Cycle Through the Noise

SUMMARY

• In the following report, we lay out the progression of a typical credit cycle and how the market today fits into this analysis. While this cycle is clearly unique in many ways, the general pattern rhymes with history.

• Leverage/excesses built up due to low rates for a long time, the Fed hiked (this time rapidly) to slow the overheating, and credit conditions then began tightening, first slowly and now more quickly given headwinds in the banking system.

• The next step is for tighter credit conditions and weaker credit demand to filter into the real economy as companies and consumers pullback. This negative feedback loop is typically halted when the Fed finally panics. The risk is that they are slow to do so in this cycle given their intense focus on inflation.

• This process takes time to fully play out. Expect several large swings in sentiment along the way, like the 'soft-landing' rally markets are currently experiencing.

• Many detailed investment ideas to come in future reports. At a high-level we continue to believe: 1) Patience is key, especially with cash paying 5%. 2) Until a recession is clear in the data (and hence fully priced in) investors should prioritize quality and lower beta credit. And 3) this distressed cycle will create good opportunities – make sure you have the capital to invest as they arise.

INTRODUCTION

For the first publication on our new website (TheSpreadSite.com) we lay out an important framework of ours – the progression of a typical credit cycle and how the market today fits into this analysis.

As we show, we think the credit cycle is turning and will increasingly feed back into the economy, but the full process takes time and won’t happen in a straight line. In fact, it is not uncommon for markets to rally sharply and even make new highs while the yield curve is inverted. To avoid chasing during these 'all-clear' moments, it is crucial to understand the big picture.

