Credit Check

Credit markets have rallied aggressively so far this year, along with most risk assets, continuing the bull market that begin in late 2022. In this week’s note we provide a brief update on corporate credit and a few thoughts looking forward.

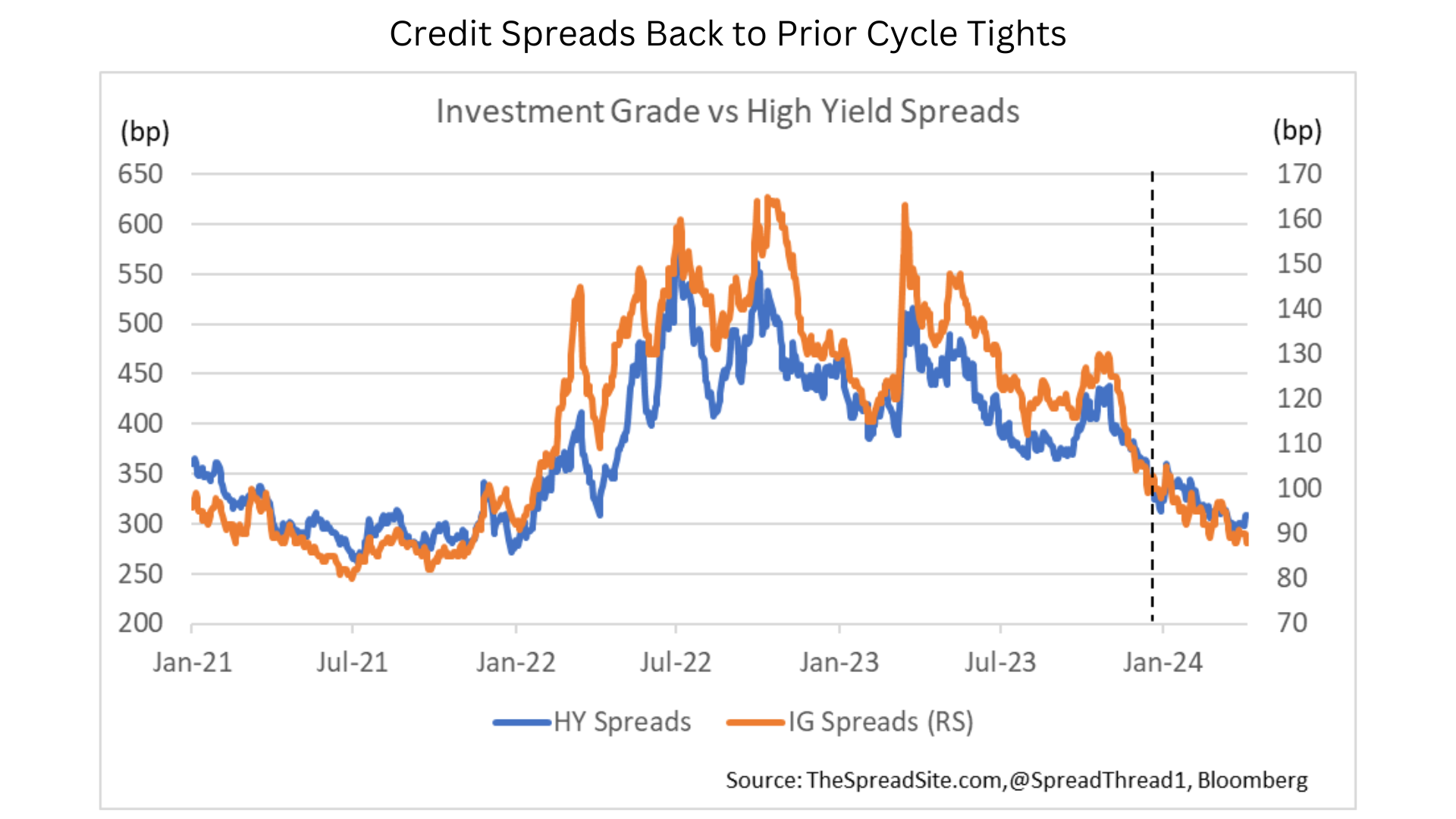

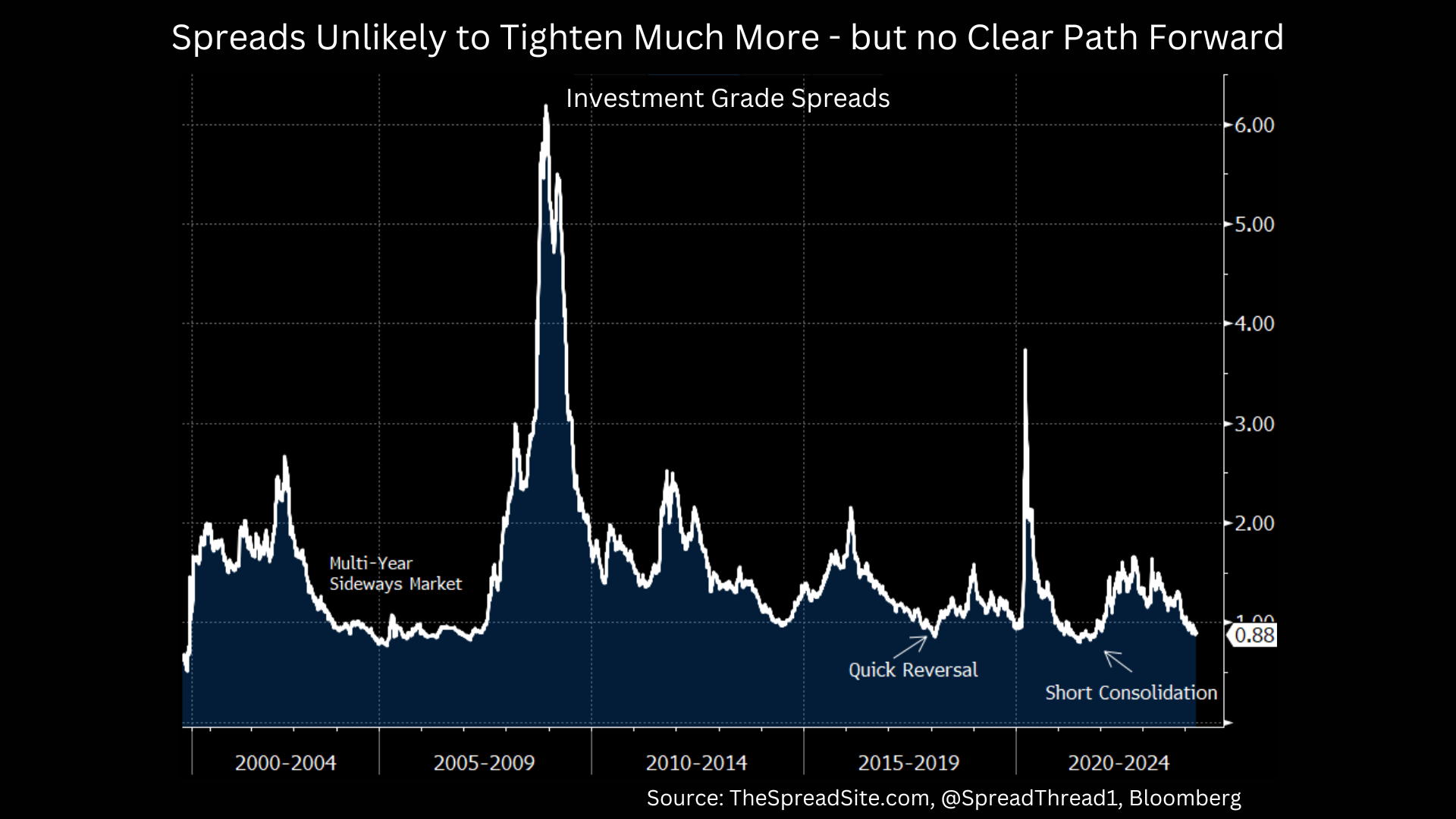

First, both investment grade and high yield credit spreads have now round-tripped, hitting levels last seen in early 2022.

