whereby the owner charges a cost of service plus a regulated return to the customer. There is no commodity price risk but there may be some volume risk.

- Fee-Based: The asset owner charges a fixed fee (or set within a range) for volume used by the customer. There is usually low or no commodity price risk but there is likely to be volume risk.

- Percent of Proceeds: Specifics can vary, but generally this is where the asset owner can get paid in-kind as hydrocarbons are shipped on their asset. There is commodity price and volume risk under this agreement.

Midstream companies have discretion in how they describe their level of contracted cash flows, specifically in the “fee-based” category where actual commodity exposure can be understated. The 6 companies highlighted in this report have limited commodity exposure relative to the broad midstream sector and can be bucketed as follows:

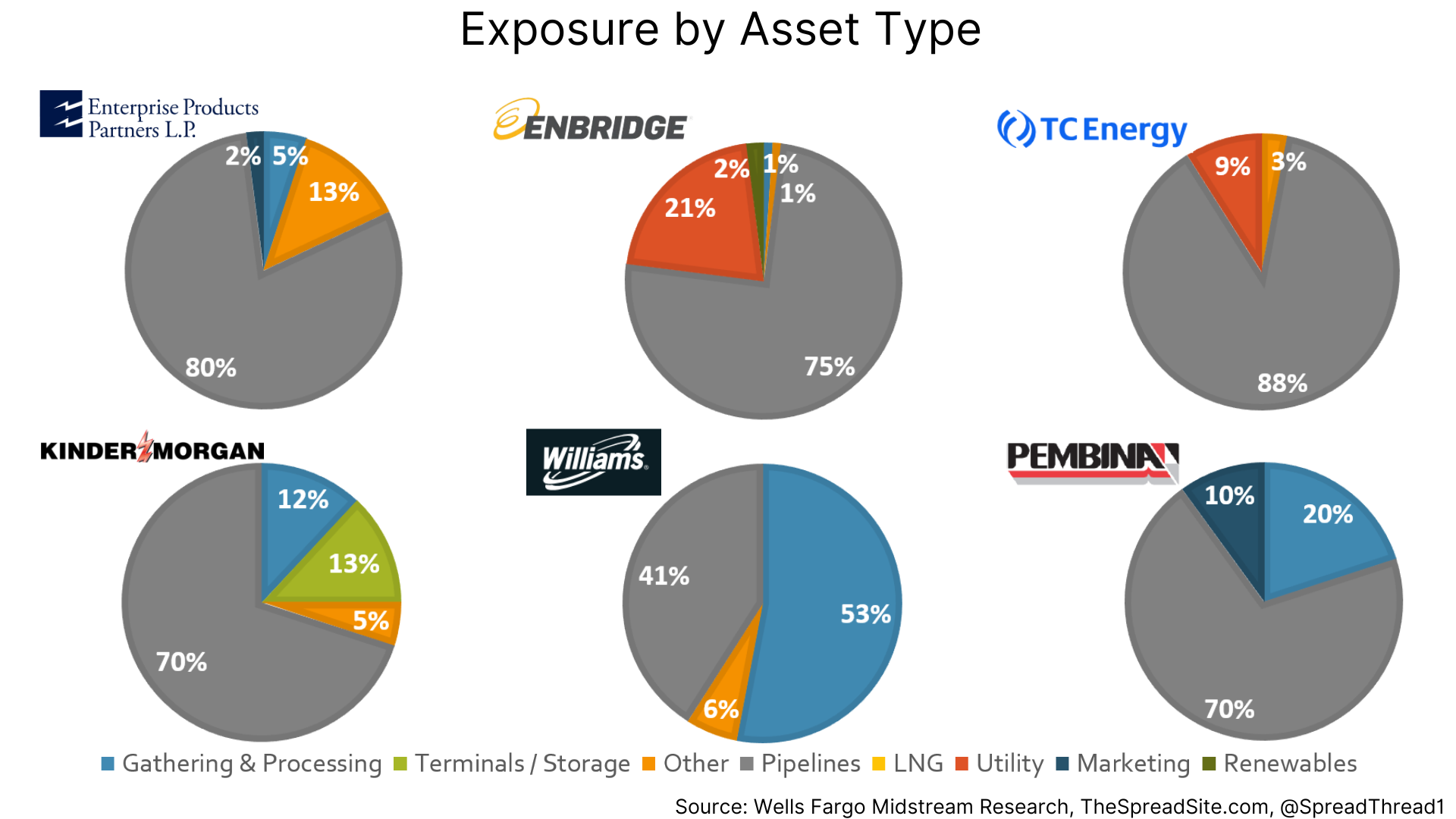

Many different asset types are lumped in as midstream, but generally the business serves as the middle man between exploration and production companies pulling hydrocarbons from the ground and end users.