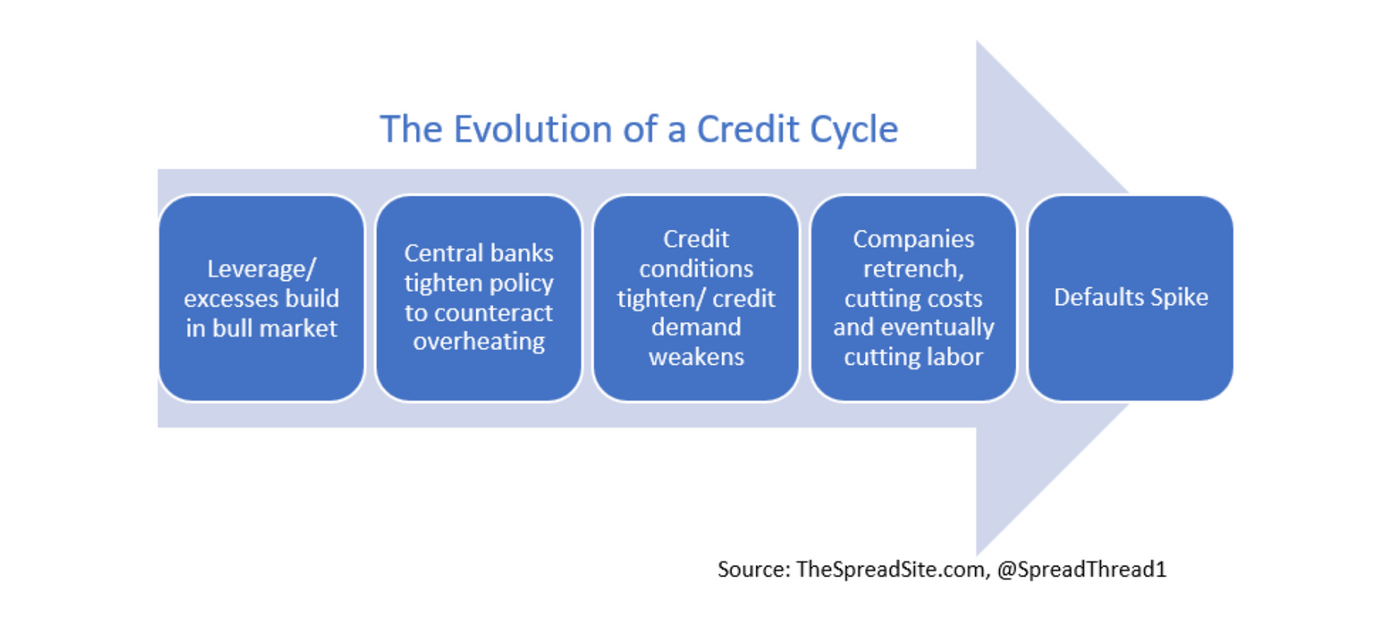

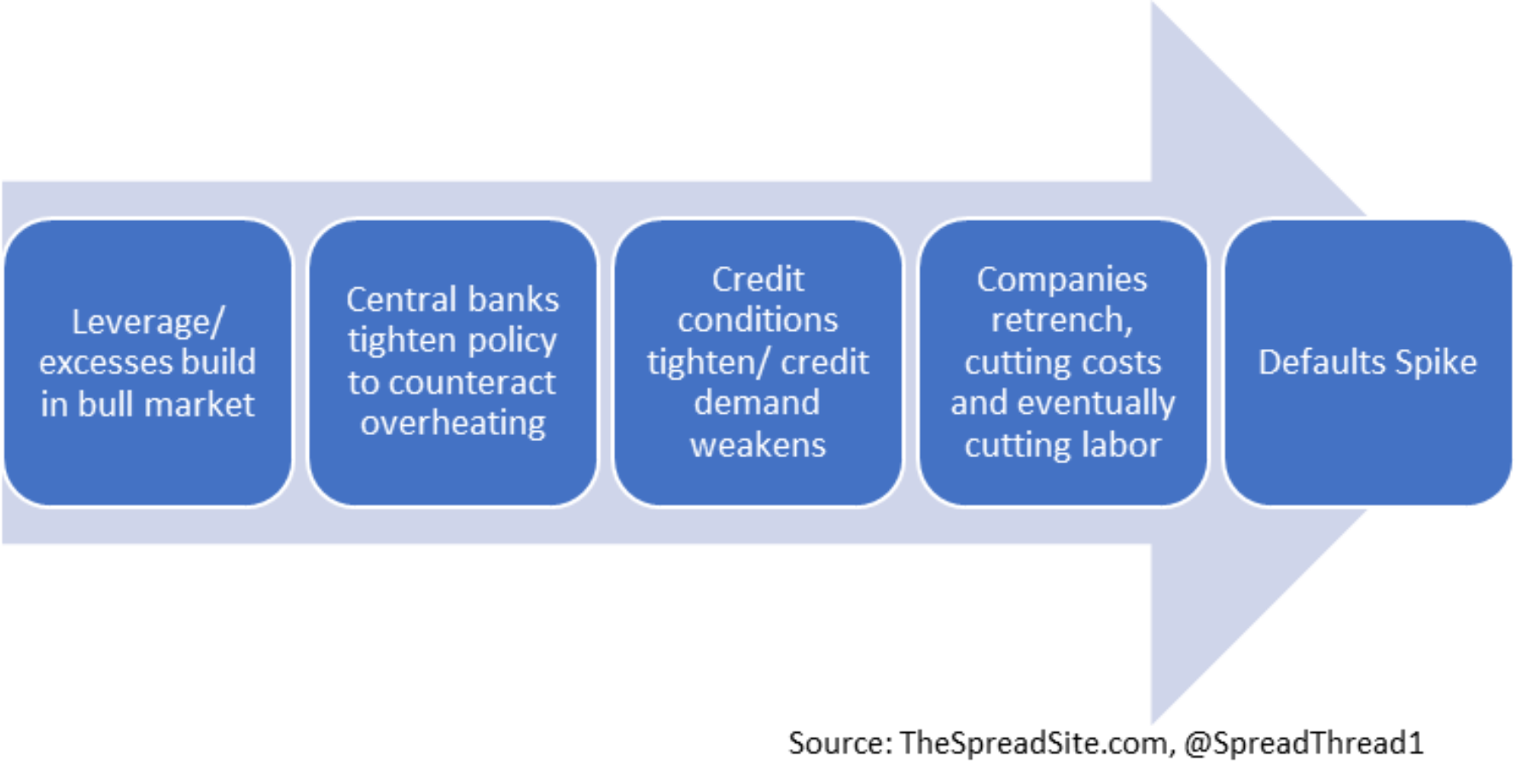

In short, our view is that credit cycles are always different to some extent from one to the next (different problem sectors, catalysts, drivers etc…) but the basic pattern is as follows:

Below we walk through each one of these steps in more detail.

Stage 1: Buildup in Leverage

In the years leading up to a default cycle, leverage/excesses build - not everywhere, but in enough places to matter. We think it is important to remember two points:

- The vulnerabilities in a cycle ALWAYS seem less severe ahead of time. In 2007, many saw growing problems in credit and subprime but the extent of the damage to come in financials and housing was only obvious to the consensus after the fact.

- Some problems are easy to spot in advance, but there are always ‘hidden pockets’ of leverage that are not clear until credit conditions tighten. For example, bubbles in crypto and high growth tech were reasonably obvious, but how many were talking about UK pension funds or US regional banks as a key source of risk a year ago?