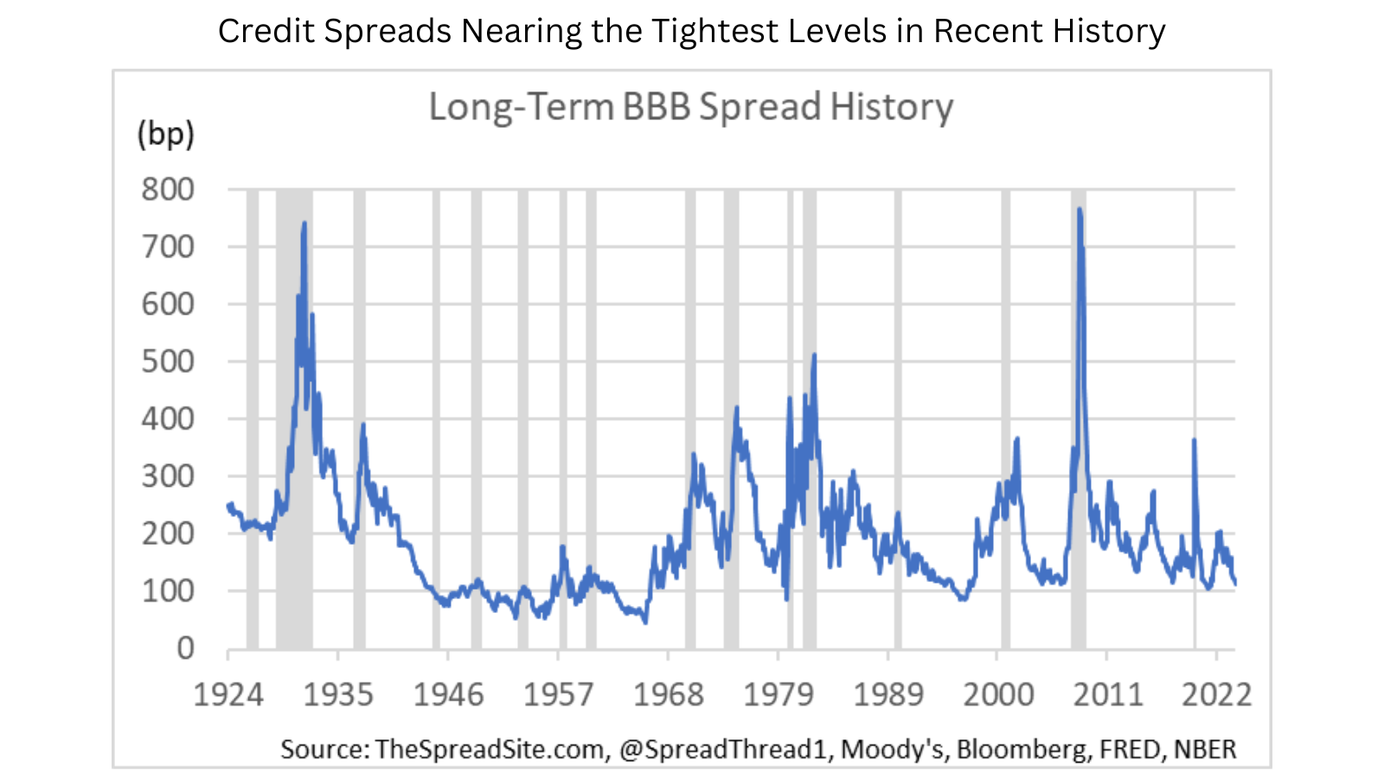

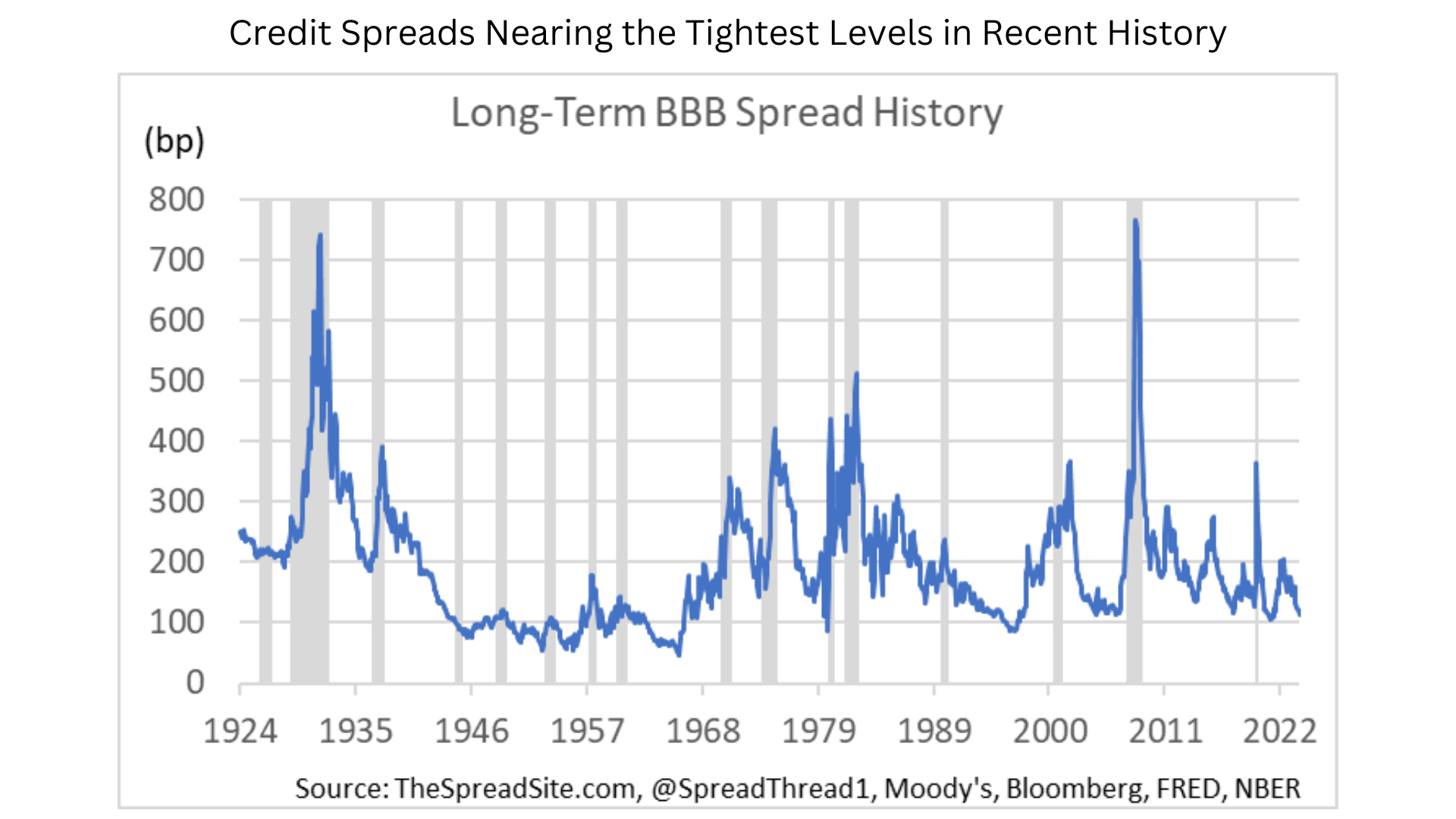

Zooming out, credit spreads are close to the tightest levels in the last fifty years or so. Modern credit markets have only been tighter for a brief period in 1997.

