Ahead of the Fed

Markets are two days away from a Fed meeting, which has the potential to rattle this ‘Goldilocks’ market. Taking a step back, over the last 4-5 months, stocks have moved higher in nearly a straight shot, and bonds have been mostly range-bound. A still healthy economy, optimism around a 1990s-like productivity boom, declining inflation, and expectations of a rate-cutting cycle have fueled risk assets. Of course, it was never going to remain this easy indefinitely, and dynamics may now be changing.

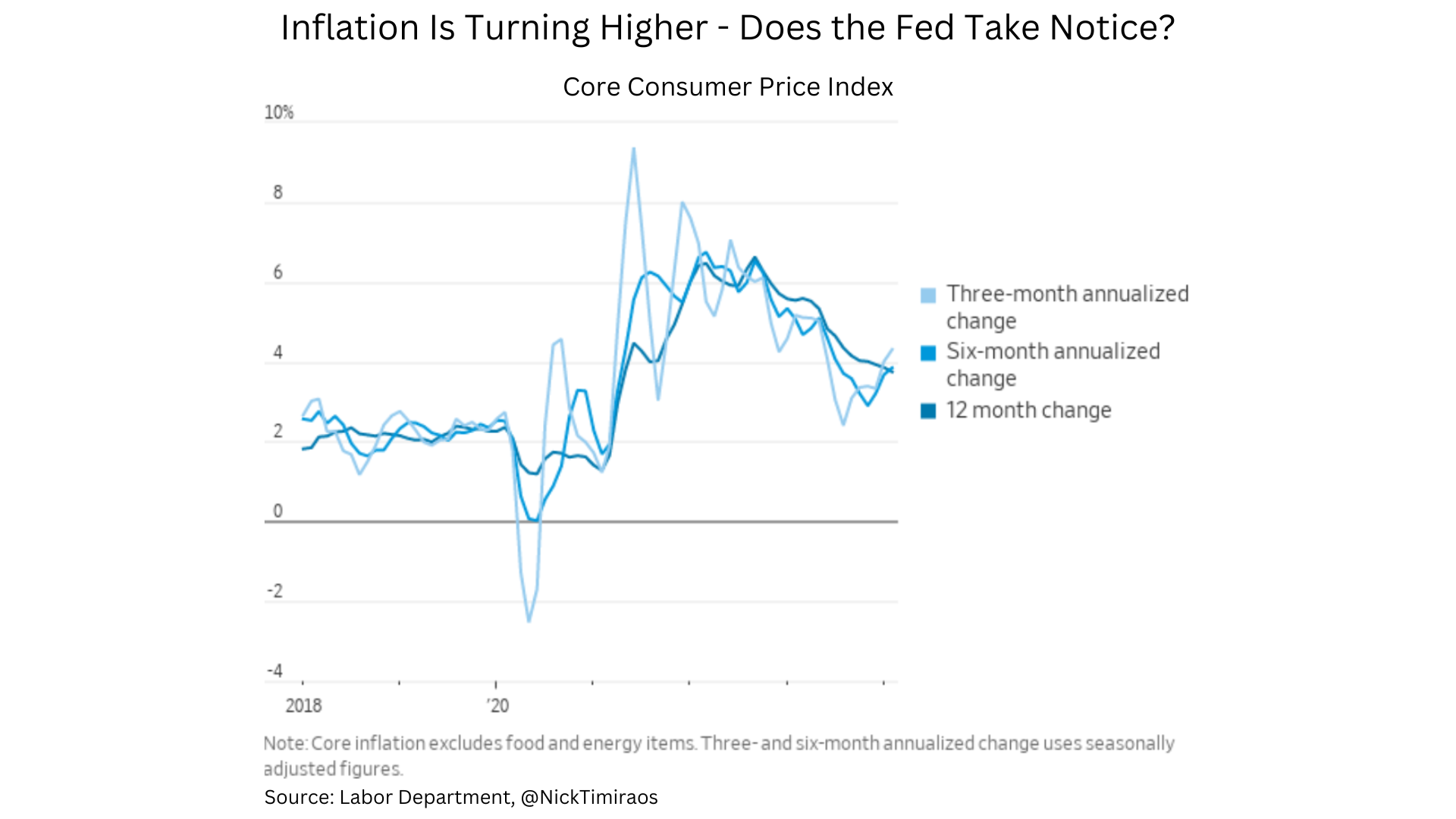

The first shot across the bow was a hotter-than-expected inflation print in January. This datapoint was easy for markets to ignore as ‘one-off.’ A single datapoint is often noisy, especially in January, given challenges with seasonal adjustments around the start of the year. However, last week we received another hot CPI and PPI report, raising the odds that the disinflation narrative could be coming to an end, at least for now.

On Wednesday, markets will be focused on the nitty-gritty details of the Fed meeting, as is usually the case. Does the median 2024 dot drop from 3 cuts to 2? Do longer-run dots drift higher signaling concerns that policy may not be as restrictive as initially expected? Do inflation forecasts move up? These details aside, the bigger picture question Powell hopefully answers in the press conference – does he believe the disinflation trend of the past year may be stalling?

