A Below Par Report

Summary

-

Given this spike in rates over the past few months, a meaningful portion of corporate credit now trades at deeply discounted prices, which matters for valuations. In this week’s report, we walk through how to quantify the fair spread differential for high vs low dollar priced corporate bonds.

-

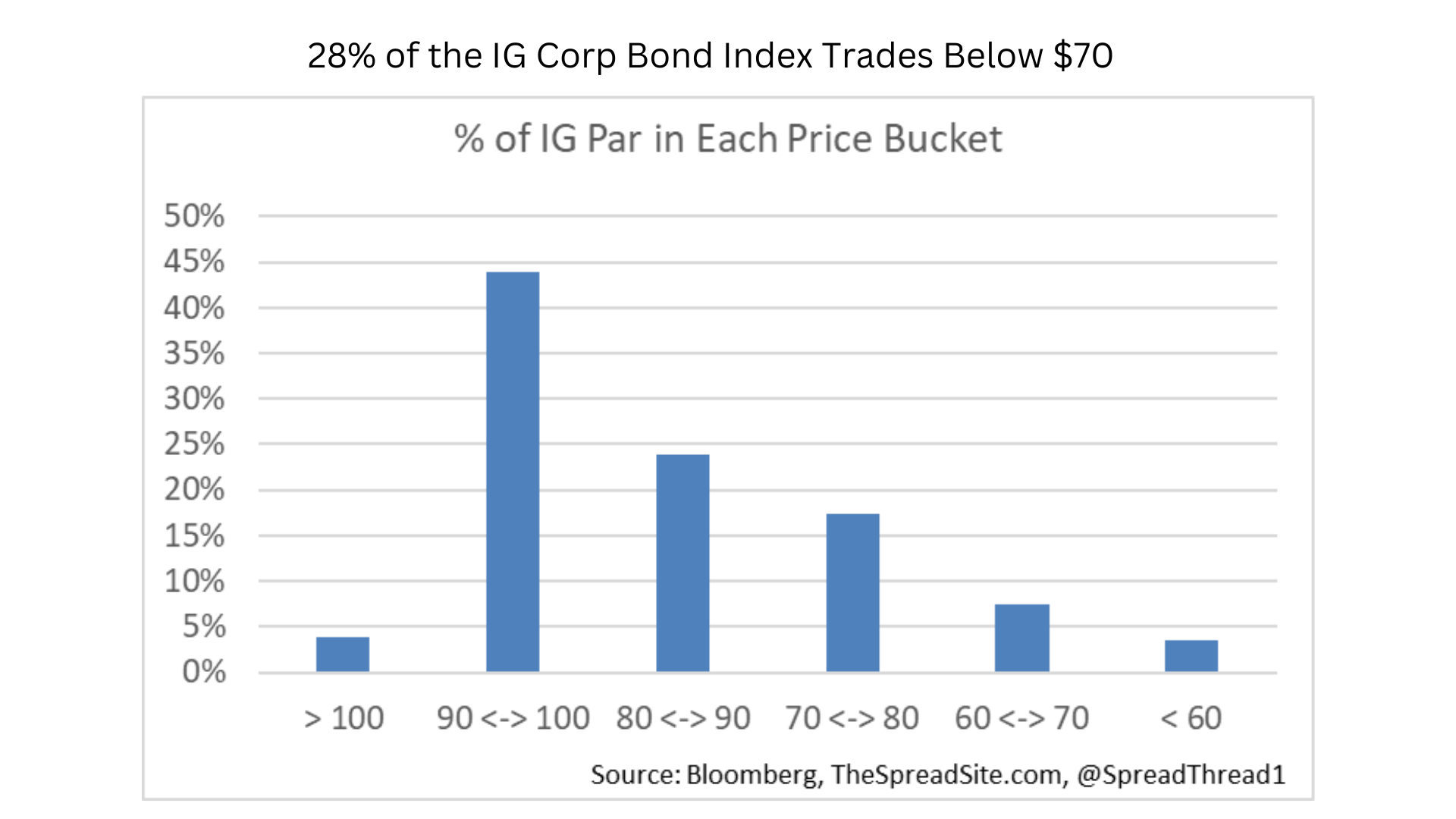

The current selloff in credit has been driven entirely by rising rates, not a re-pricing of credit risk (which we think is still to come). Only 4% of the IG corporate index is above par today, whereas 28% trades at a very deep discount, with a dollar price below $70.