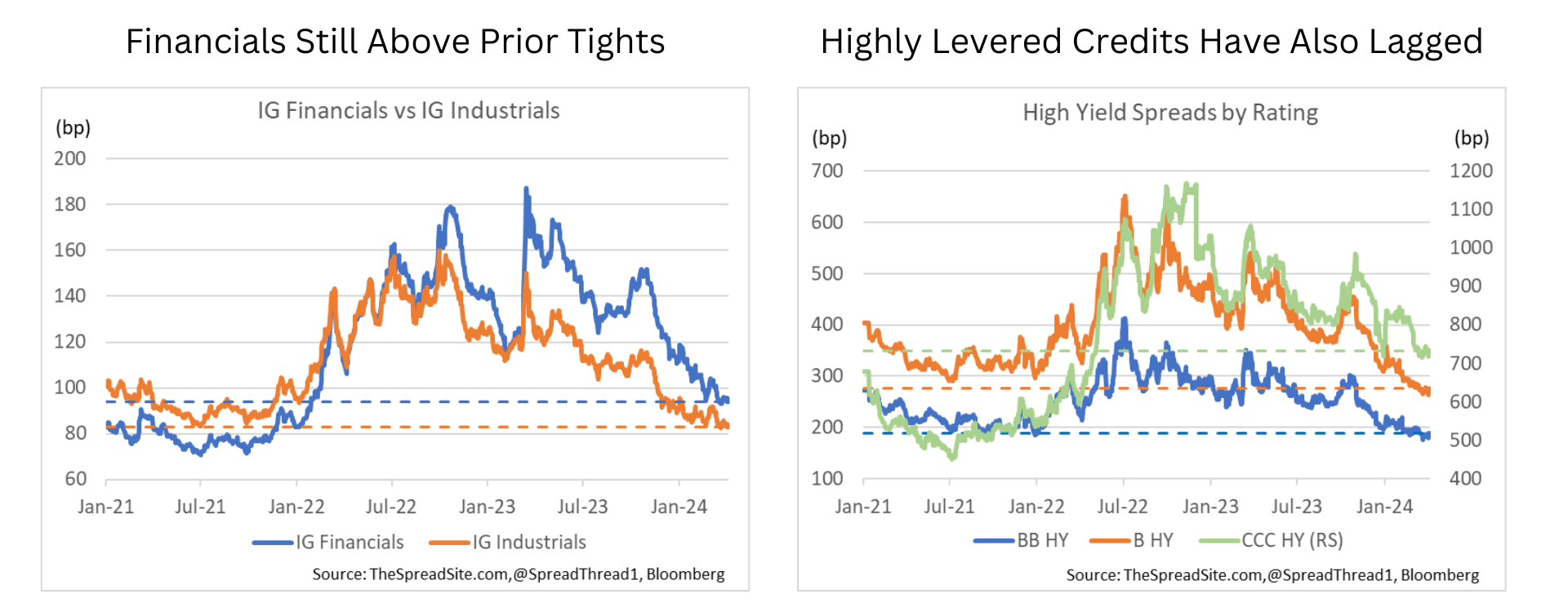

Though nearly all parts of markets have rallied, there is still some bifurcation under the surface. For example, in investment grade credit, non-Financials are at prior-cycle tights, while Financials still have a little ways to go. In High Yield the bifurcation is more noticeable, with Bs and BBs through the 2021 tights, while CCCs are almost 300bp wide to 2021 levels. Despite the strong rally to-date, there is still a reasonably sized distressed tail in the market.