In the current cycle, we are firmly in the camp that leverage and excesses have built up throughout the economy, driven by a decade of ZIRP, and will become more obvious as the credit cycle progresses. To give a few examples:

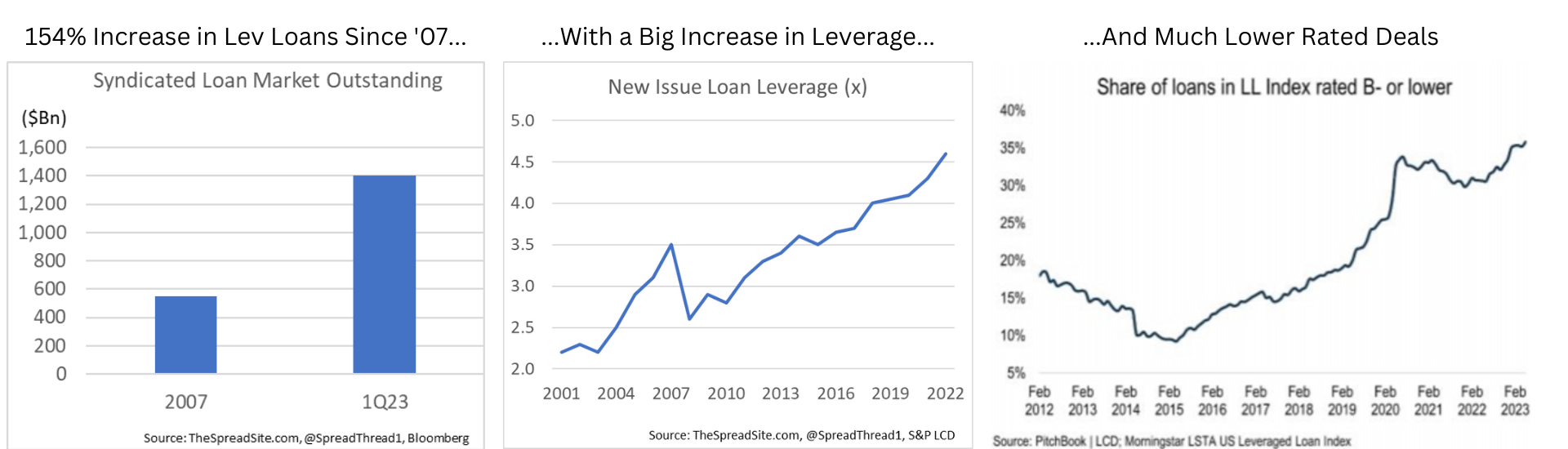

• Leveraged loans outstanding have grown by 154% since 2007 with a surge in lower rated loans, weaker structures, and higher leverage in deals.

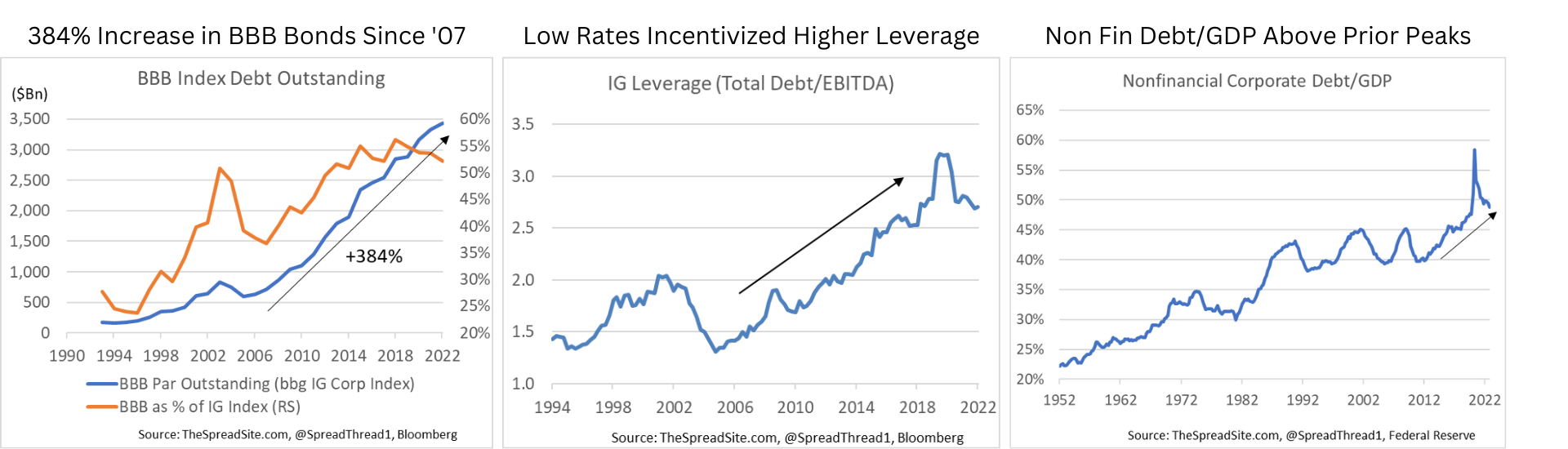

• BBB IG debt has increased by 384% since 2007. IG leverage is sitting at higher levels than prior to any past recession, as high quality companies were incentivized for years to issue extremely low yielding debt to buyback stock, for M&A, etc... The broadest measure of corporate leverage, non-financial debt/GDP is well above past cycle peaks (ex the brief covid spike in 2020).

