A Late-Cycle Melt Up

SUMMARY

-

The sharp rally YTD has many, us included, reassessing our market and macro views. However, we continue to believe that price action in 2022/23 is not abnormal for a late cycle period.

-

Markets often correct around when the Fed begins raising rates. Yes, it is not always a 25% selloff like last year, but price action is typically weakest during fast rate hike cycles, and this one certainly qualifies as fast.

-

In addition, markets usually rally meaningfully while the curve is inverted, many times to new cycle highs. Even credit often hits cycle tights only shortly before a recession. Quite simply, the period when rate hikes are nearly done but unemployment is still low, allows markets to dream of soft landing.

-

We certainly would not underestimate how far the melt-up could go or how long it could last. But we do believe a ~20x p/e multiple on the S&P 500 and current high yield spreads (380bp) very much require Goldilocks to continue. We like asymmetric bets that it does not.

INTRODUCTION

Markets in 2023 have done a good job proving most investors wrong. If you are in the entrenched inflation camp, the current disinflation narrative, combined with tame long-end bond yields has been frustrating. If you are in the recession camp, an S&P 500 just 5.5% from all-time highs has been even worse. If you are one of the 3 investors predicting ‘Goldilocks’ to start the year (we certainly were not), congrats on crushing 2023 thus far.

We still firmly believe in the broader cycle framework that we recently laid out in Cycling Through the Noise, and have noted many times just how slow this process can be. Regardless, it is important not to dismiss price action and always consider what the market is telling us that we could be missing. The question we find ourselves asking as stocks rally seemingly every day – is the worst behind us and are we back to slow and steady growth, or is this just another sharp swing in sentiment, which is not atypical near cycles turning points?