-

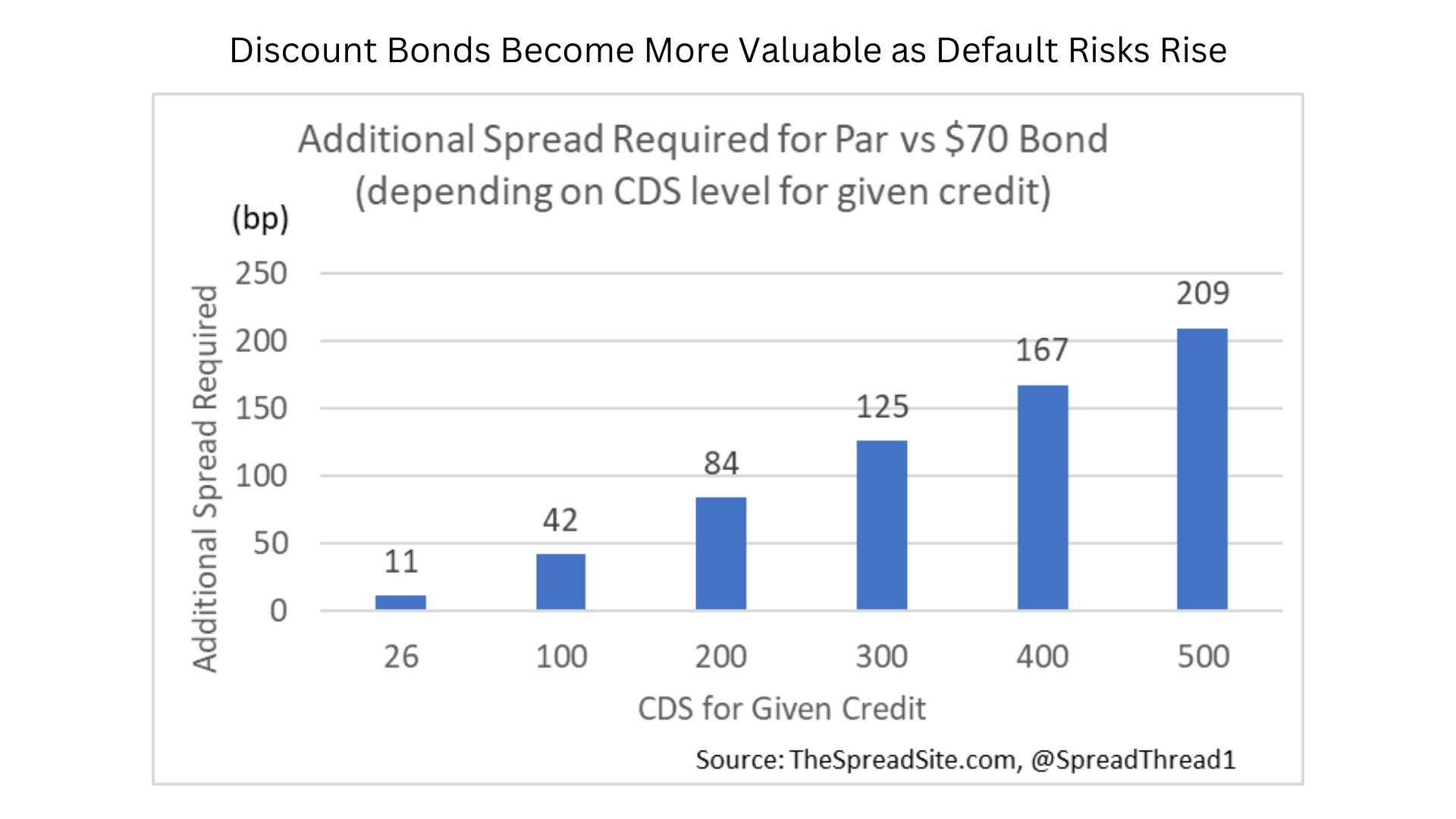

Discount bonds have value in credit because of a lower loss in the event of bankruptcy. We find a 10Y IG bond at a price of $70, should trade 42bp tighter than a 10Y par bond in the same cap structure, assuming a CDS spread of 100bp.

