Financial Conditions Tightening

Summary

-

The key question today: Was growth in 3Q23 a temporary bounce in a bumpy late-cycle economy, or a more durable re-acceleration? We remain in the former camp and think markets are also looking beyond 3Q with economically-sensitive sectors hit hard since late July. Ultimately it comes down to how much you believe this recent surge in rates matters. We think a lot.

-

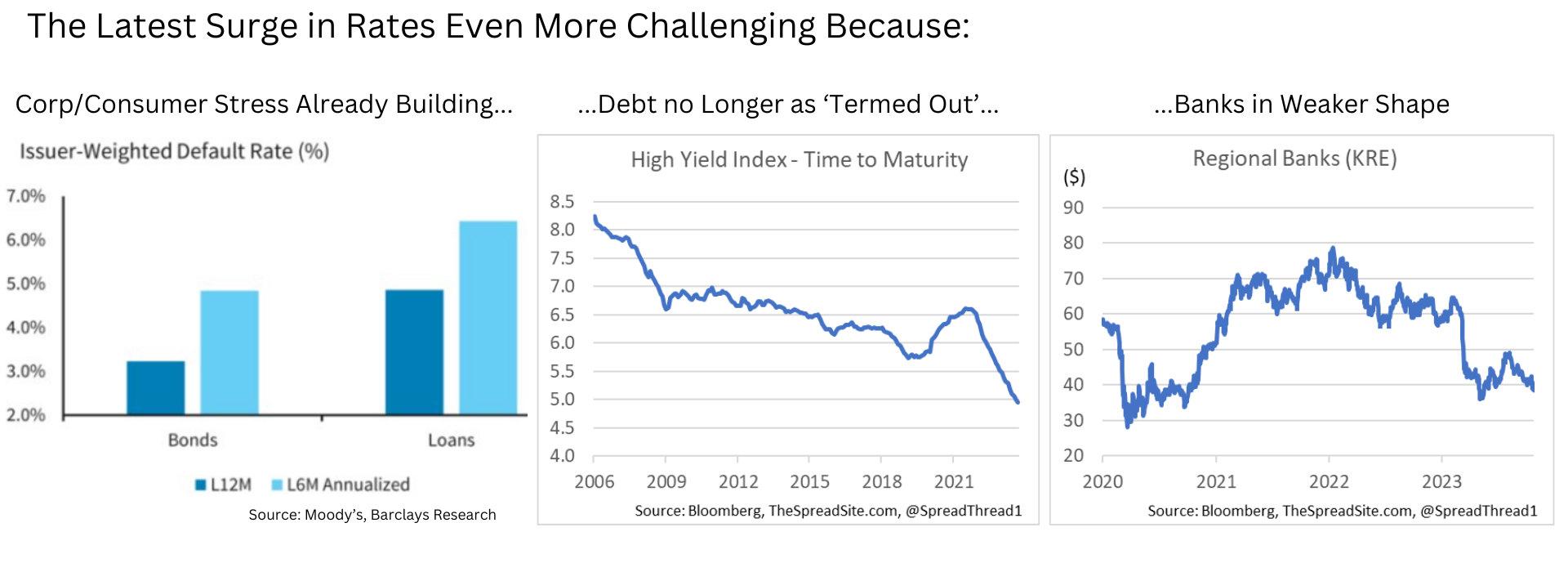

The rate rise in 2022 was easier to handle, because the economy had a bigger “buffer.” That is changing. Now rates are surging with consumer delinquencies beyond ‘normalization,’ more debt needing a refi, banks in a weaker position, and the jobs market starting to soften. This dynamic is exactly why a late cycle bear steepening can be so painful. Watch for the bull steepener to signal more imminent risks.