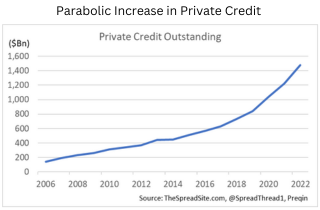

• Private credit has grown from next to nothing pre-crisis to $1.5 trillion today, as investors gave up liquidity for extra yield.

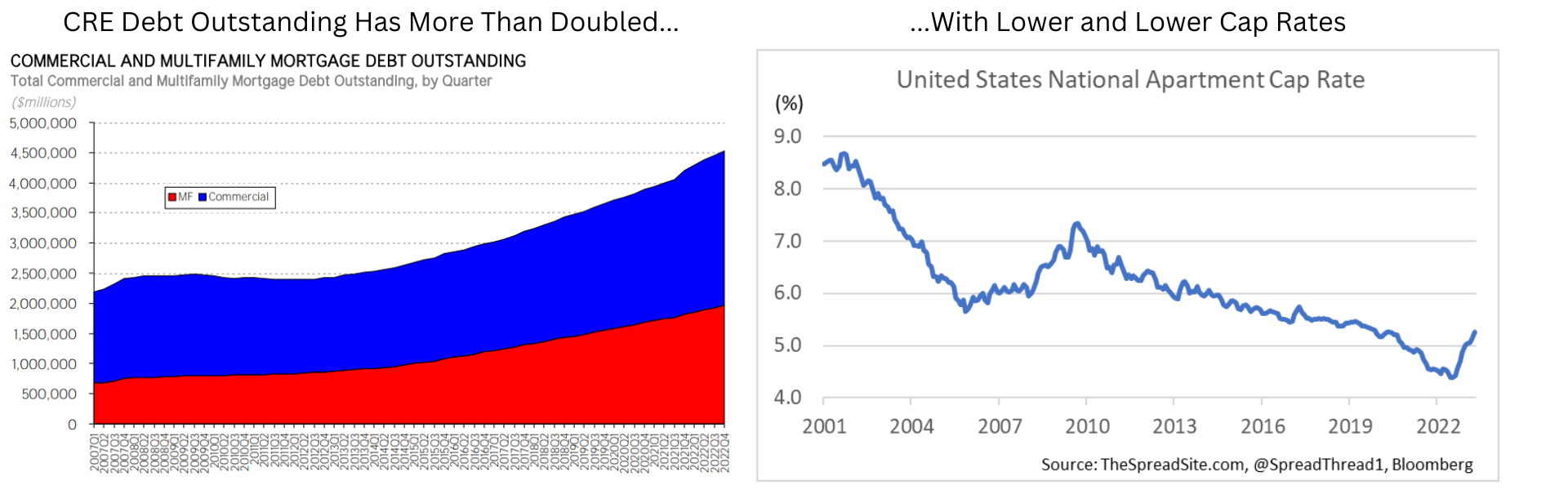

• Commercial real estate debt has more than doubled since 2007, with deals done at lower and lower cap rates because of such low-cost financing.

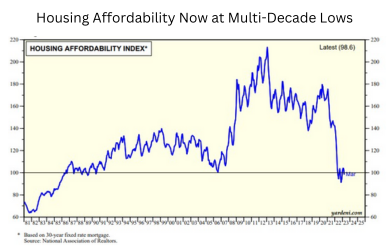

• Housing affordability is near multi-decade lows, again in part because buyers could justify higher home prices with such low borrowing costs.