Common Asset Types:

- Pipelines: This can refer to long-haul interstate pipelines regulated by the Federal Energy Regulatory Commission (“FERC”) or intrastate pipelines that may face more competition. Pipelines are generally used for one product type (i.e. an oil pipeline or a natural gas pipeline).

- Gathering & Processing: Assets generally used to gather and process hydrocarbons at one or many oil fields and process them before being shipped for end use.

- Terminals & Storage: Facilities that can be viewed as a bridge or middle man between the upstream production and downstream consumption of hydrocarbons.

- Marketing: Generally, this refers to the purchase and sale of hydrocarbons flowing through the midstream company’s system with varying fee or margin potential.

- Utility: This category would refer to assets with a regulated return.

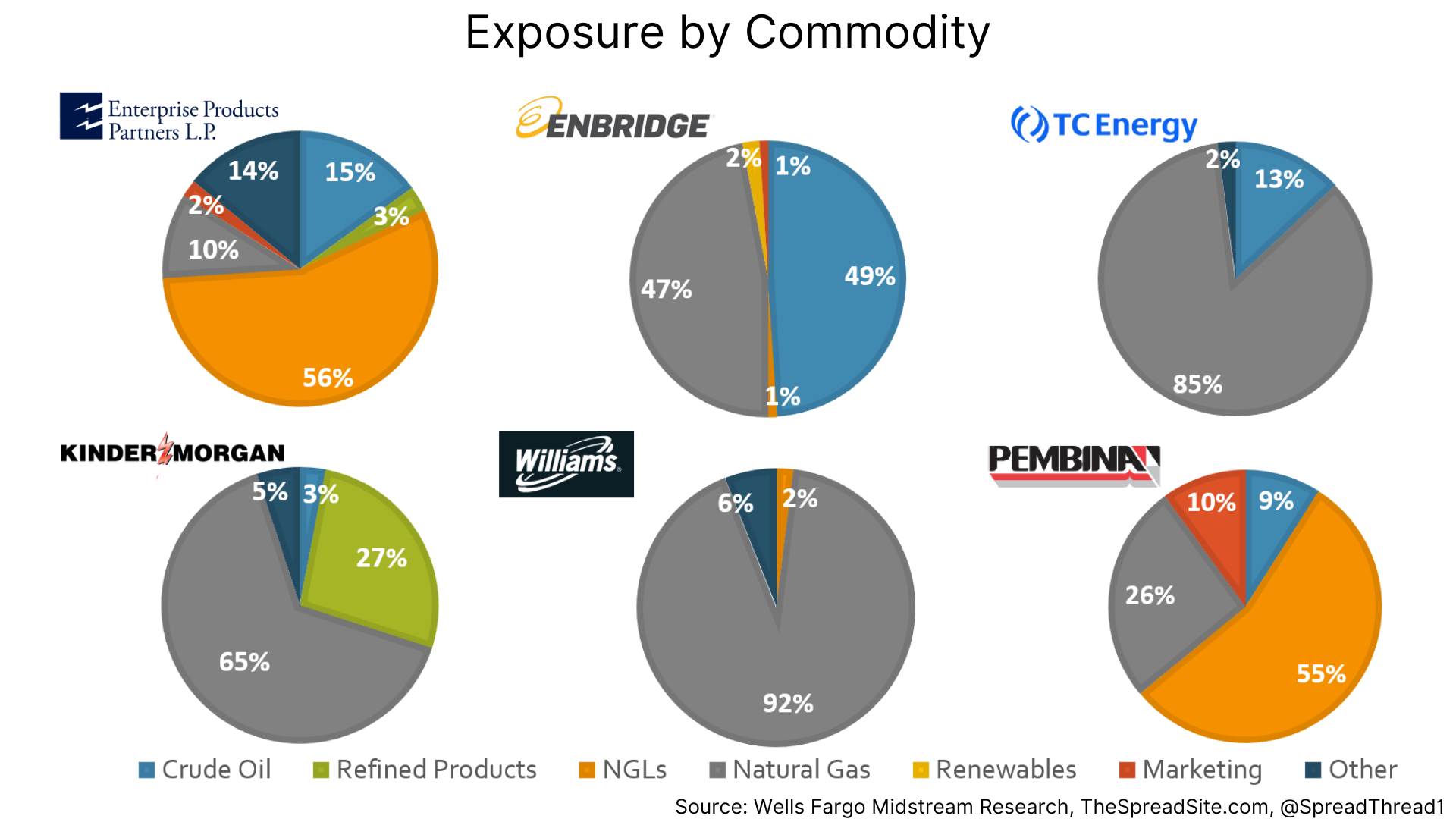

The pie charts below show each companies' exposure by asset type with pipelines being the largest overall category (gray slices).