For example, in order to cut rates Powell has said the Fed needs more good inflation data. In his words, “It’s not that we’re looking for better data — it’s just that we’re looking for a continuation of the good data that we’ve been getting. We just need to see more.” After the past two months, it hard to argue the “more good inflation data” box is getting checked. For example, the 3-month annualized pace in core PCE, the Fed’s preferred inflation gauge, may have risen to ~3.5% in February from ~2.5% in January.

But he can spin it in multiple ways. Powell has repeated many times that the path to bring down inflation will be bumpy. Does he message recent inflation data as just a bump on the path to 2% and that the Fed remains on track to cut “at some point” this year? Or does he spin it in a more hawkish way, talking up the risk to 2024 cuts? We think this answer will be key to whether this press conference is taken as hawkish or dovish by markets.

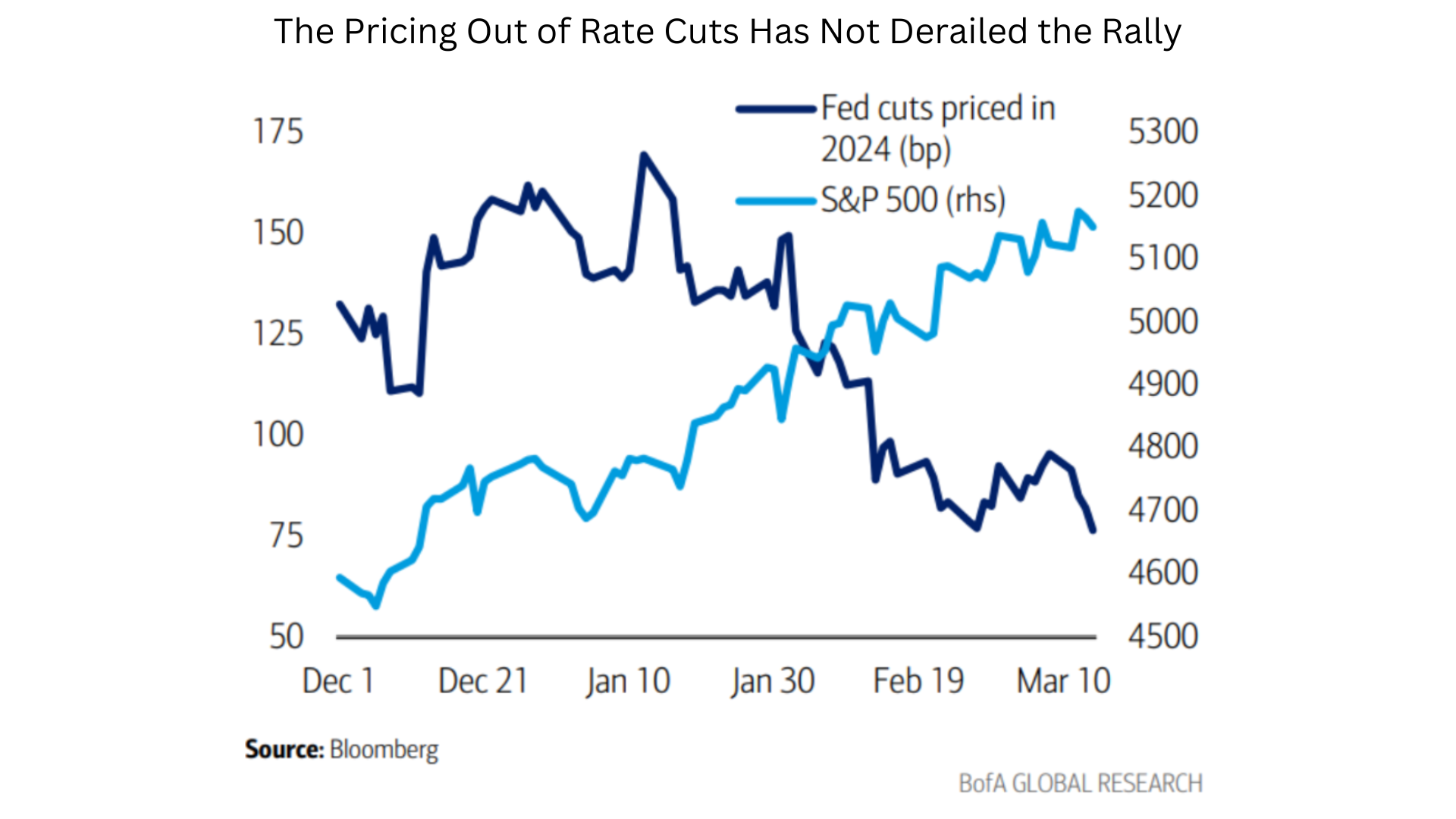

To some extent, the bond market has already front run the Fed, slowly pricing rate cuts out, with an average of ~2 cuts now expected in 2024 vs ~6 cuts anticipated just a few months ago. And this more hawkish pricing hasn’t derailed the equity market, at least so far. Why not? For one, until recently, like the Fed, investors have generally believed fewer cuts are due to solid growth, not renewed inflation. And related, long-end bond yields have remained range-bound, also supporting risk assets.