-

Using our methodology, the IG index is about 18bp cheaper than it would be if it were trading at par instead of $87, and HY is about 58bp cheaper. This is just one component of a ‘fair value’ calculation. Credit is still quite rich, all things considered.

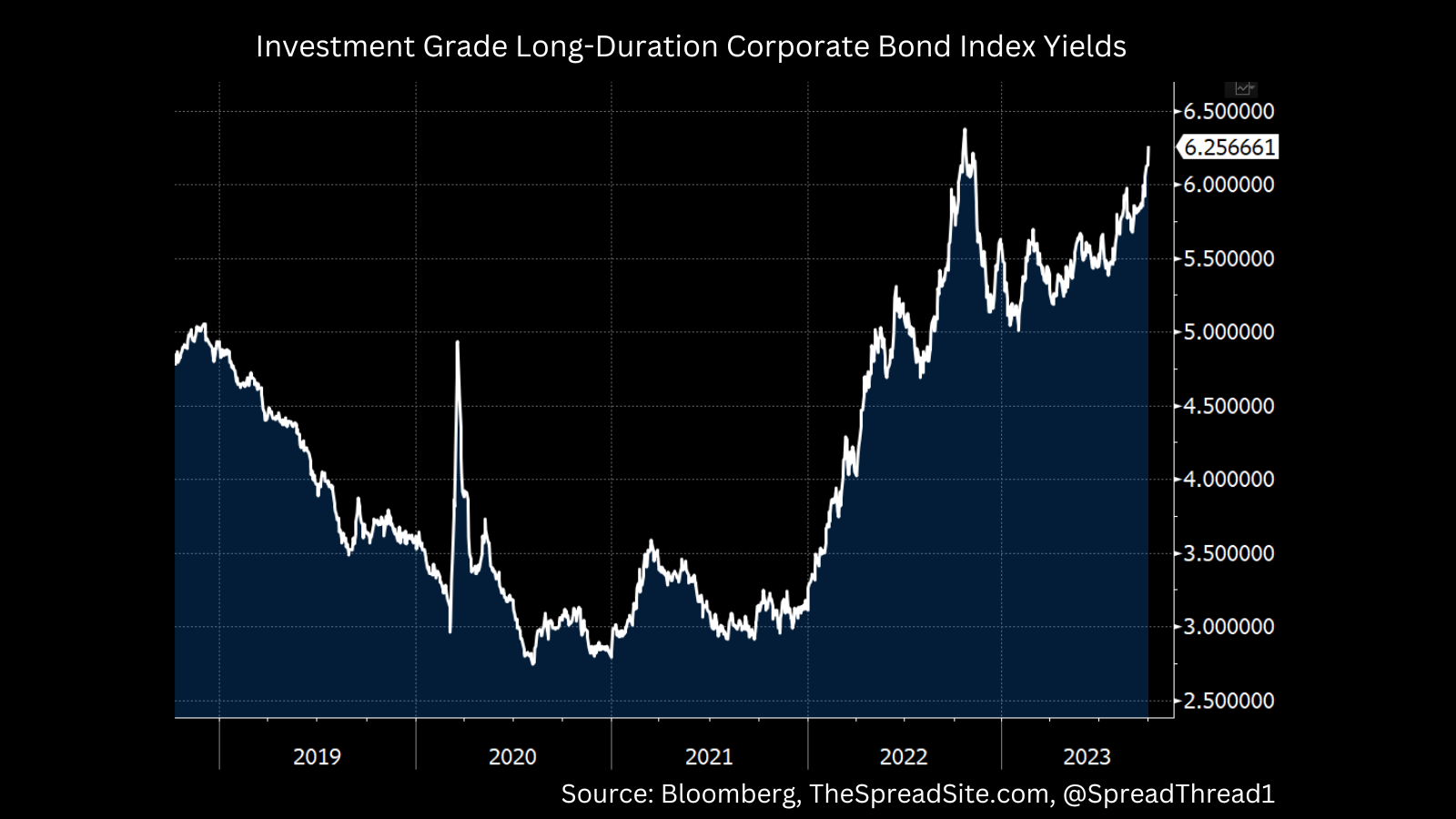

The rise in interest rates over the past few months has been dramatic, pushing investment grade yields to 6.15%, finally surpassing the peak in October of 2022. The inverse of those high bonds yields is very low prices, which can have interesting implications for fixed income investors. For example, in the MBS market, very low prices mean prepayment risk is low. To state the obvious, homeowners are unlikely to refinance a 3% mortgage when the prevailing rate is now well above 7%. Similarly, low dollar prices can have an impact on corporate credit valuations/ spreads that in normal times doesn’t matter all that much. But given the carnage in high-quality long-duration bonds of late, and the wide array of deeply discounted bonds as a result, we think the valuation impact of low dollar prices is more important today. In the note that follows, we briefly walk through how to quantify the fair spread required when buying a high vs low dollar priced bond.