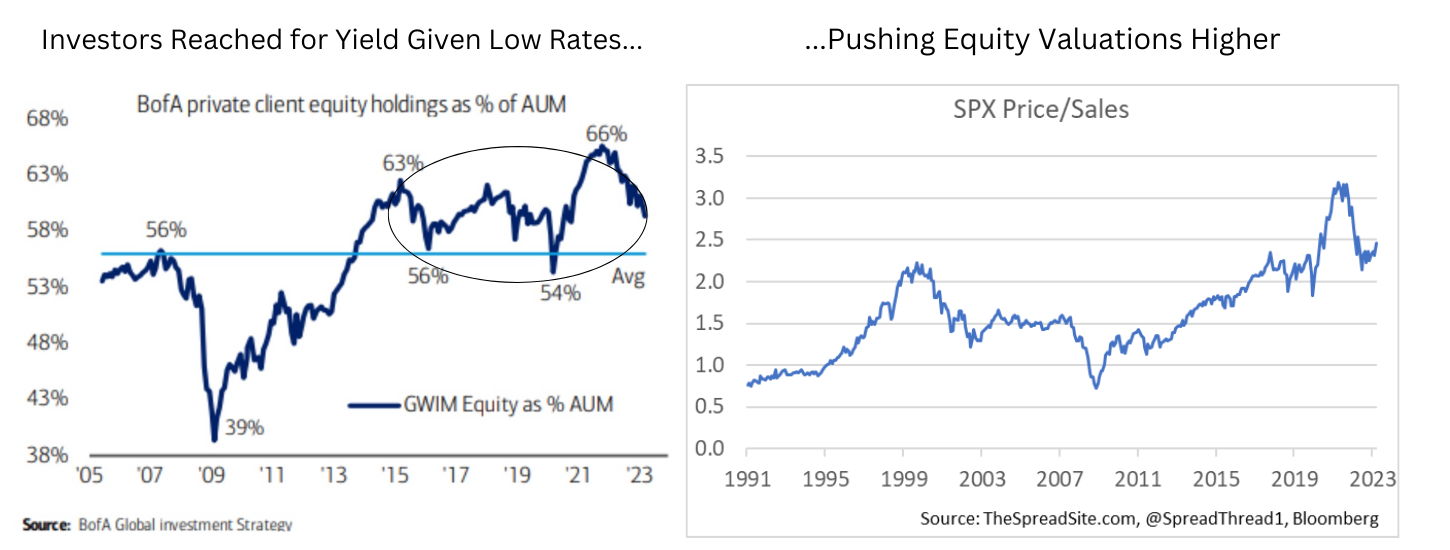

• Equity valuations were pushed to very high levels as investors, who had a harder time achieving a reasonable yield in fixed income, were pushed out the risk spectrum to generate returns.

• We could keep listing areas where excesses built up in the economy or markets given ultra rates – from crypto, to profitless tech, to venture capital, to private equity, to pockets of consumer borrowing – but you get the point.

To be clear, we are not claiming all of these dynamics are catastrophic by any means. But it is important to remember that balance sheets, consumer/corporate behavior, and the global economy as we know it today have all been highly shaped by extremely low rates for a very long time.

Stage 2: Central Bank Tightening

Next central banks begin to raise rates, in some cycles to stem the overheating, in others simply to normalize policy. Either way, markets often do fine during this stage because the economy is still ok and earnings are still holding up.

To state (what should be) the obvious, it always takes time for rate hikes to filter through. First, not all consumers and corporates have to make large investments or finance new purchases right away. Second, companies have cash buffers and ways to offset the initial rate shock. And third, as long credit is still available to levered borrowers, (which is usually the case until late in or even after a rate hike cycle), problems can be pushed out.

But make no mistake, shocking a levered system, that has been this reliant on cheap debt for this long will have an impact, even if the process is slower than some expect.

And the idea that corporate America is not rate sensitive because companies have locked in low cost financing is not fully accurate. Yes, large, high quality companies benefit, in this regard, in many cases. But remember, most small and mid-sized companies don't have access to public bond markets. Adding it all up, approximately 30% of non-financial corporate debt is tied to short-rates in one form or another and about 10-15% of fixed rate debt will need to be refinaced over the next year. Most importantly, the growth in leveraged finance debt in this cycle (which carries the highest default risk) has come predominantly from the leveraged loan and private credit markets - both floating rate asset classes.