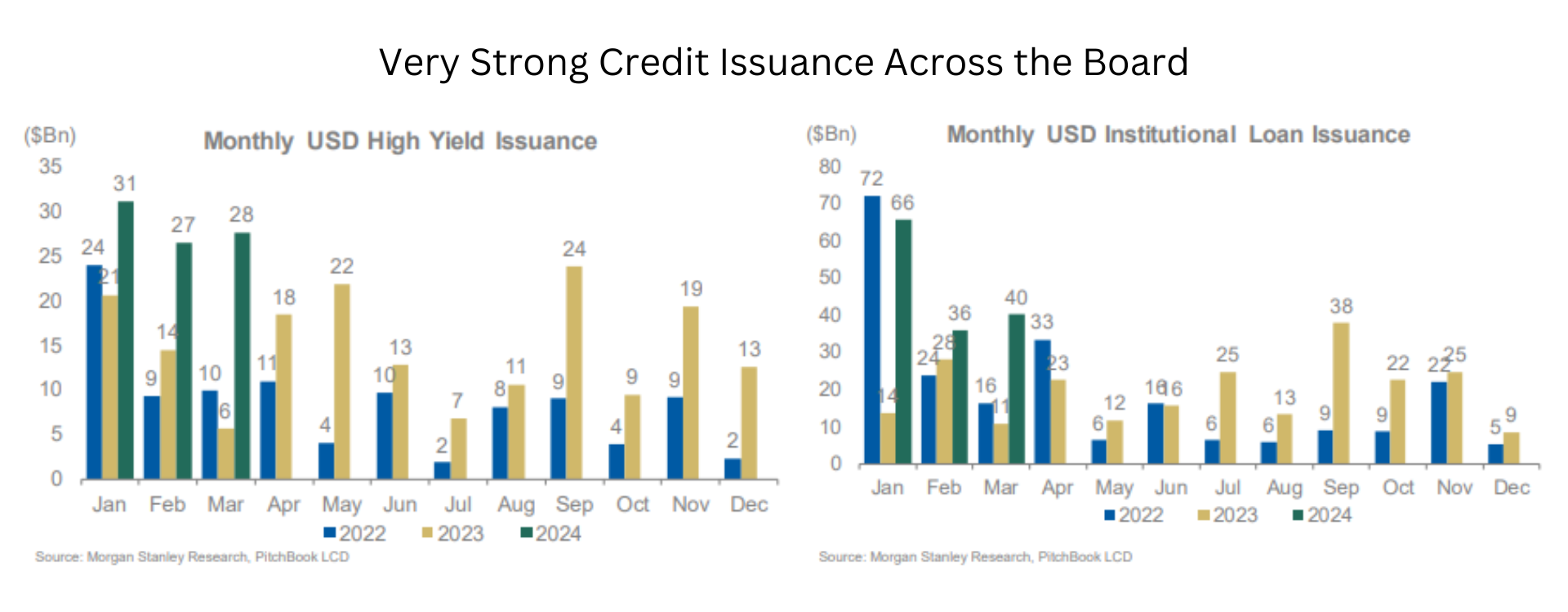

Along with the rally in credit, issuance has been substantial across IG, HY and leveraged loans. What is driving the supply? First, demand for new paper. As is often the case, strong returns in credit have driven flows into the asset class. And demand eventually leads to supply, as issuers take advantage of the open window. Second, issuance was reasonably subdued over the past two years, especially for levered borrowers (HY and loans). Private credit filled some of the void, but there is likely still some pent up need to issue debt. And lastly, companies want to strike while the iron’s hot given uncertainty later in the year, especially with upcoming elections.