Regarding commodity exposure, natural gas (gray slices) is the largest piece. In our view, this is relevant as natural gas is hovering at 52w lows of around $1.66/MMBTU, yet ’23 and ‘24E cash flows remain robust.

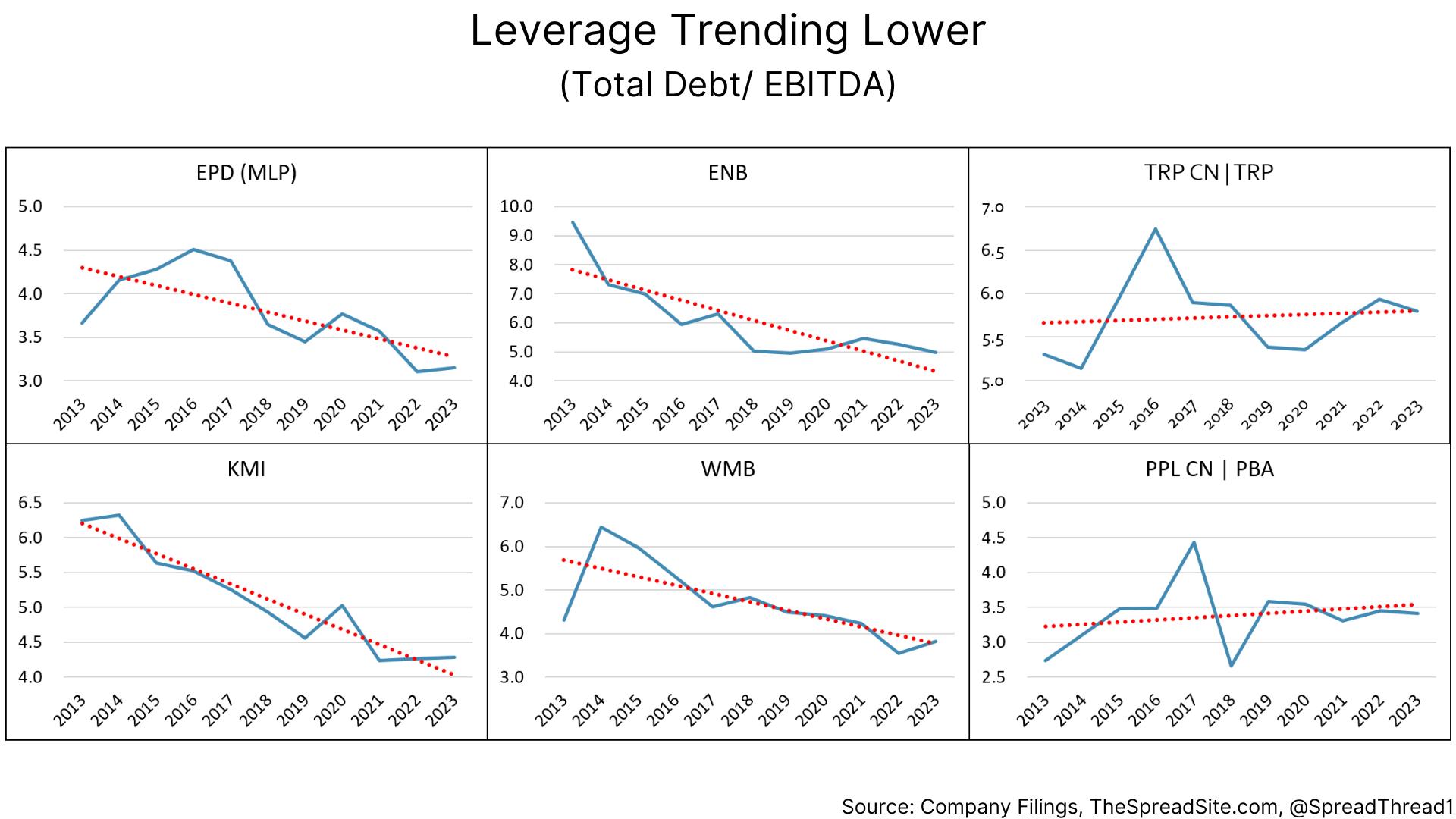