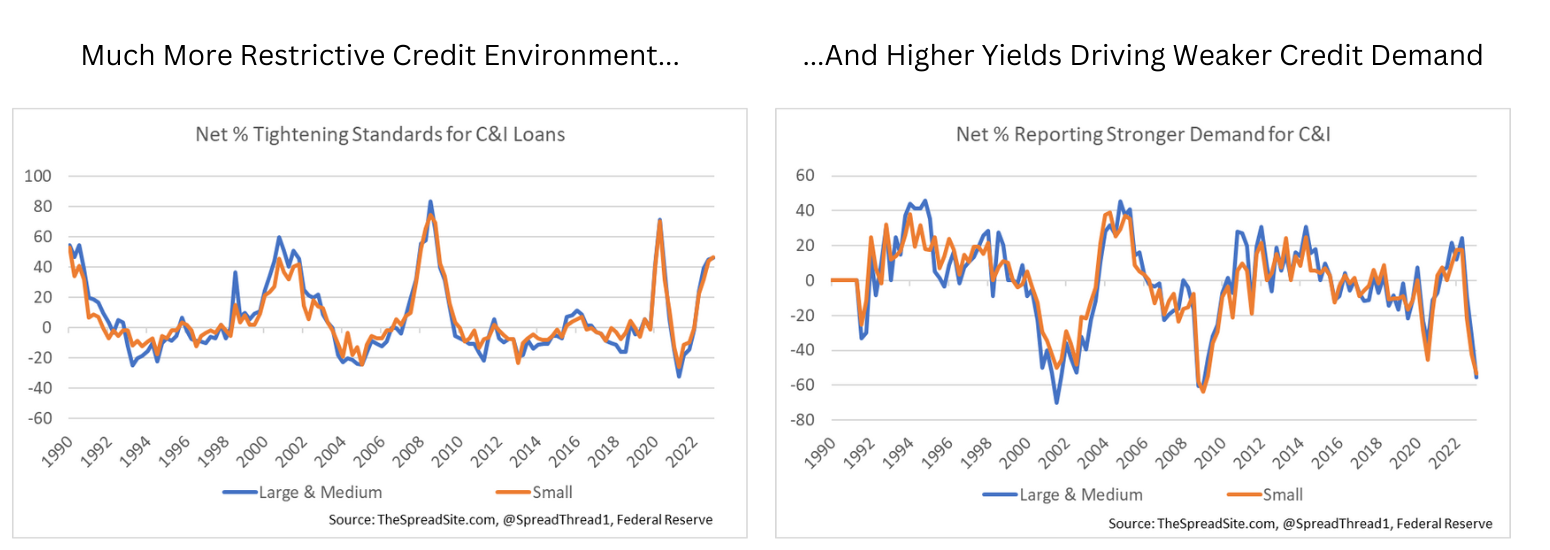

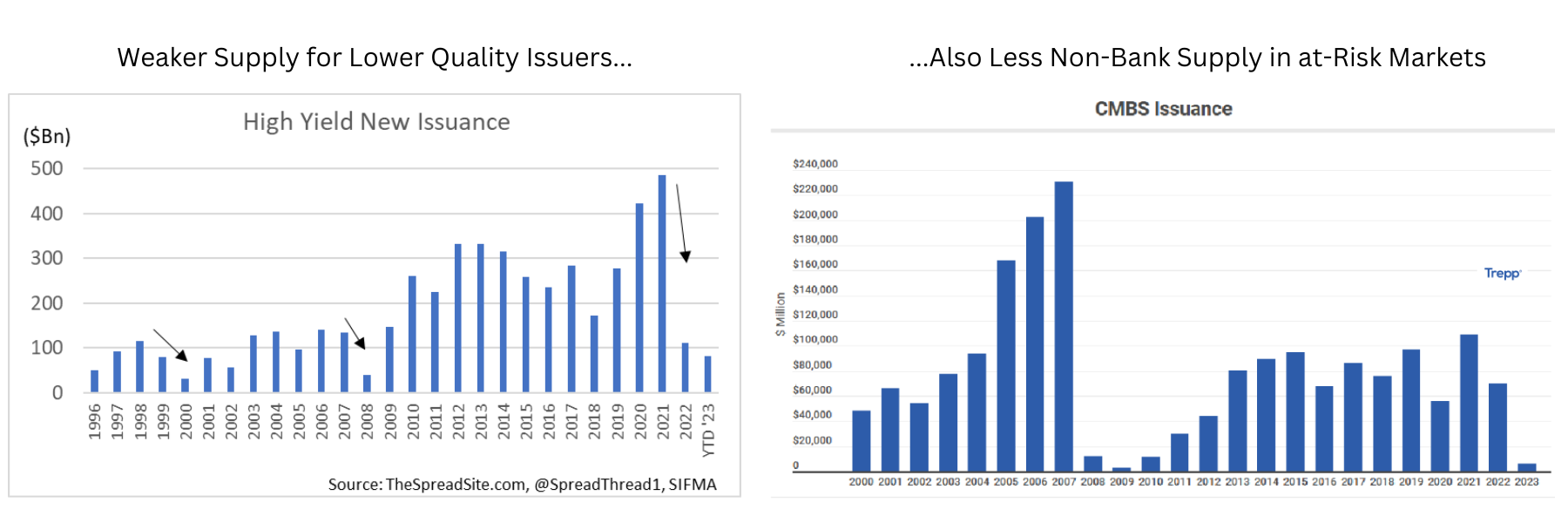

Stage 3: Credit Conditions Tighten

With rate hikes feeding through the system, credit conditions eventually tighten as banks start to feel pain from an inverted yield curve, credit issues begin to pop up, and the economy starts to soften. In other words, those who need to borrow have a tougher time doing so, and those who don’t need to borrow can do so, but at a higher cost. So both the supply of credit is restricted and the demand for credit drops, like we are seeing today.