ASSESSING THE RALLY

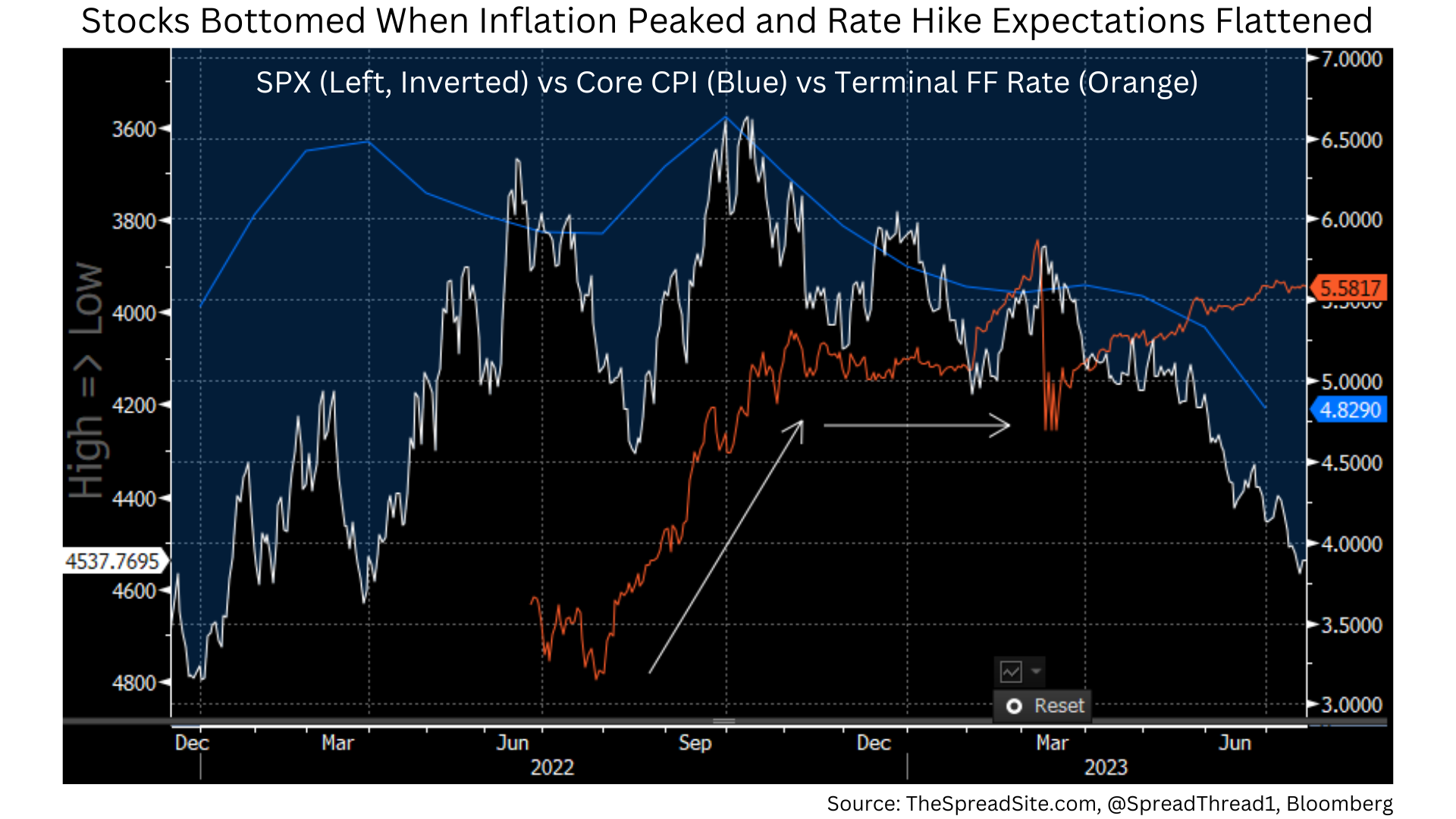

First, we take a step back and think about what has driven this sharp rally in 2023. There are many possible explanations. We believe the main driver is simply the belief that inflation has been tamed without a rise in unemployment, and as a result, the hiking cycle is coming to a close. Said another way, 2022 was about an unexpected surge in inflation and the fastest rate hike cycle in decades. 2023 has been a perceived moderation in those risks, with markets bottoming right around when core CPI peaked, and when the rise in the terminal Fed Funds rate leveled off.