Quantifying the Discount

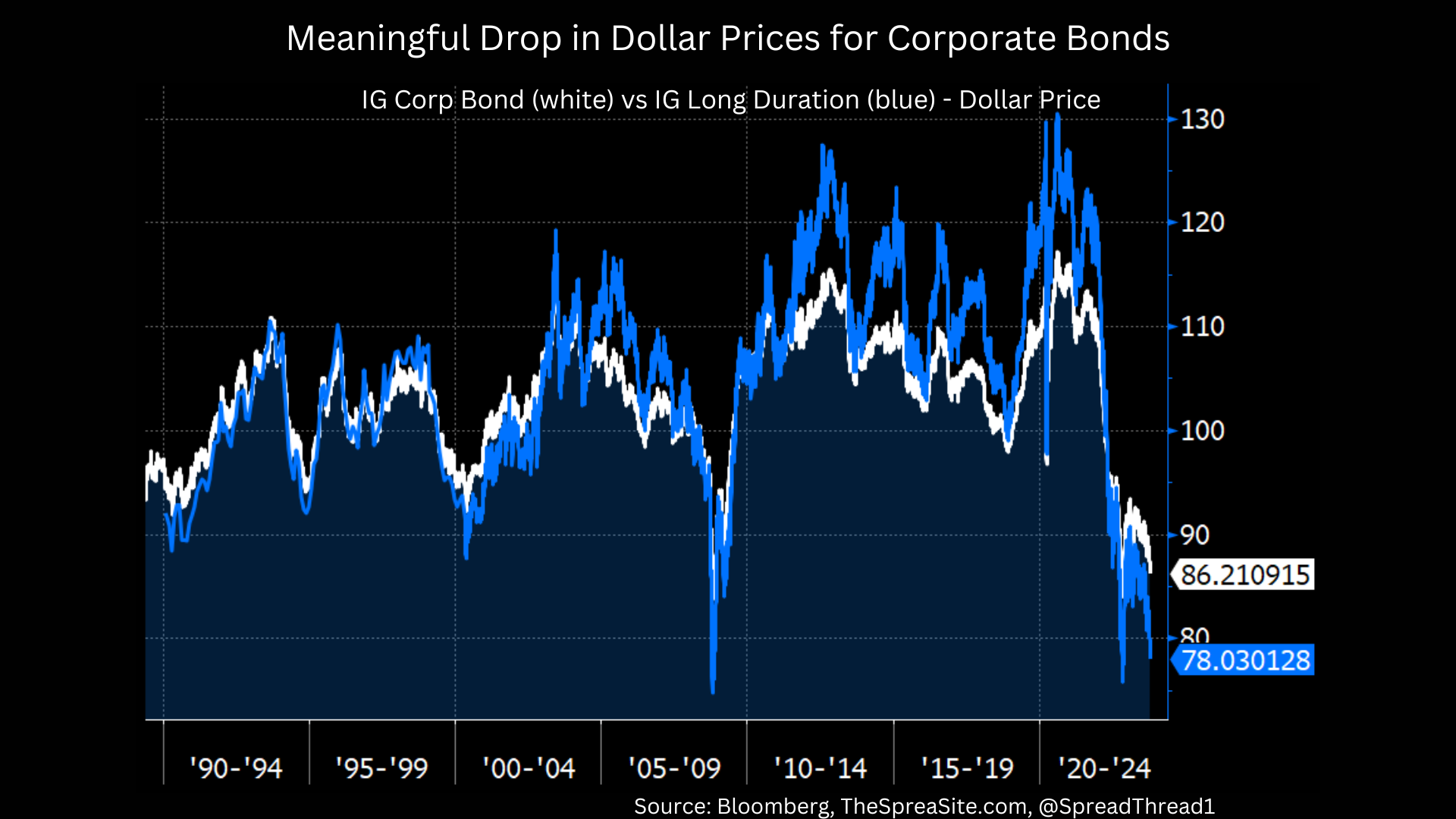

To begin with, the drop in dollar prices, especially for investment grade credit has been significant, with the index now trading at $86, a level rarely seen in history. The long-duration IG bond index trades at $78, even more dramatic. High yield has been hit less-hard by rising rates than IG, given a lower duration in the former, but still trades well below par at an index price of $87.