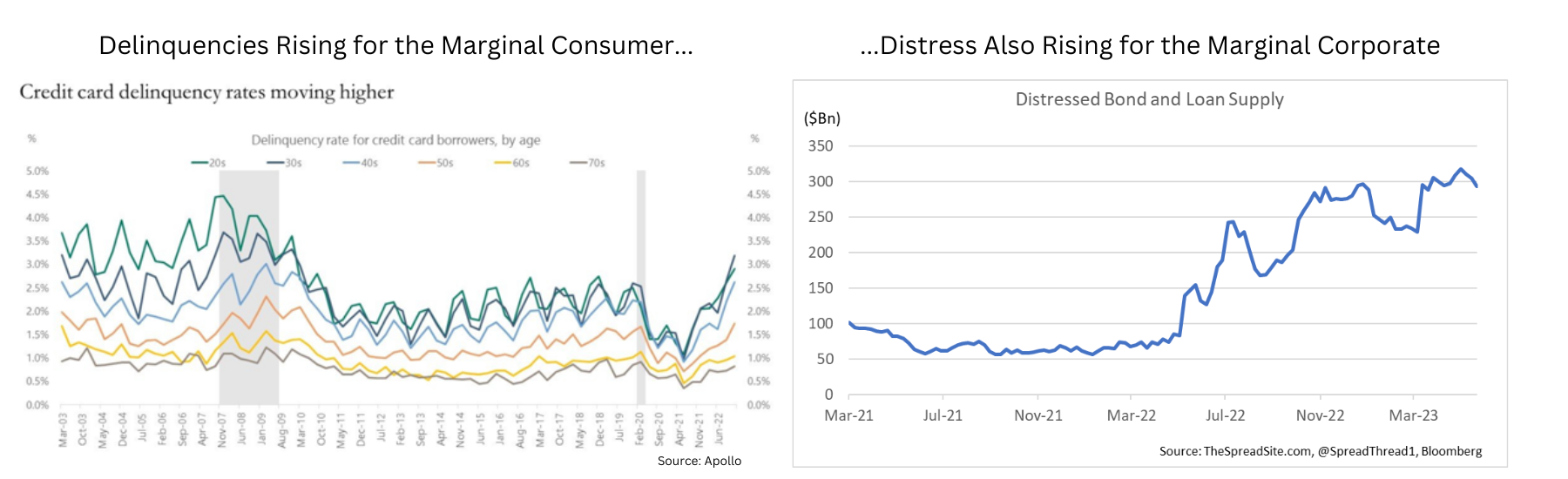

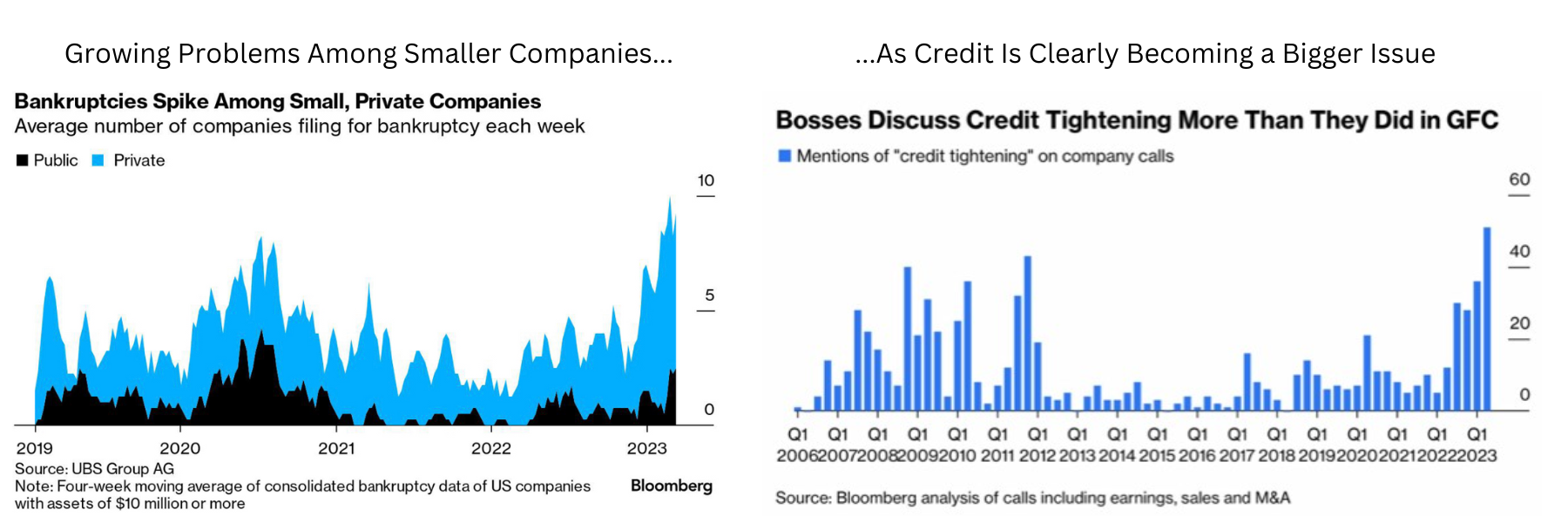

At this stage credit issues are often popping up under the radar, but are mild enough that the consensus will write them off as “normalizing” – for example, rising consumer delinquencies, a widening in spreads for low quality credit, lower issuance for levered borrowers, increased distressed debt outstanding, a rise in defaults for smaller companies, companies noting that tighter credit is impacting business – all dynamics we are also starting to see.