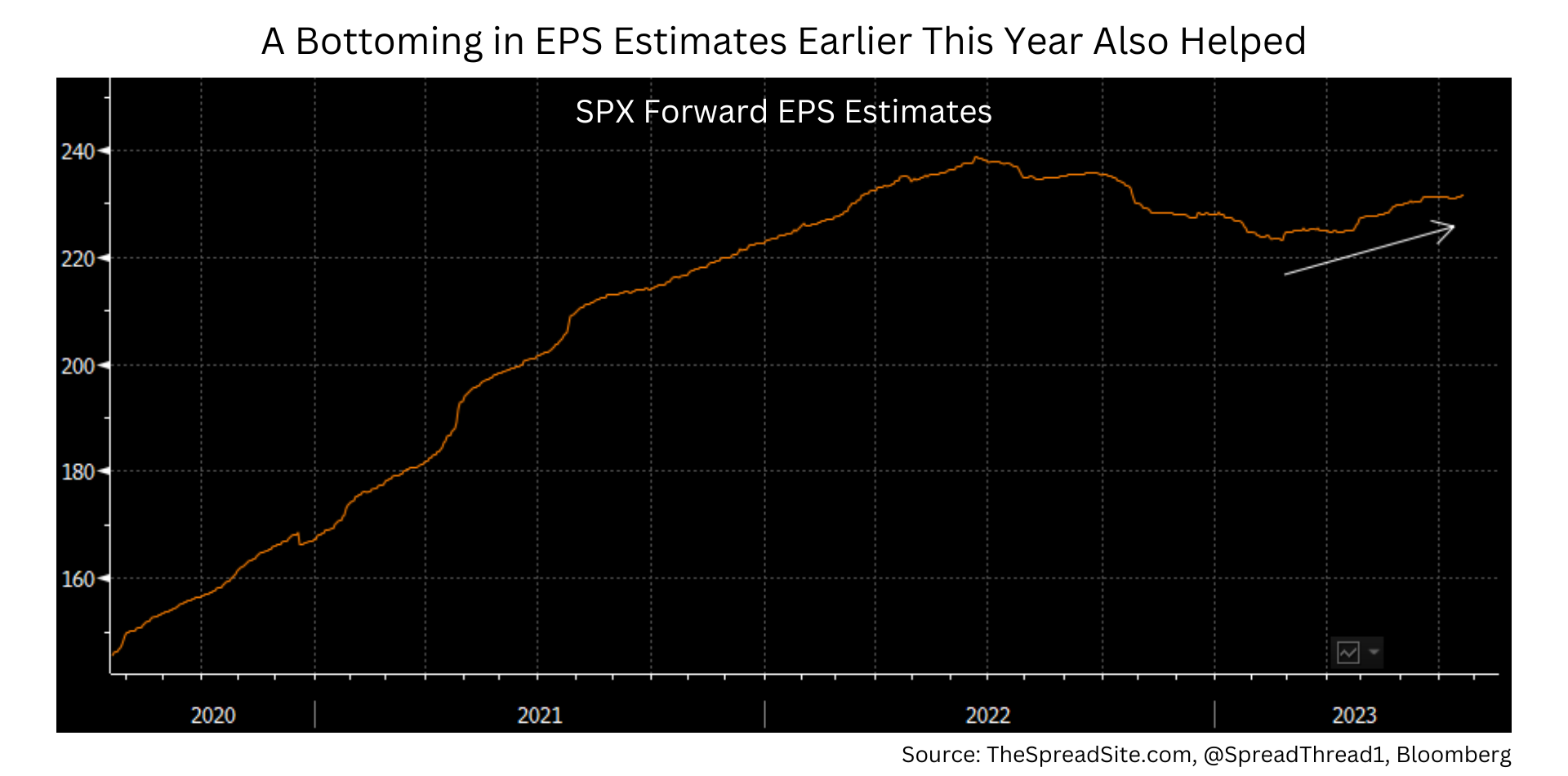

Clearly, there have been other drivers of this rally as well. For example, forward earnings estimates bottomed early in the year, and have trended upwards ever since, helping fuel the soft-landing narrative, and the idea that companies have successfully weathered the rate hikes.

Additionally, we are still firmly in the camp that the impact of the banking stress in March, in the form of even tighter credit conditions, is meaningful and will be increasingly felt over time. But as a side effect, it did slow down the Fed, arguably supporting asset prices in the process. And finally, other technical factors such as overly bearish sentiment to start the year, have clearly contributed to the extent of the rally as well.

NORMAL CYCLE BEHAVIOR

We continue to believe that while this is a very unique cycle in many regards (they all are), price action in 2022 and 2023 is not abnormal for a late cycle period.