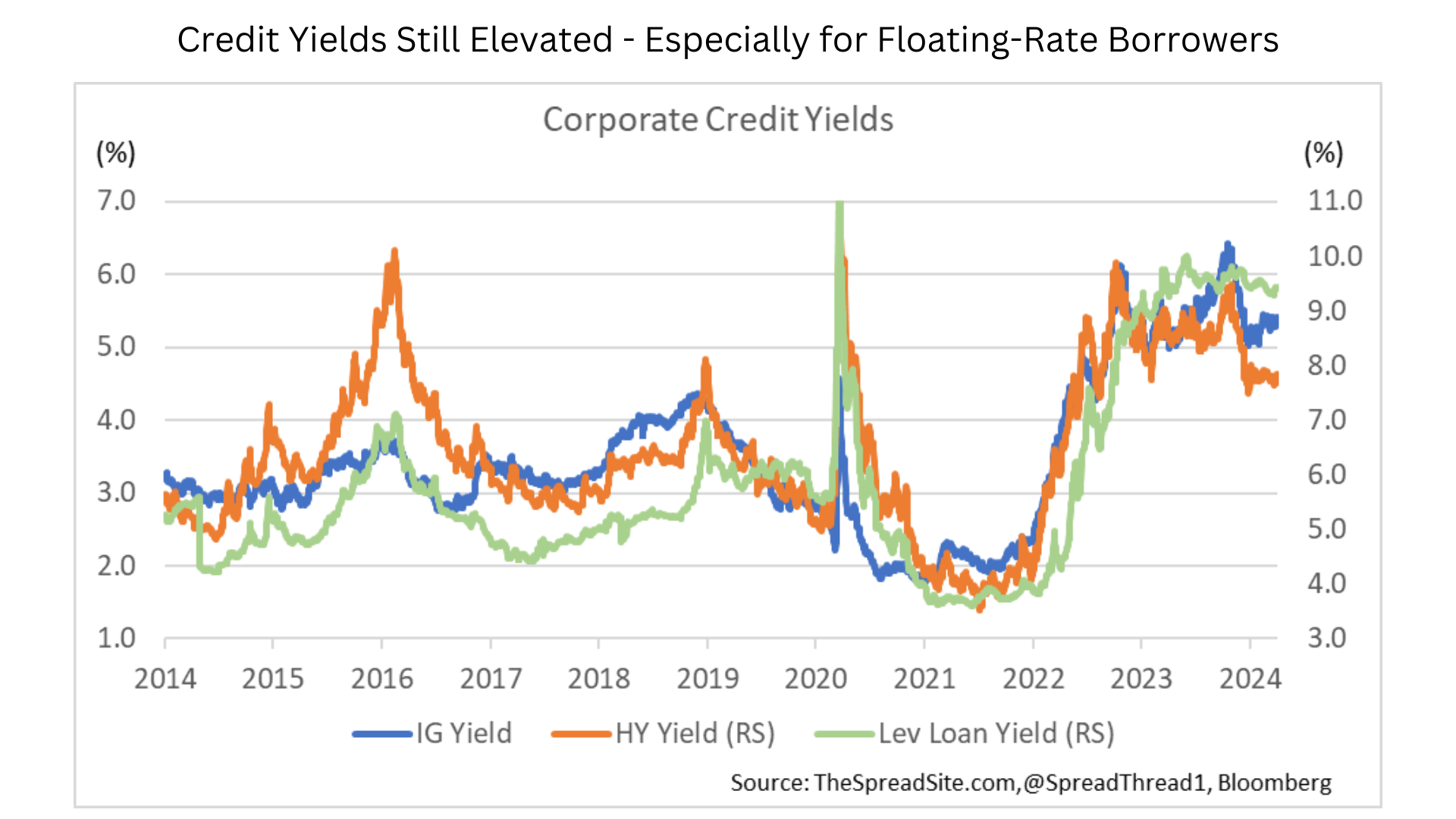

While spreads are very tight, yields are still wide, at least by post-crisis standards, especially for floating-rate borrowers (i.e., loan index yields ~9.5%). This means that issuers refinancing bonds, in most cases, are resetting their coupons HIGHER, unlike in almost all refinancing waves over the past few decades.