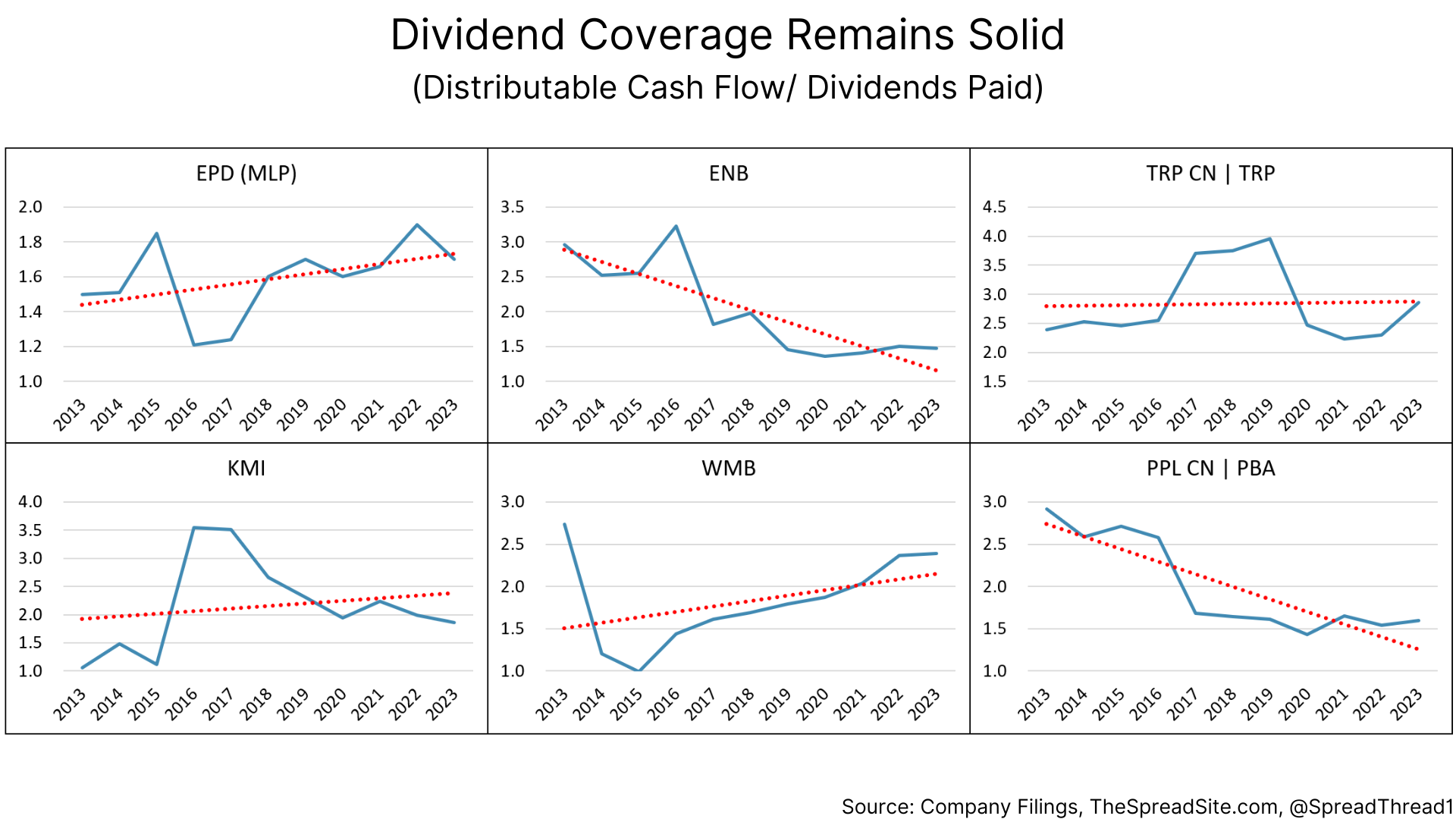

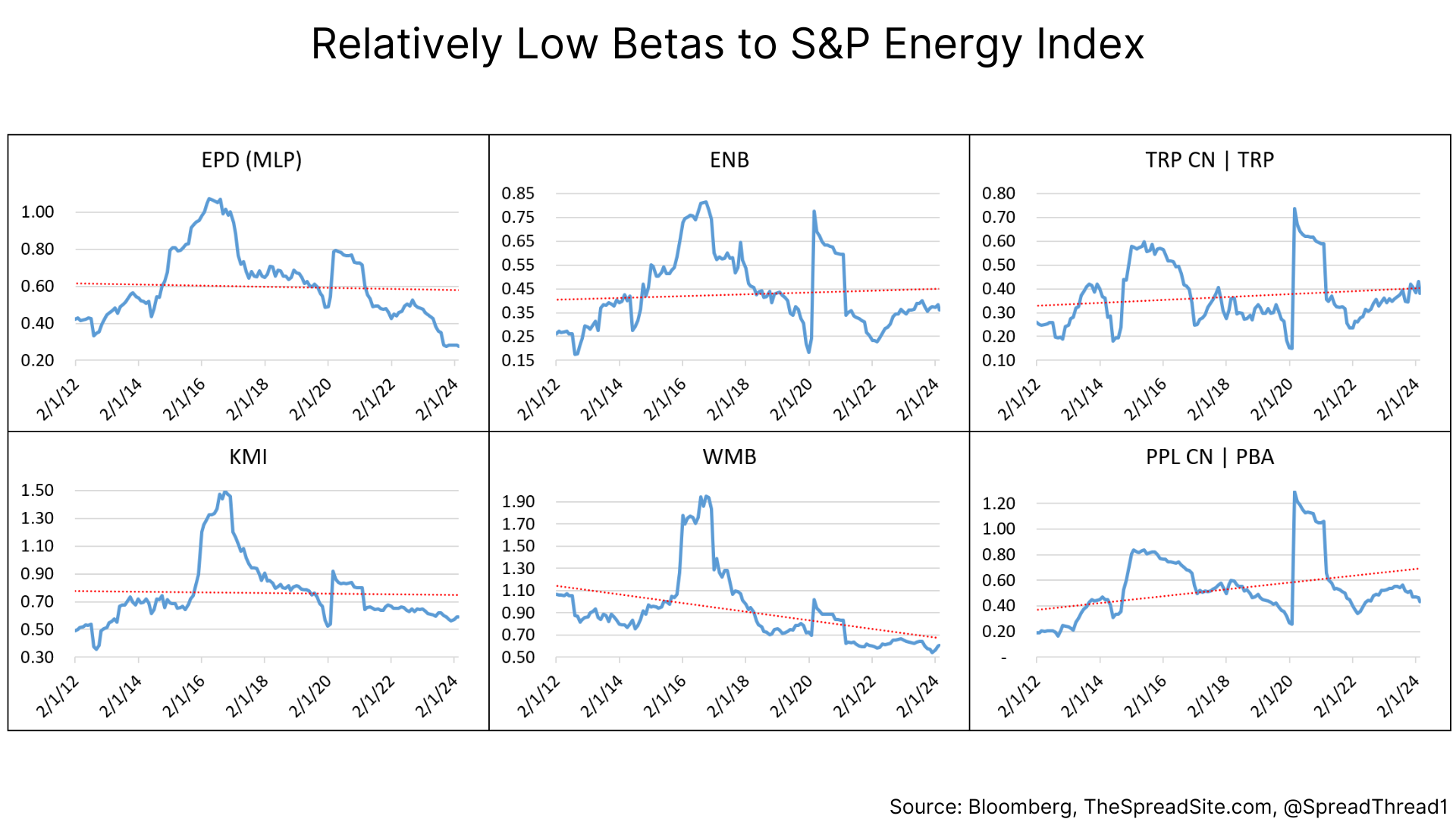

Historical Perspective in Chart Form

Investors may have a distaste for midstream companies given a history of high valuations, complex structures and the extreme price volatility seen during 2014’s energy meltdown and more recently, COVID.

However, not all midstream businesses are equal with some carrying significantly higher business risk and sensitivity to commodity prices.