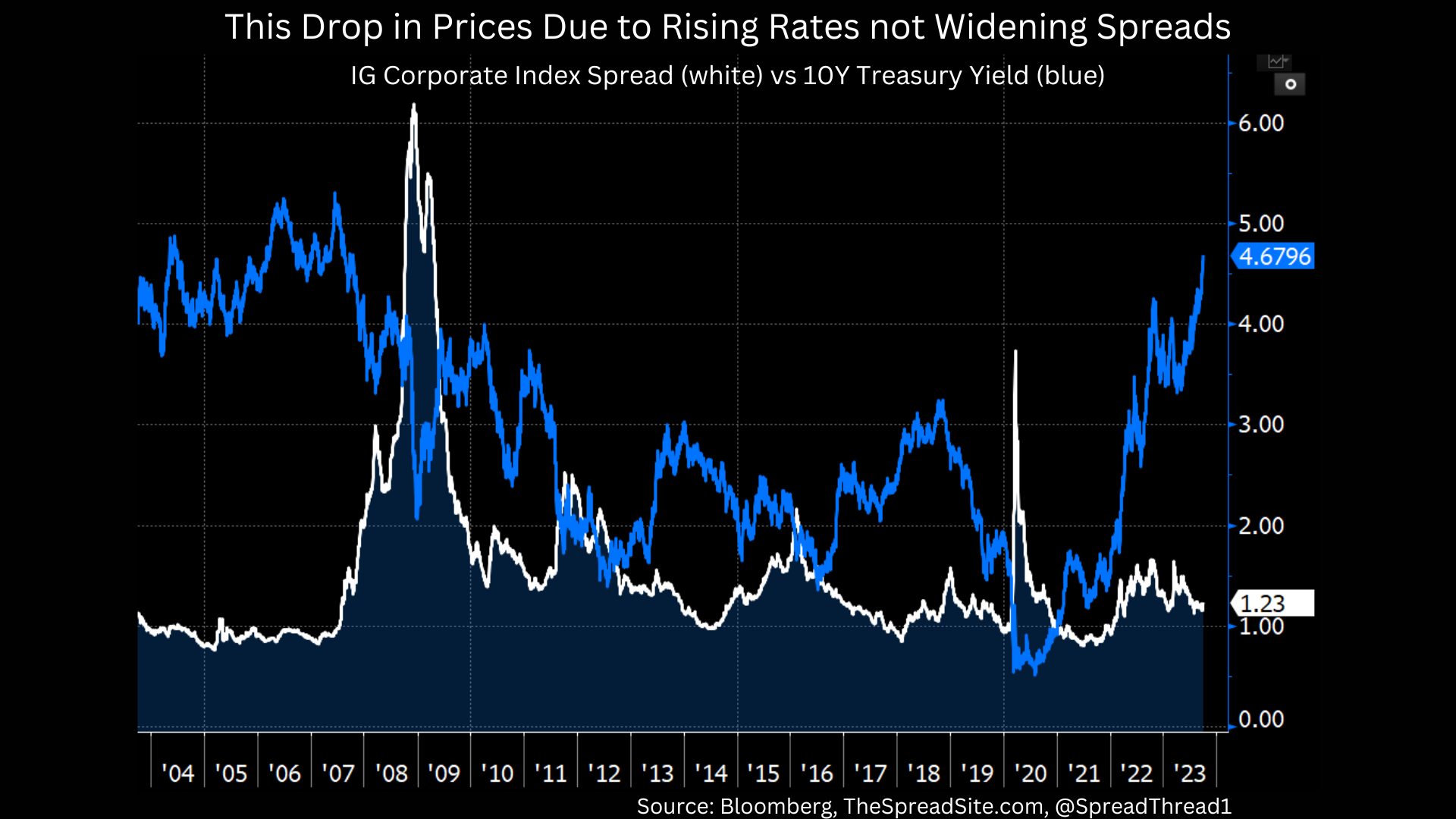

Many past instances of a sharp drop in prices have come from widening spreads in periods of stress, such as 2008 and 2020. Even last year’s rise in rates coincided with IG spreads hitting 165bp and HY ~600bp, pricing in some incremental default risk as recession concerns rose. The current selloff in credit, on the other hand, has been driven entirely by rising rates, with spreads moving only marginally wider. In other words, index prices dropping to current levels is not the market’s way of pricing in increased “credit risk” (i.e., defaults/ downgrades). We think that re-pricing is still to come, but for now the move lower in corporate bond prices is all about rising interest rates.

In the Exhibit below we show how much par outstanding in the IG corporate bond index sits in each dollar price bucket. Only 4% of the index now trades above par, whereas 28% is now at a very deep discount, with a dollar price below $70.

Valuation Implications

Discount bonds have value in credit (vs par or premium bonds) because in the event of bankruptcy, all bonds have the same par claim (assuming the same level of seniority in the capital structure – ignoring minor differences for accrued interest). This means bonds that trade at a lower price only due to a lower coupon have less of a loss in the event of default, and therefore should trade at a tighter spread, all-else equal. As a sidenote, all else usually isn’t equal. For example, two bonds in the same cap structure can have different levels of liquidity, impacting relative valuations. For this analysis, we hold factors like liquidity constant for bonds within a given capital structure.

Getting to the math, using market pricing and/or historical default rates, we can calculate the fair spread differential between two bonds with the same probability of default but with different dollar prices. For example, a bond trading at $70 will have 30 points less of loss in a bankruptcy (slightly offset