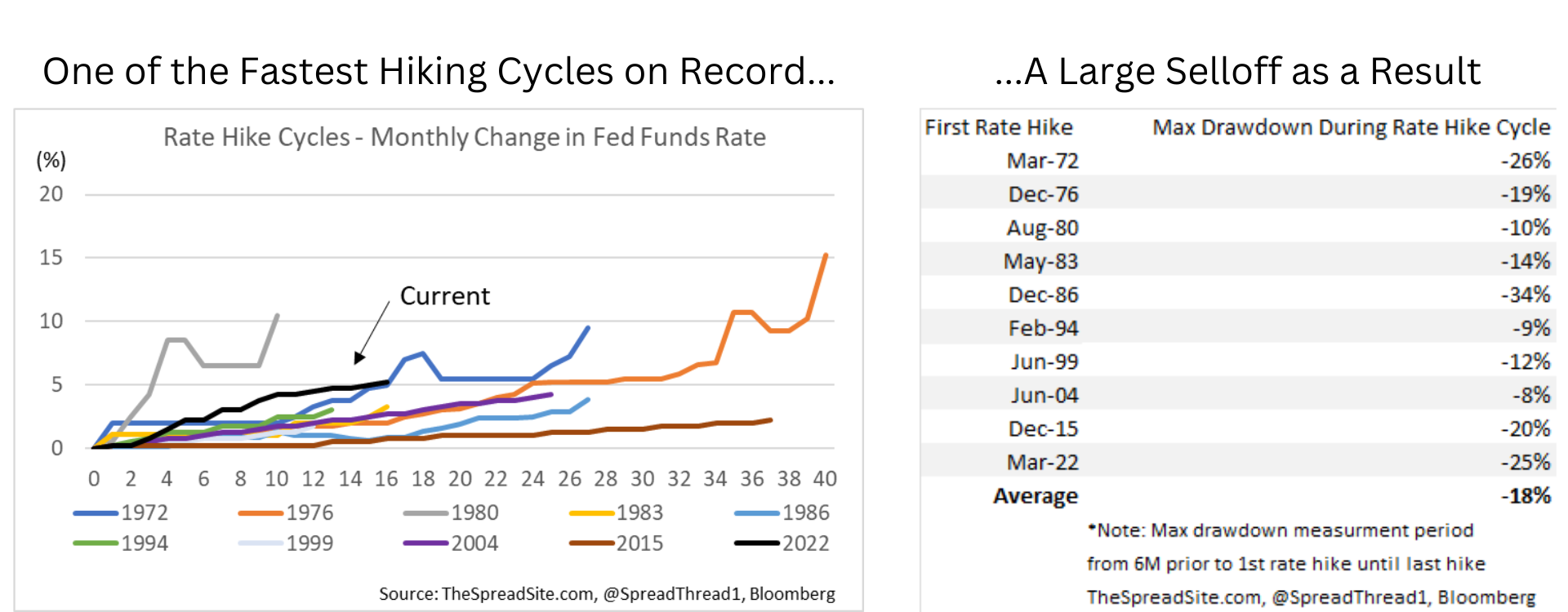

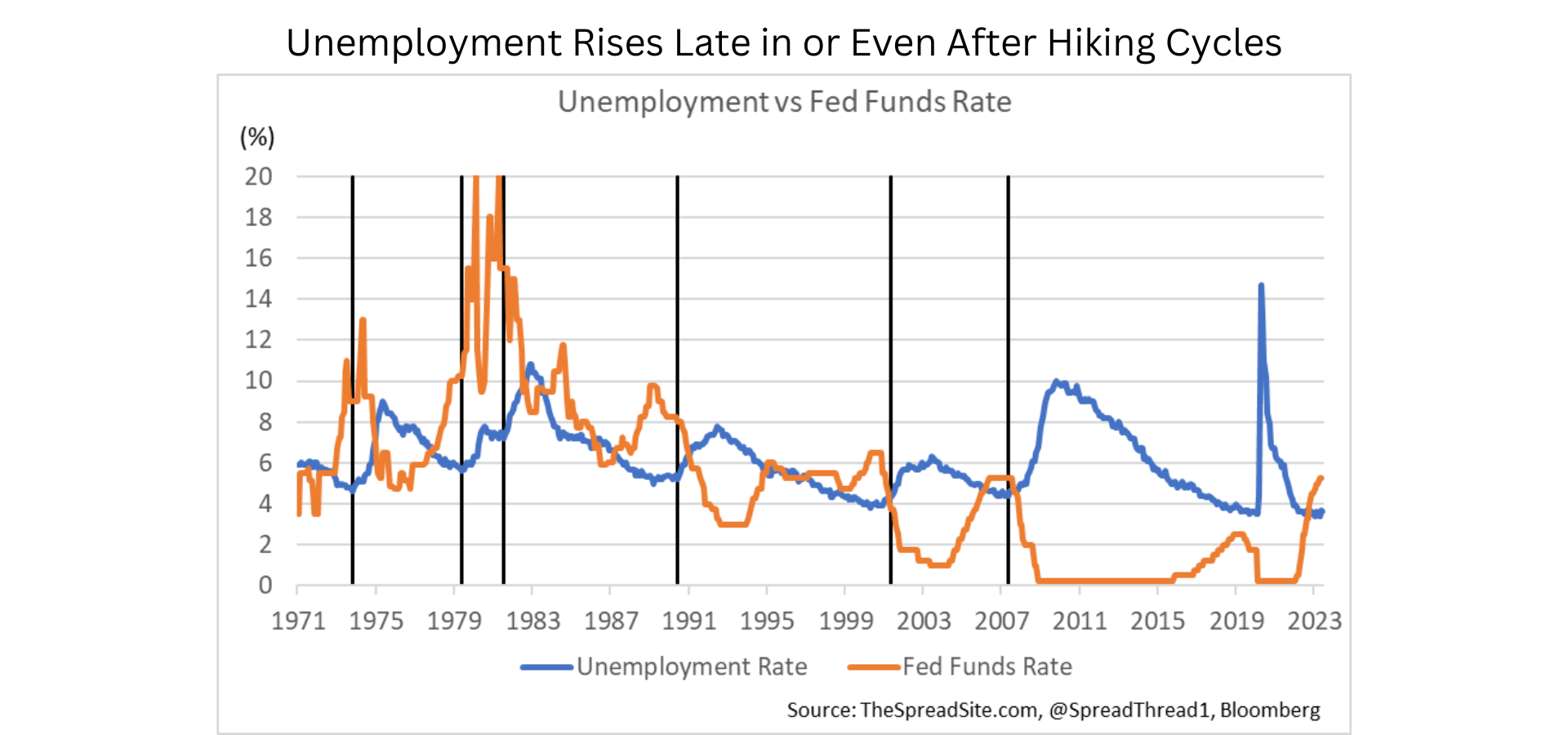

First, markets often correct around when the Fed begins raising rates. Yes, it is not always a 25% selloff like last year, but price action is typically weakest during fast rate hike cycles, and ~500bp in a year (plus QT) coming from a zero Fed Funds rate certainly qualifies as fast.