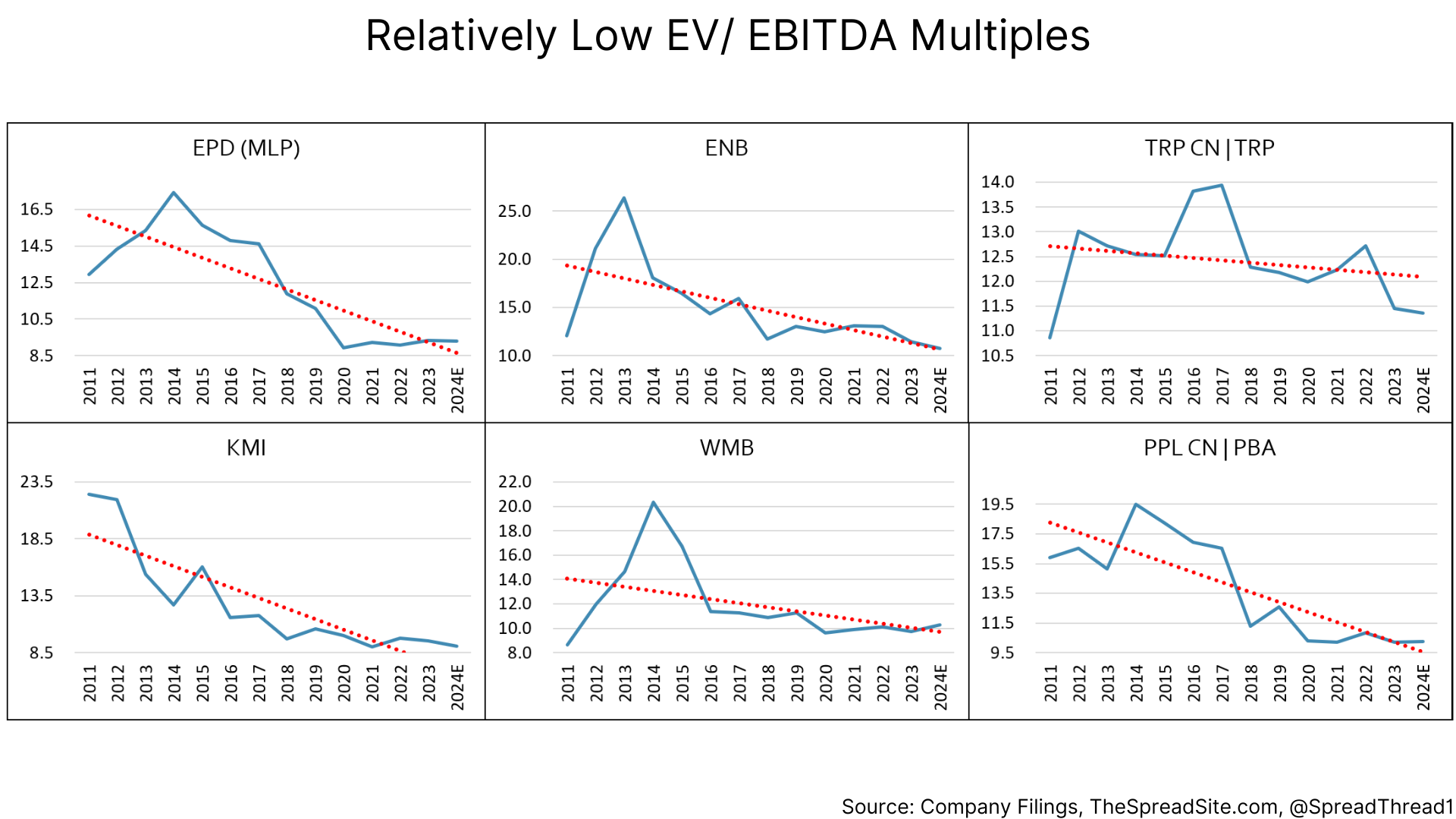

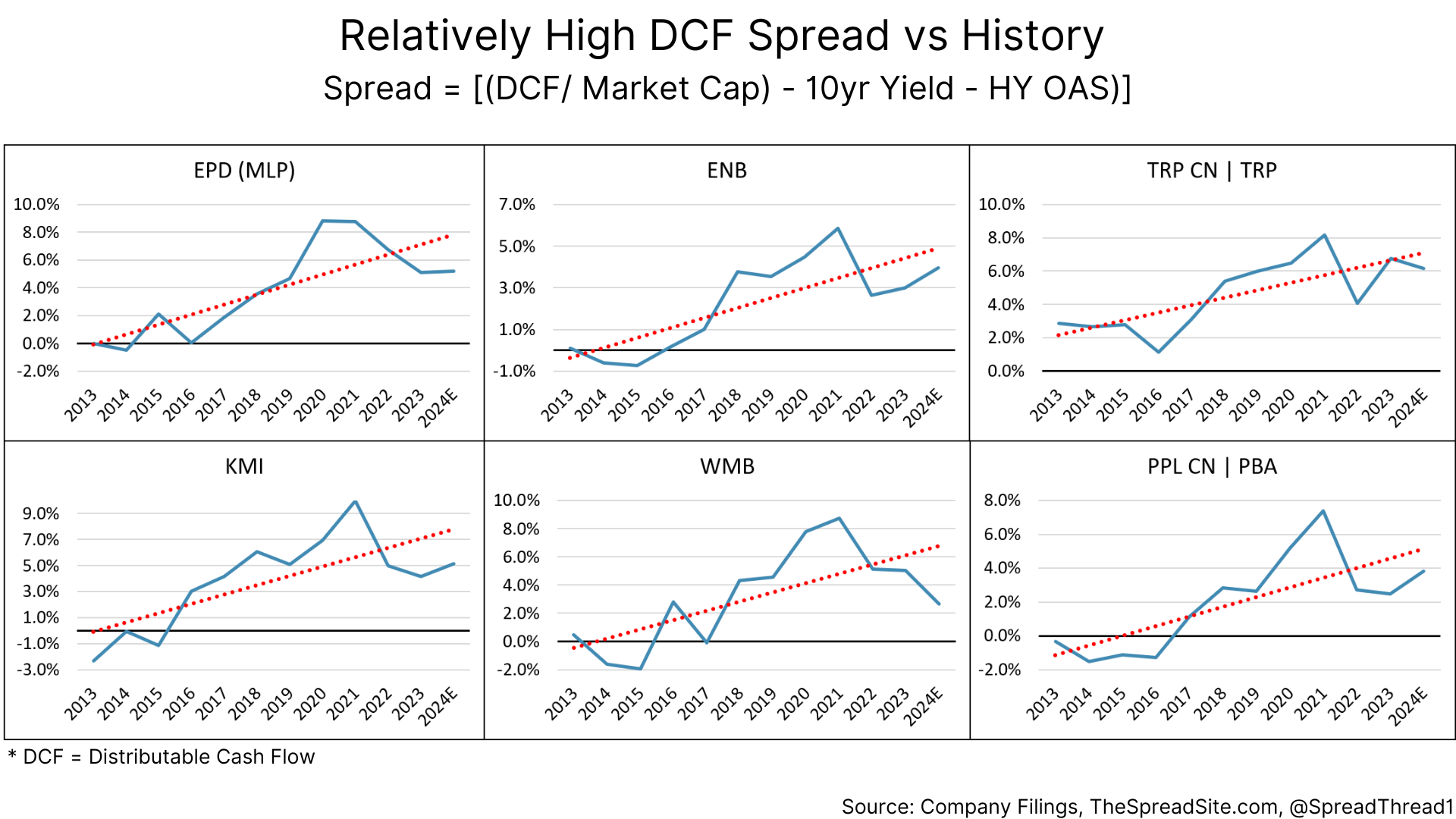

As we show in the charts below, the aforementioned midstream companies have investment grade balance sheets, relatively high contracted cash flows and reasonable valuations. In our view, they are becoming more bond-like and should continue to have declining (but not zero) sensitivity to the overall energy sector.

Midstream Yield

Yield for equities can be thought of in multiple ways including dividend yield, free cash flow yield etc., but for midstream companies, our preferred focus is to start with Distributable Cash Flow and discuss why below.

Standard metrics such as dividend yield or free cash flow yield can be incomplete proxies for yield. With dividend yield, companies can choose how much of their free cash flow to payout as dividends making this an incomplete measure for yield. Free cash flow yield has issues as large capex projects can understate free cash flow but carry a significant growth component in outer years.

Starting with Distributable Cash Flow (“DCF”) we can use two approaches to analyze yield and form a total return estimate. Generally, DCF is defined as:

Adjusted EBITDA

+/- adjustments for non-controlling interests

-cash interest (including preferred dividends)

-maintenance capex

-taxes (if applicable)