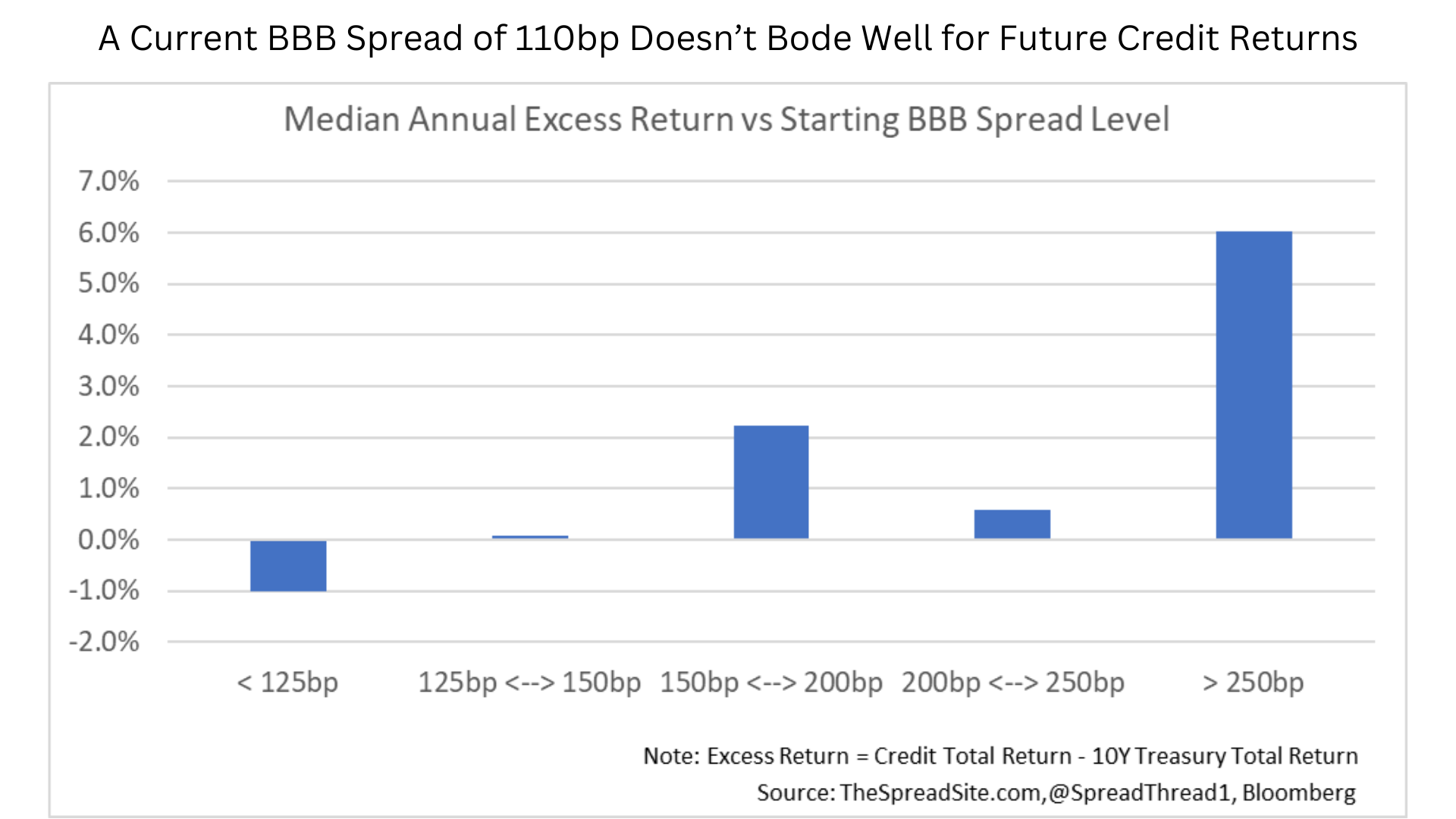

What do current spread levels tell us about the path forward? In short, not that much. Very tight spreads do imply weak returns going forward, to state the obvious. As we show below, credit tends to have a difficult time outperforming Treasuries when spreads are this tight.