by higher coupons over time) vs a par bond in the same cap structure. Using the CDS curve for a given name, assuming it has one, we can calculate how much it would cost to hedge against that additional loss in the event of default per year, PV that cashflow, and then convert it into an annual spread using the duration of the bond. As the chart below shows, a 10Y IG bond at a price of $70, should trade 42bp tighter than a 10Y par bond in the same cap structure, assuming a CDS spread of 100bp. If we assume a CDS spread of 400bp, the spread premium of the par bond (vs the $70 priced bond) rises to 167bp.

This method uses risk-neutral default probabilities. If we instead use actual historical default rates, the fair spread is lower. For example, on the chart below we show that using the long-term average default rate for BBB bonds of 26bp, the fair spread differential drops to 11bp (note- the long-term average speculative grade default rate is about 3%, for comparison). However, we think this underestimates the true fair value difference between a discount and par bond because it is essentially assuming zero risk premium.

This point aside, this framework gives you some perspective on how to value low vs high dollar price bonds. Using our methodology, the IG index is about 18bp cheaper than it would be if it were trading at par instead of $87, and HY is about 58bp cheaper due to lower prices/coupons. Credit is still quite rich, in our view, and other differences often work in the other direction (such as lower ratings quality in IG vs history). That said, low dollar prices, at the margin, do help credit valuations, once again, all-else-equal.

A final important consideration – low dollar price bonds can underperform in a rising rate environment, given their longer duration. But historically, they behave more defensively as spreads widen because markets often demand a much bigger premium for riskier bonds, including those with a higher losses in the event of default.