And remember, initial signs of stress are not always going to be blatently obvious - that would be too easy. But when CRE debt can't get rolled in many cases and levered corporates are struggling to renew revolvers/ extend loans or paying rates in the teens to do so, investors should be on alert that the credit cycle is progressing.

We think this stage is important for three key reasons.

- High and rising leverage doesn’t matter (often for years) until vulnerable companies lose access to credit. In this sense, tighter credit conditions is the catalysts for stress to spread.

- The timing of acute credit events is hard to predict, but as we saw this past spring with the regional banks, when rates are high and credit is tight, the risks of those shocks goes up by an order of magnitude.

- Tighter credit and higher borrowing costs drive a negative feedback loop, by impacting corporate and consumer behavior, as we discuss below.

Stage 4: Companies Retrench

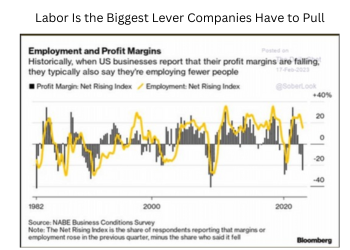

This next stage, which we think markets are soon entering, is the negative feedback loop from credit to the economy back to credit back to the economy. In other words, corporates and consumers cut back at the margin – in some cases because they want to (it is more expensive to finance new capex/spending) in other cases because they have to (for example, regional banks reducing lending to build capital).

The cost cutting always begins with low hanging fruit, but eventually leads to jobs if it gets bad enough, because labor is the biggest lever available for corporates to pull. This retrenchment weakens the economy and thus earnings, which pushes corporate leverage even higher (the denominator in debt/EBITDA drops). As a result, credit quality weakens further, bank portfolios deteriorate/ non-banks suffer portfolio stress, which leads to more credit tightening and more cost cutting.

Along these lines, in a recent Fed Notes (6/23/23) titled "Distressed Firms and the Large Effects of Monetary Policy Tightenings" the authors (Ander Perez-Orive and Yannick Timmer) note: "The strength of the transmission of monetary policy depends on the aggregate distribution of firm financial distress" and "The recent policy tightening is likely to have effects on investment, employment, and aggregate activity that are stronger than in most tightening episodes since the late 1970s."

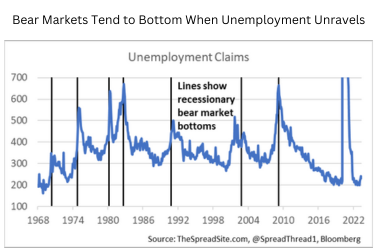

As unemployment claims shoot higher, bear markets often take their last leg down, which is the market’s way of pushing policy makers to finally break this vicious credit cycle, in part through lower rates.

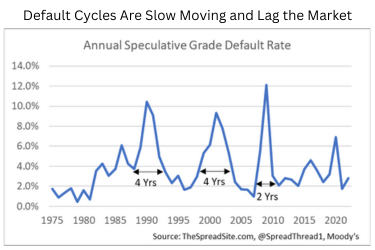

Stage 5: Defaults Spike

The last stage in a credit cycle is a broad-based rise in defaults. But remember, defaults take time to materialize - a bond may sit in distressed territory for a year or more before it finally defaults. And as a result, default cycles can take a few years to fully play out, usually ending well after a new credit bull market has already begun.

Conclusion

While this cycle is unique in many ways, the general pattern clearly rhymes with history. Leverage/excesses built up due to low rates for a long time, the Fed hiked (this time rapidly) to slow the overheating, and credit conditions began tightening, first slowly and now more quickly given headwinds in the banking system. The next step is for tighter credit conditions and weaker credit demand to filter into the real economy as companies and consumers pull back. This negative feedback loop is typically halted when the Fed finally panics. The risk is that they are slow to do so in this cycle given their intense focus on inflation.

Of course, this process takes time to fully play out. Expect several large swings in sentiment along the way, like the 'soft-landing' rally markets are currently experiencing. We will have many detailed investment ideas to come in future reports. At a high-level we continue to believe: 1) Patience is key, especially with cash paying 5%. 2) Until a recession is clear in the data (and hence fully priced in) investors should prioritize quality and lower beta credit. And 3) this distressed cycle will create good opportunities – make sure you have the capital to invest as they arise.

Disclosures

Please click here to see our standard Legal Disclosures

The Spread Site Research

Receive our latest publications directly to your inbox. Its Free!.

{kind=link}