-

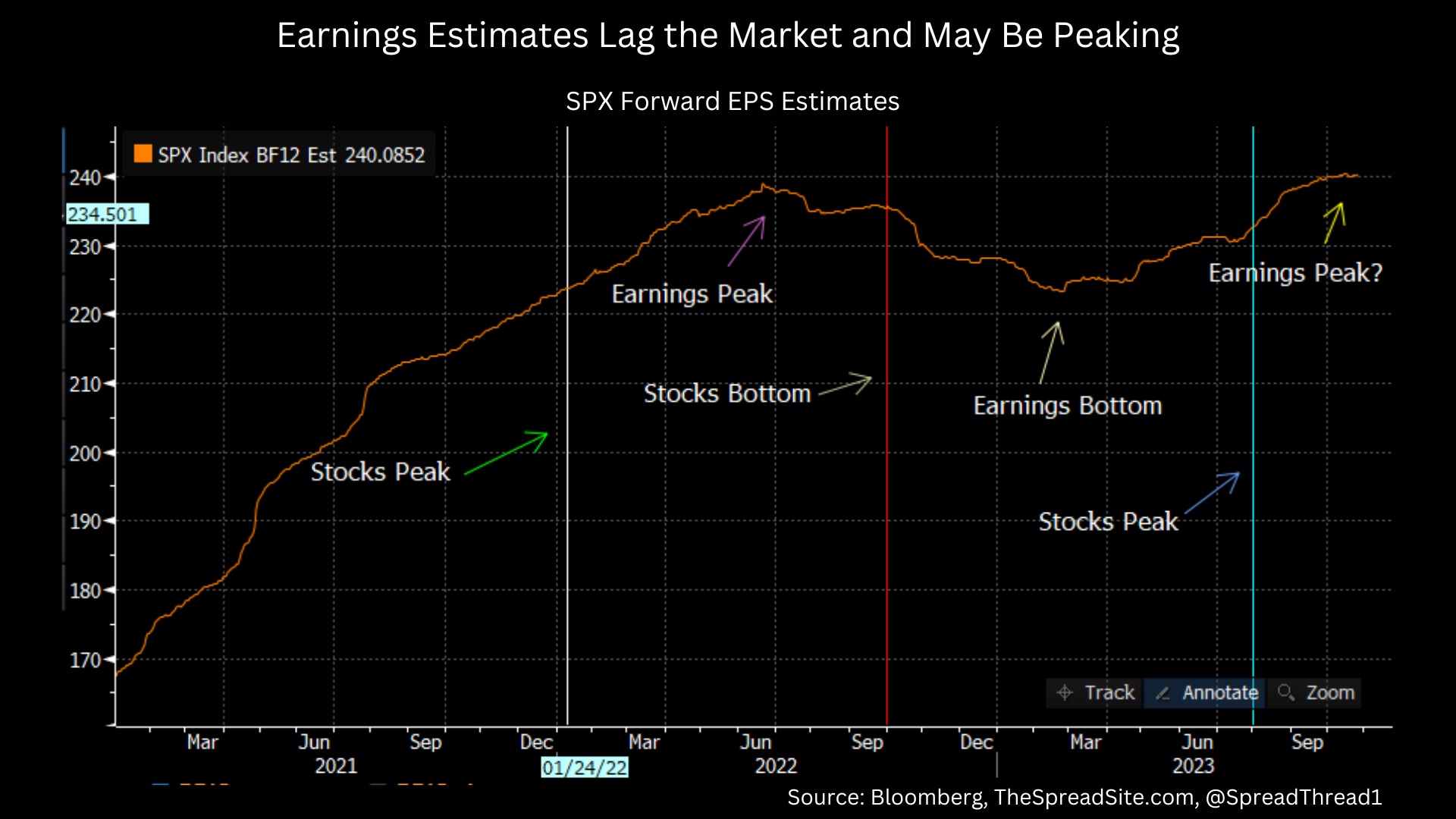

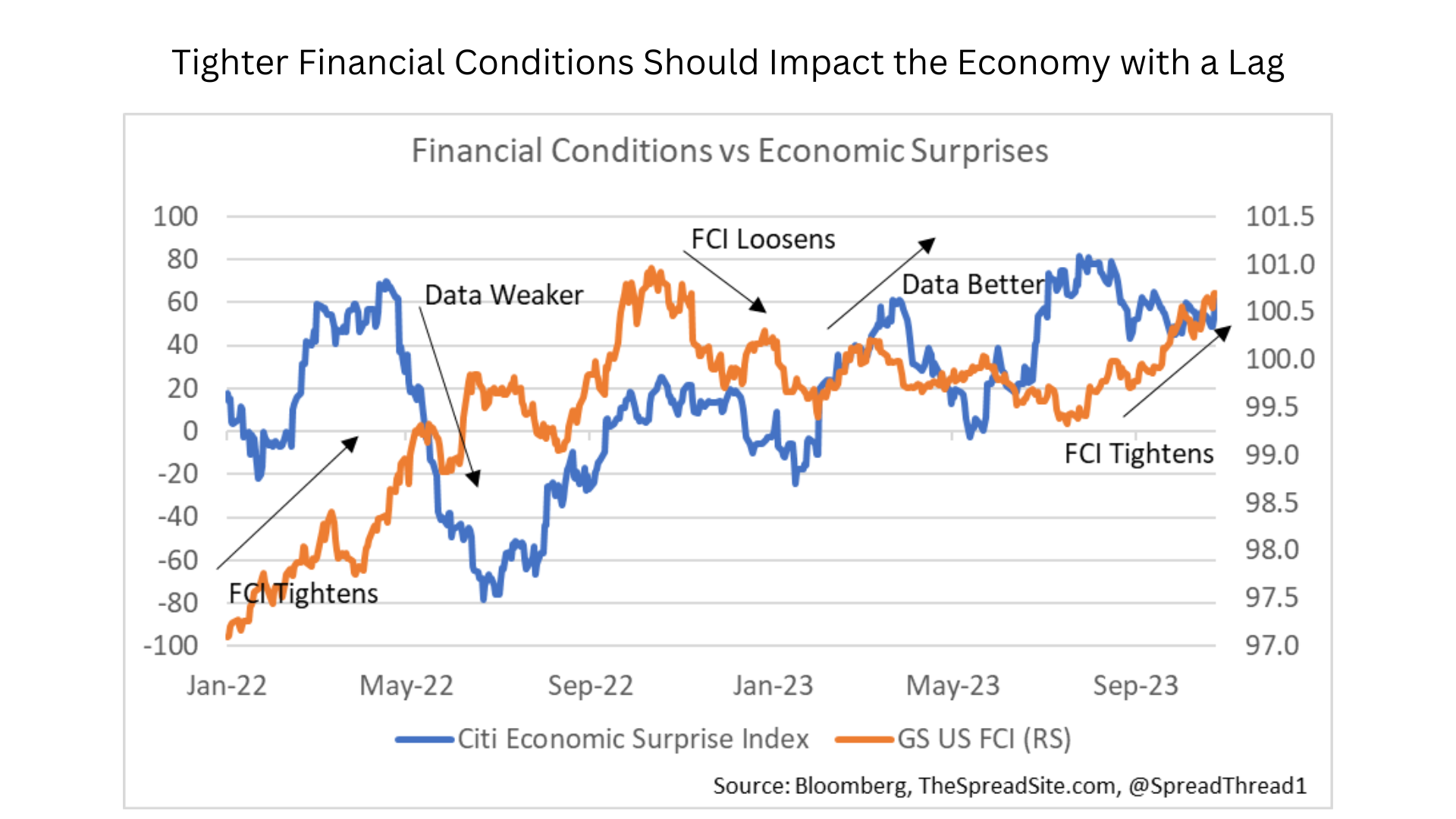

On timing, moves in financial conditions have led macro data surprises. With the sharp tightening in financial conditions over the past two months, on top of very strong 3Q GDP, conditions are ripe for downside macro surprises over the next two quarters. We think EPS estimates may be peaking, lagging the top in stocks by a few months, with earnings revisions breadth now rolling over.

-

Some of the most beat-up areas of the market (cyclicals, small caps) do offer more value. They are probably due for a bounce. For investors we think it’s too early for that trade. We are still sticking with quality/ defensives. For example, we think long duration IG at ~6.5% is very attractive for long-term, total return focused investors.

Peak Growth

After a brief period of calm this summer, volatility is clearly back, with the VIX hovering near 20, driven by an even sharper increase in interest rate vol. Sentiment around macro data has also been volatile, with this week’s 3Q23 GDP release of 4.9% feeding the narrative of booming growth. The key question: Was last quarter a temporary bounce in a bumpy late-cycle economy, or a more durable re-acceleration?

We have argued the former, and remain in that camp. Clearly large government deficits have offset the headwind from Fed tightening this year. But we think other temporary factors helped as well. Financial conditions eased and markets rallied throughout the first half of the year, boosting sentiment across the board. Falling interest rates supported a re-acceleration in housing activity. And large one-offs (Barbenheimer/Taylor Swift tour, etc…) contributed to a jump in consumer spending.