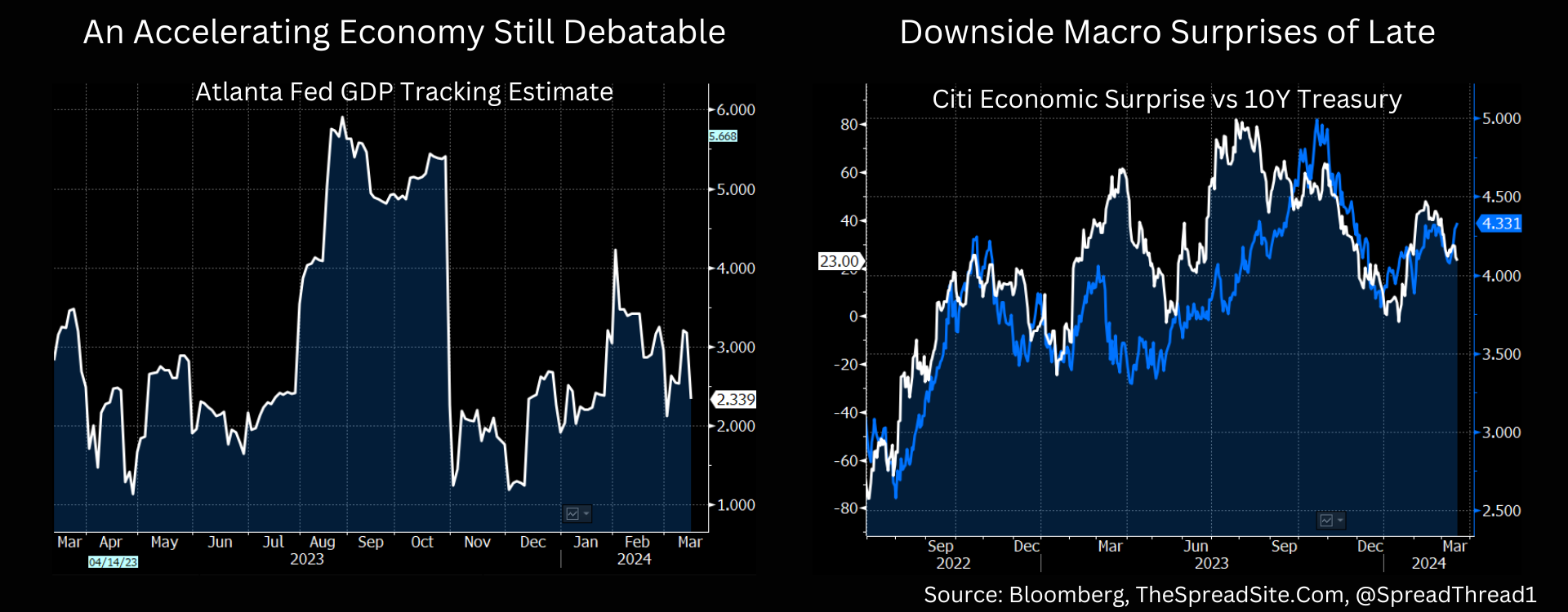

Why haven’t long-end bond yields risen more materially with a few hot inflation prints and the belief that growth is accelerating? In our view, because accelerating growth may be more narrative than reality. In fact, despite clear reasons for a re-acceleration – for example, a large drop in Treasury yields in 4Q23 and a sharp rally in risk assets (and hence positive wealth effect), the Atlanta Fed 1Q24 GDP tracking estimate is just 2.3% (Goldman is at 1.6%). Additionally, as the chart below shows, over the past year or so, long-end bond yields have generally followed economic data surprises, which have turned down over the past month, keeping a lid on yields.

Despite mixed data, inflation is coming in hotter, and inflation breakevens as well as commodity prices are rising. We think these dynamics increase the odds that Treasury yields finally break out of the recent range to the upside. This price action, combined with a hawkish Powell on Wednesday, may finally drive a tradeable pullback in equities. To conclude, the way we see markets at a high level in the short term is as follows:

- We think bond yields break higher in the short-term, but we would buy that dip (in prices). We don’t think the economy is accelerating, and believe the jobs markets is softening (slowly). All it takes is one weak payroll print for the macro narrative to shift and duration to quickly reverse course. We doubt long-end yields in the high-4% range are sustainable for long.

- If Powell comes off as dovish, yet again, then the rally in risk can broaden. The R2K likely outperforms and gold has another leg higher. We would fade this ‘broadening’ trade, however. We think large-cap/quality is the right trade, likely until we are well into a rate-cutting cycle. We continue to believe gold and therefore gold miners can work in multiple scenarios.

- A hawkish Powell is not a catastrophe for markets, but likely catalyzes a bit of a reversal in the ‘everything rally’ of the past few months. We think this could drive the first tradeable correction of 2024 (5-10% over a month or two), but still believe dips will get bought until tighter Fed policy transitions into recession scare.

Disclosures

Please click here to see our standard legal disclosures.

The Spread Site Research

Receive our latest publications directly to your inbox. Its Free!.

{kind=link}