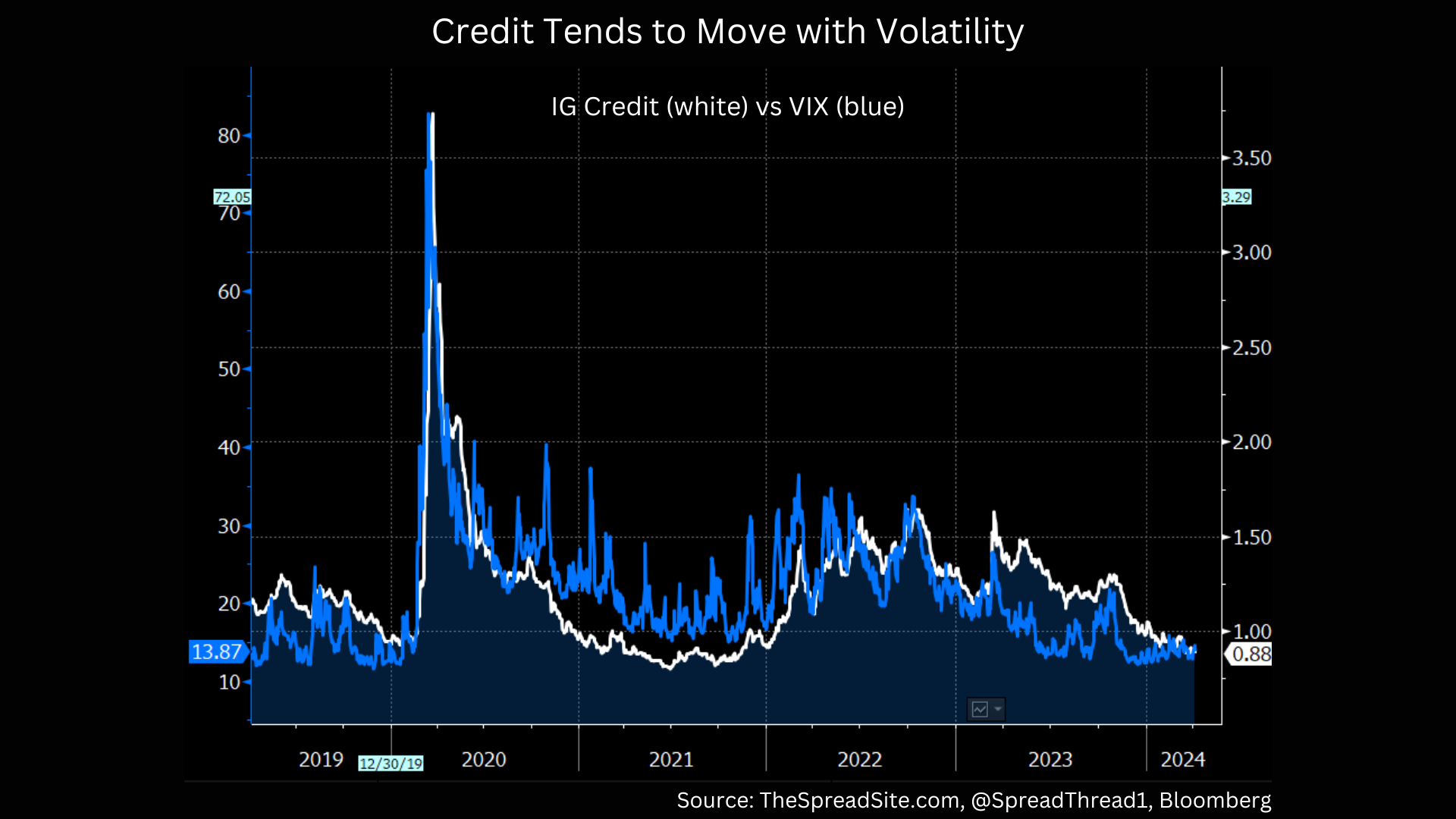

Beyond future returns, we are not sure tight spreads tell us much more than what we all know – the consensus expects this ‘Goldilocks’ backdrop to continue. In our view, public credit markets have become a sentiment gauge, generally trending with volatility in the medium-term.