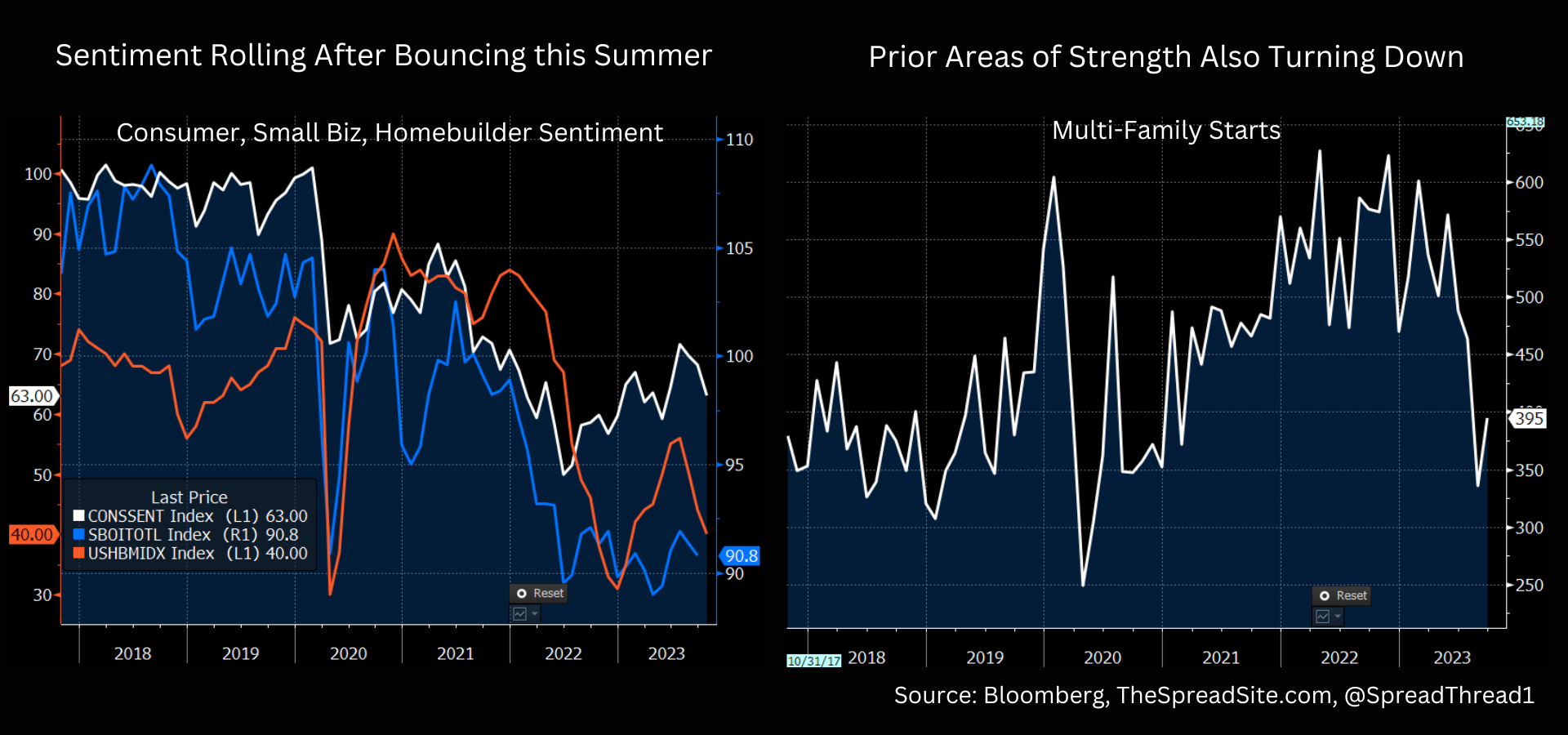

In our view, headwinds are going to start to overwhelm. First, many of the areas of the economy that bounced this summer are turning down. For example, consumer and small business confidence is rolling over after a brief jump this summer. Homebuilder sentiment is also rolling over. Second, other areas that held up better as the economy was weakening last year are now softening, with multi-family construction just one example. Third, new challenges are hitting, like student loan repayments, just as consumer stress is becoming more apparent. Fourth, the boost from a growing deficit will be no where as large in 2024 as it was in 2023.