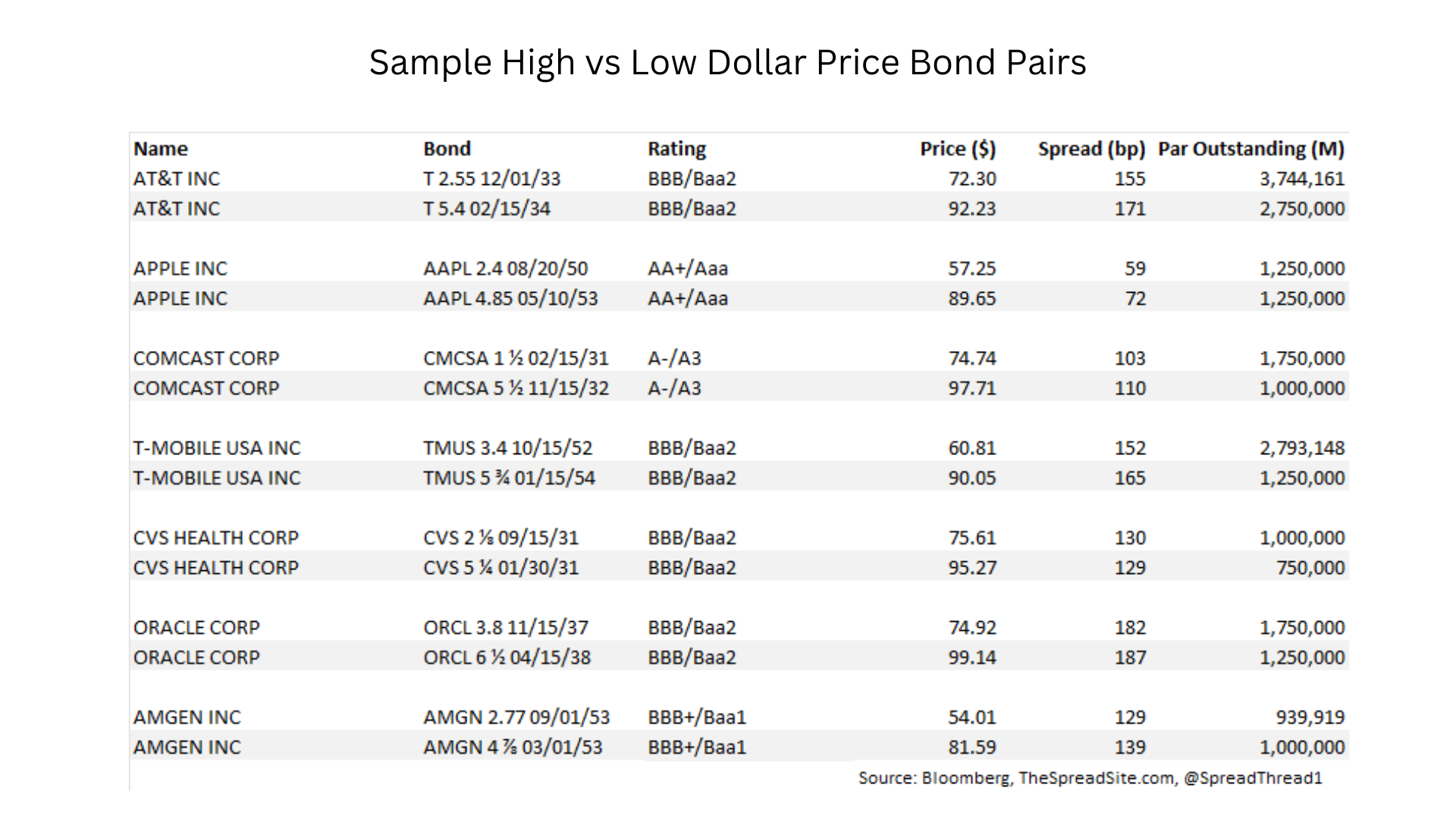

Single Name High/Low Price Pairs

Lastly, we end with some single name pairs – bonds within a given cap structure with a large difference in price given very different coupons. We tried to pick similar bonds, for example roughly the same maturity, not a very large difference in issue size, etc… Of course, it is impossible to control for every factor except coupon. Some of these bonds will be less liquid than others, which will affect the spread differences. But hopefully this gives a few examples of how the market values the premium required when buying a higher (vs lower) dollar priced bond. In general, we believe the market typically under prices this premium in tight spread environments like today.

Disclosures

Please click here to see our standard Legal Disclosures

The Spread Site Research

Receive our latest publications directly to your inbox. Its Free!.

{kind=link}