So it is unlikely spreads tighten much from here, but there are multiple potential paths forward. Very tight credit spreads could mean markets are late cycle, like when High Yield hit ~250bp in June of 2007. But they could also be consistent with a mid-cycle environment like 2004, when spreads bounced around at tight levels for several years.

However, having a view on the cycle does matter for positioning within the asset class. For example, if you believe markets are mid-cycle, the right trade is to own the most levered parts of credit (i.e., CCCs) and play for spread compression. If you are in the late cycle camp, as we are, high beta credit is poor risk/reward, even if a turn is not imminent.

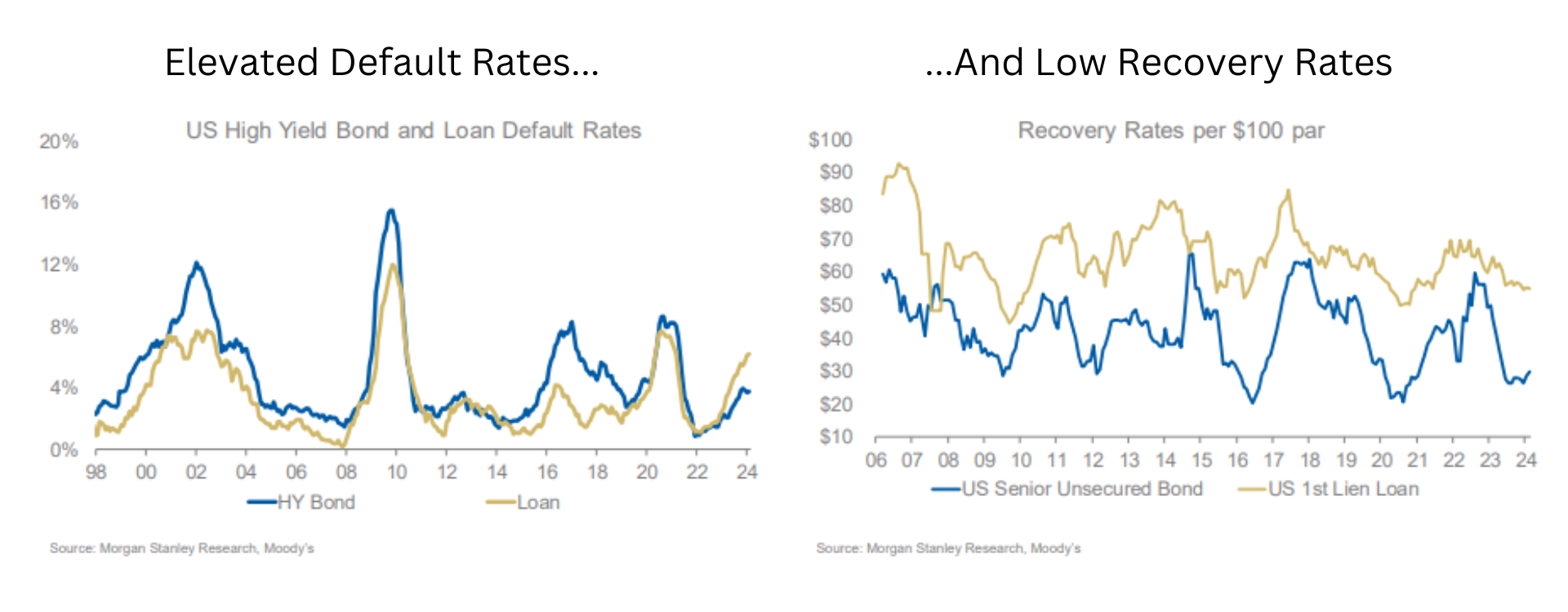

Finally, while spreads are very tight, default rates are actually quite elevated, and recovery rates are low. How can this be? One possibility is that defaults simply lag returns, and markets are saying defaults are going to turn lower again. For example, 2009 was a huge positive return year for credit, and also one of the highest default rates in history. The spread widening happened in 2008, forecasting the defaults to come in 2009. And the rally in credit in 2009 preceded the decline in defaults in 2010 and beyond.

The second possibility is that markets are misreading the situation, too optimistic about the reduction in credit stress around the corner. Our view is the latter, however, we don’t think this default cycle will look anything like 2009, where the default rate shot up and then shot right back down. In our view, the path will be bumpier where the default rate remains above average, but not double-digits, for several years, consistent with the work we’ve done on a ‘Haves/Have Nots’ economy and higher long-term rates.

Disclosures

Please click here to see our standard legal disclosures.

The Spread Site Research

Receive our latest publications directly to your inbox. Its Free!.

{kind=link}