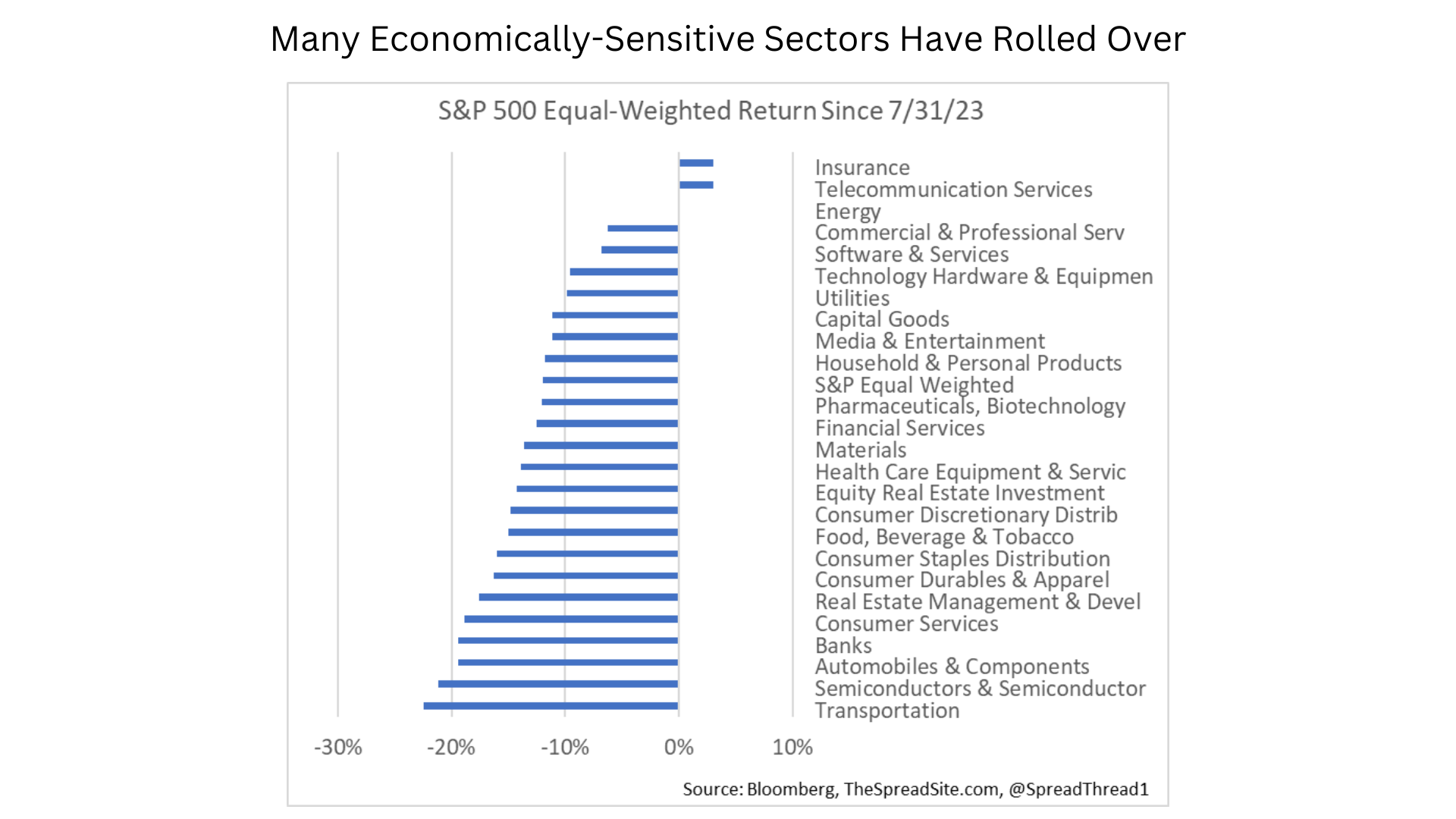

Last, and most importantly, the issues noted above are mostly before the surge in interest rates and associated tightening in financial conditions occurring over just the past two months, which some economists estimate is equivalent to an additional three Fed rate hikes. We think markets are looking past 3Q GDP growth, towards the weakness to come, with economically sensitive sectors like Transports, Consumer Cyclicals, Banks, Consumer Lenders, and Small Caps getting hit hard since late July.