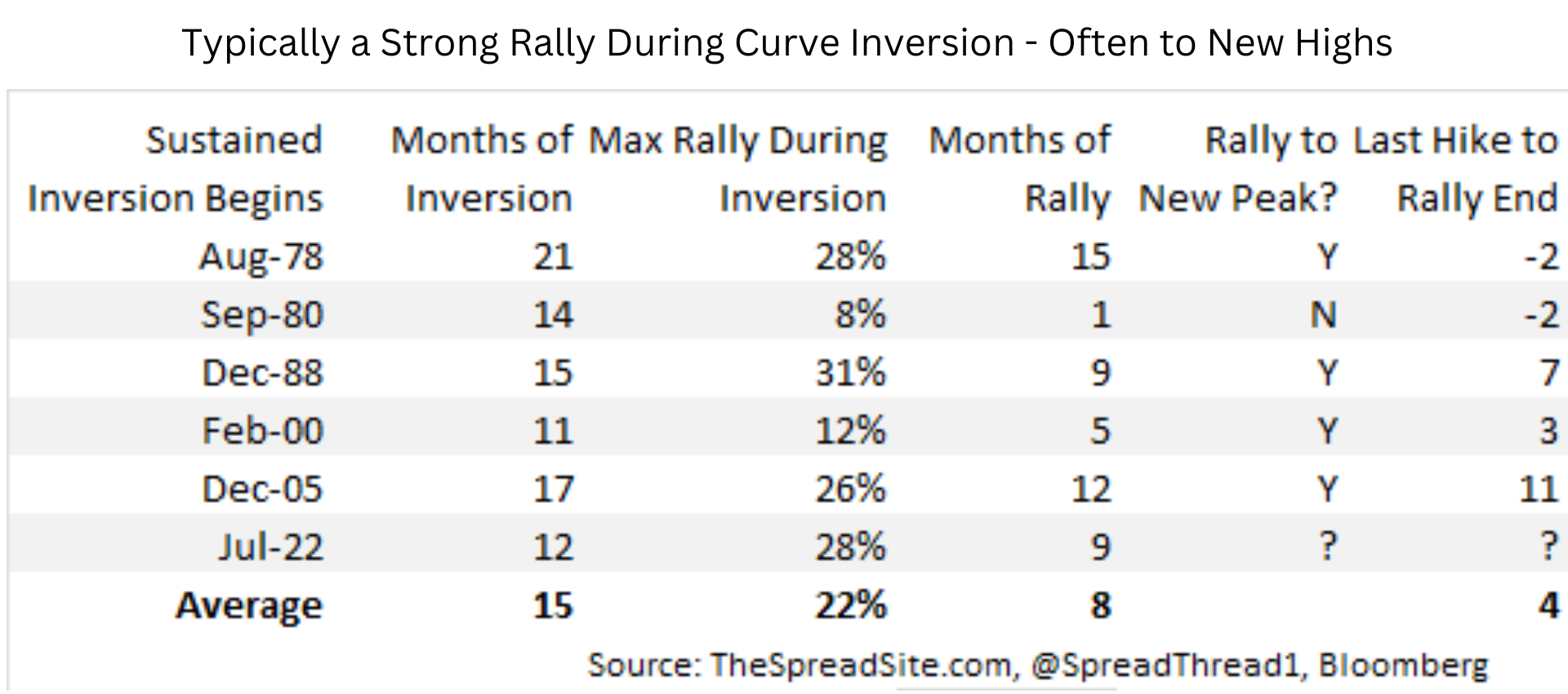

Second, as we have discussed on Twitter, many argue that because the Treasury curve inverted last year but the economy has held up, that this time is different – i.e., ignore the yield curve. We think that is a misinterpretation. An inverted yield curve does not tell you a recession is imminent. It tells you that policy is becoming restrictive, which usually means it is a late cycle environment, and naturally a recession often follows. But as some forget, there is significant variability between when the curve inverts and a recession begins, just like there is a lot of variability in how long a late cycle economy can persist. Importantly, just as we have experienced this year, markets almost always see a sharp rally while the curve is inverted, often to new cycle highs. In fact, this late cycle ‘melt-up’ is more the norm than the exception, especially in recent history.

In fact, even credit often does not give the warning far ahead of time that many believe, with spreads usually bottoming for a cycle not long before a recession begins. At the end of the day, publicly traded credit markets are sentiment barometers just like stocks.

Fundamentally, why do markets rally when policy is becoming tight and (in hindsight) a recession is getting closer? In our view, it is because the path from overheating to recession usually has to go through ‘goldilocks’ first. In other words, there is typically a period when rate hikes are nearly or completely done while jobs haven’t started rolling over that the market (prematurely) celebrates the Fed accomplishing the impossible, as we are witnessing today.

And while some feel vindicated that the economy skirted a recession in 2022, that was never a likely scenario. The hiking cycle didn’t even begin until March and unemployment lags, often by a long period of time. Even in the high-inflation cycles of the 70s/80s when the Fed hiked right into recession, unemployment did not begin rising until late in the hiking cycle. In more recent episodes, unemployment did not begin rising until well after the hiking cycle was done, which drove sizable ‘goldilocks’ rallies.