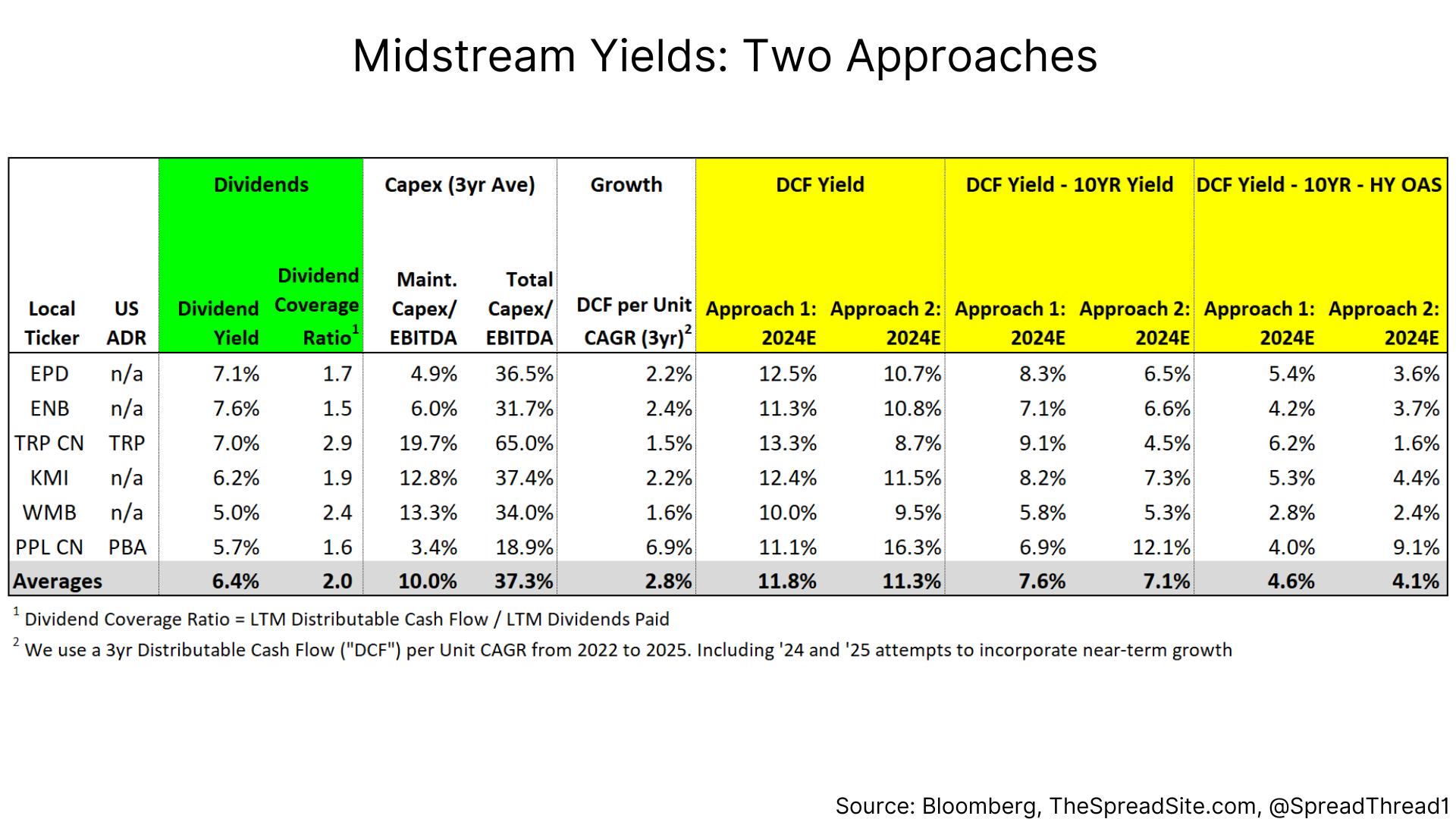

Approach 1 (steady state) uses DCF as defined above and divides by market cap (or DCF/shr divided by stock price) to get a DCF yield. However, a key point is that DCF uses "maintenance capex" which is a company estimate and only includes the capital required to maintain operations. Therefore, a DCF yield assumes a steady-state situation without incorporating growth or a decline rate (some view midstream businesses as having a finite life with Morgan Stanley estimating this metric at ~22 years). Regardless, we can look at DCF yields relative to a 10yr yield and HY spreads, which are shown in table below.

Approach 2 (growth) uses DCF as a starting point, but includes the total capex instead of maintenance capex (3yr ave) and adds a growth CAGR (i.e. [DCF – total capex + growth]. Using a 3yr DCF/share CAGR from 2022 through 2025 is reasonable, in our view, to incorporate recent capex spend and the near-term expected growth. However, there can mismatches between growth estimates and capital outlays if a company is embarking on a very large growth project.

The yellow section in the table shows the outputs for each approach while also comparing as a spread to current 10yr yields and HY spreads. In aggregate, each approach is similar while Approach 2 shows more variation by company as growth projects can be lumpy.

Dividend yield and payout ratios are also shown (green section) as they remain important metrics for investors to approximate current yield regardless of their inherent flaws.

In our view, looking at spreads relative to HY is more appropriate than comparing to IG even though the companies have IG credit ratings as we are analyzing equity yields which have added risk from being at the bottom of the capital structure.

In short, we think high quality and diversified midstream companies are attractive given total return potential of ~11-12% (DCF Yield), wide spreads and lower valuations relative to history. Additionally, as we showed above, we believe their structures have gotten less risky over time, which should lead to tighter spreads and lower yields.

Conclusion

Simply looking at dividend yield or free cash flow yield provides an incomplete view of yields in midstream energy. By looking at DCF yields using the standard maintenance capex or using total capex plus a growth CAGR, investors can better approximate total returns. After all, DCF approximates the cash flow available for any combination of dividends, share buybacks or growth.

Commodity prices and overall hydrocarbon use remains a risk, but all businesses face uncertainty far into the future. The added spread relative to other fixed income products and relative to history compensates for this risk, in our view. Further, as the 6 companies mentioned in this report continue to become more shareholder friendly we think valuations are likely to trend higher.

Disclosures

Please click here to see our standard legal disclosures.

The Spread Site Research

Receive our latest publications directly to your inbox. Its Free!.

{kind=link}