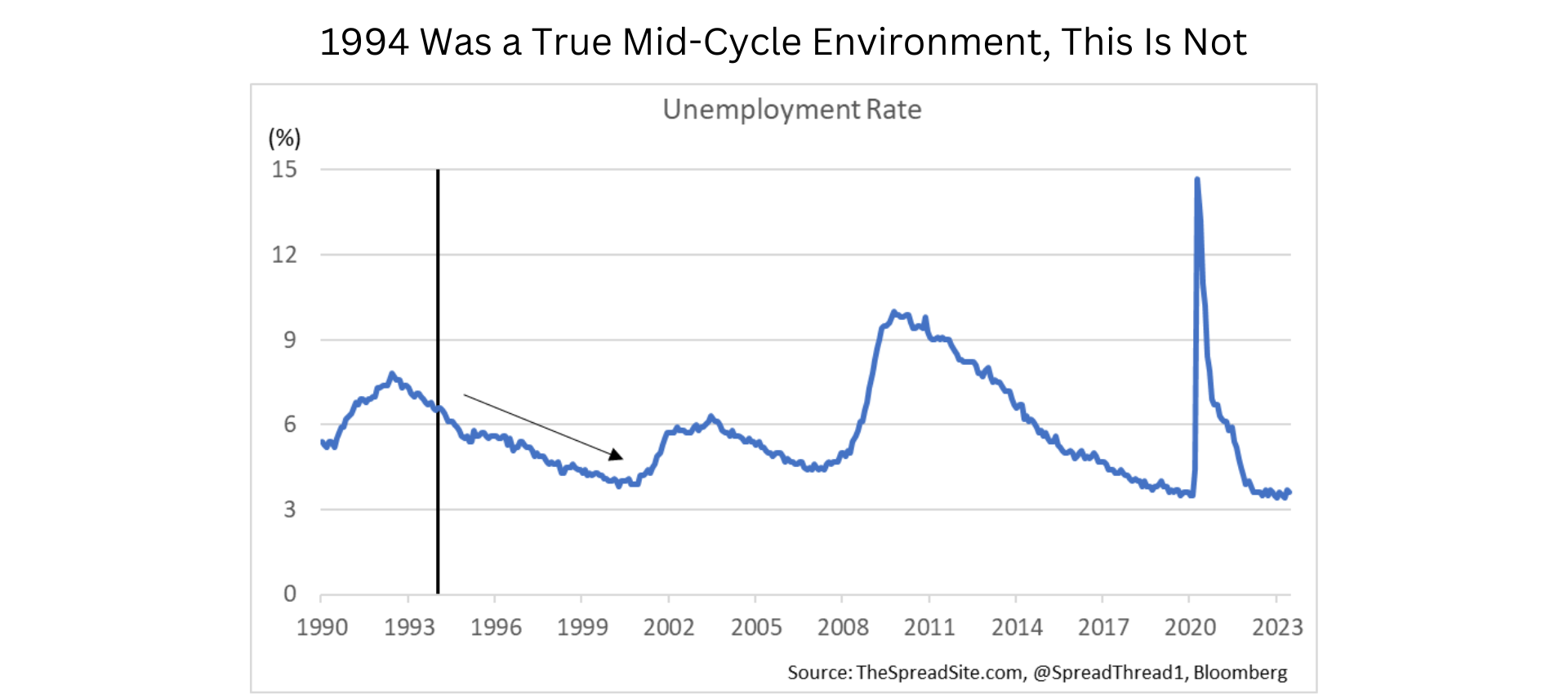

As a result, we believe this rally in markets is not the start of a new protracted bull market, but a typical late cycle melt-up that serves to drag investors into the pool, at the same time cracks build under the surface. Ultimately our view is supported by the countless market and macro datapoints that we continue to see (outlined in Cycle Through the Noise), which we believe are representative of a late-cycle economy nearing a turn, not what you would expect at the start of a new expansion or even mid-cycle slowdown. Remember, in the 1994 hiking cycle, one of the few true mid-cycle soft landings, unemployment was still not far from the prior recession peak, and able to decline for years as a result, very different than the situation today.

FOCUSING ON THE END GAME

We never underestimate how far bear-market rallies, overshoots, melt-ups, etc… can go, and that has influenced our recommendations all year. While we certainly did not expect or predict S&P 4550, we also haven’t been telling investors to pile into outright shorts. Most of our recommendations have been relative value trades with a defensive bias, or expressing shorts through put spreads, that if wrong, allow you to fight another day. We continue to have this mentality – focusing more on the end game, then trying to precisely time the turn, recognizing that the latter is in part a guess, and that there is no telling how extreme valuations can get in the short-term.

That said, valuations are already extreme, in our view. A ~20x p/e multiple on the S&P 500 (on forward earnings that are probably quite a bit too high, even in the bull case) and high yields spreads at 380bp, very much require Goldilocks to continue. Ultimately, the economy will likely break one way or another. As we have outlined, we think it breaks to the downside as a high cost of borrowing/ tight lending continues to bite, excess savings run out and student loan repayments kick in, among other headwinds.

We certainly could be wrong and do consider the risk that rising asset valuations drive renewed animal spirits and thus a temporary re-acceleration in growth. Even if that is the case, we think it does not change the end game, but just delays it, ultimately forcing an even more aggressive Fed. A true soft landing (i.e., 1994) is the outcome which would prove us wrong, and while that scenario is not impossible, we think it is a 20% probability, that is 80% priced.

The Spread Site Research

Receive our latest publications directly to your inbox. Its Free!.

{kind=link}