Borrowing Costs Have Surged

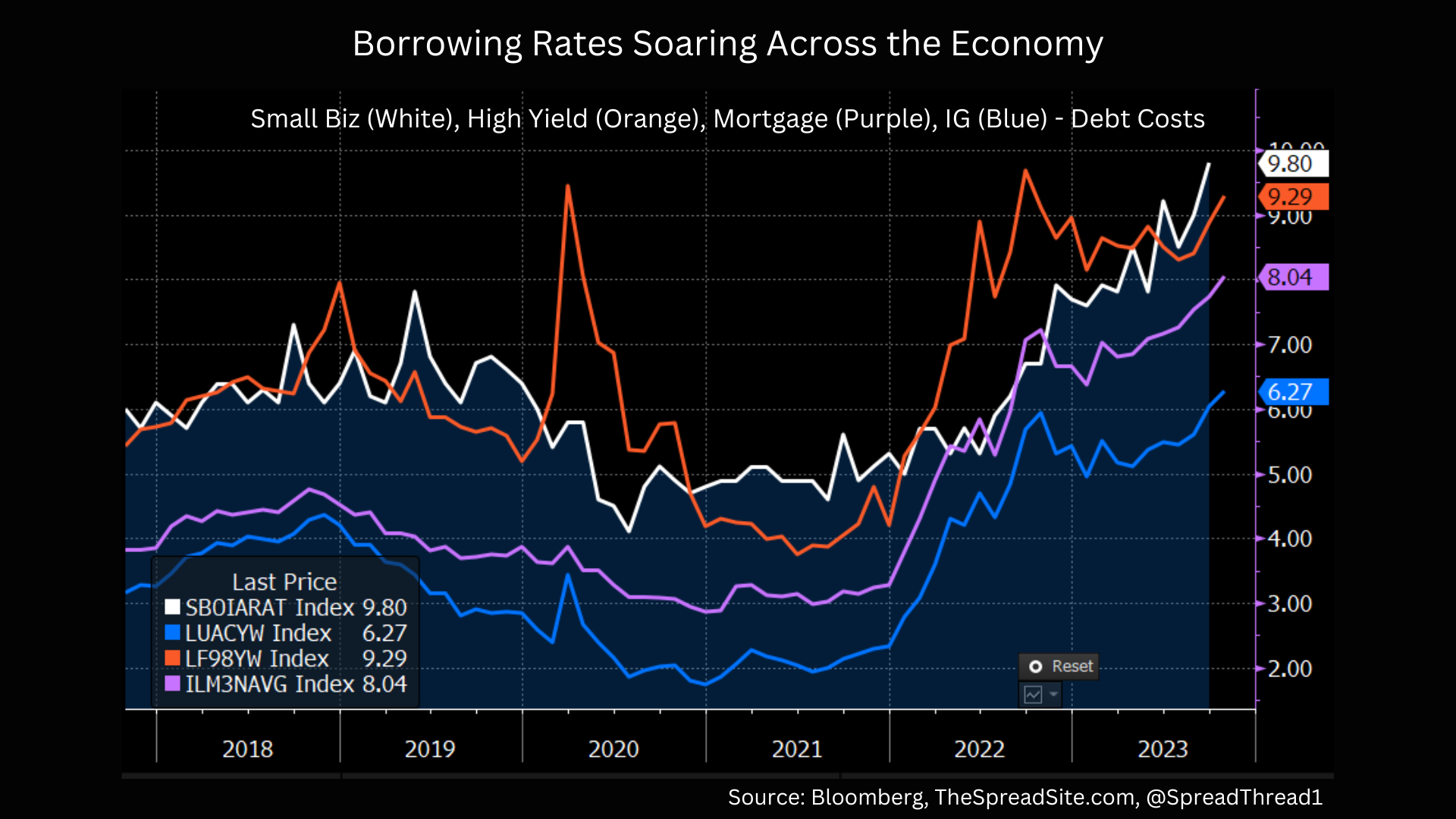

Whether we are correct on our macro view largely comes down to how much this recent rise in interest rates matters for markets and the economy. We think it matters a lot.

We often hear the argument that a 5% interest rate is not that high in the grand scheme of things – that rates were higher in the late 90s, as an example, a period of strong economic growth. In other words, the economy can handle it. Putting aside key differences between now and then, we think this comparison misses two important points. First, rates were high in the 90s, but trending lower over most of the decade - very different from today, when borrowing costs have surged over a very short period, across the economy, and after a decade of ZIRP.

Second, as we have argued, the only reason current rates are manageable is because most of the economy is not feeling these borrowing costs. In other words, an 8% mortgage rate is only fine because most consumers are locked in at 3%, but that is slowly changing as time passes.

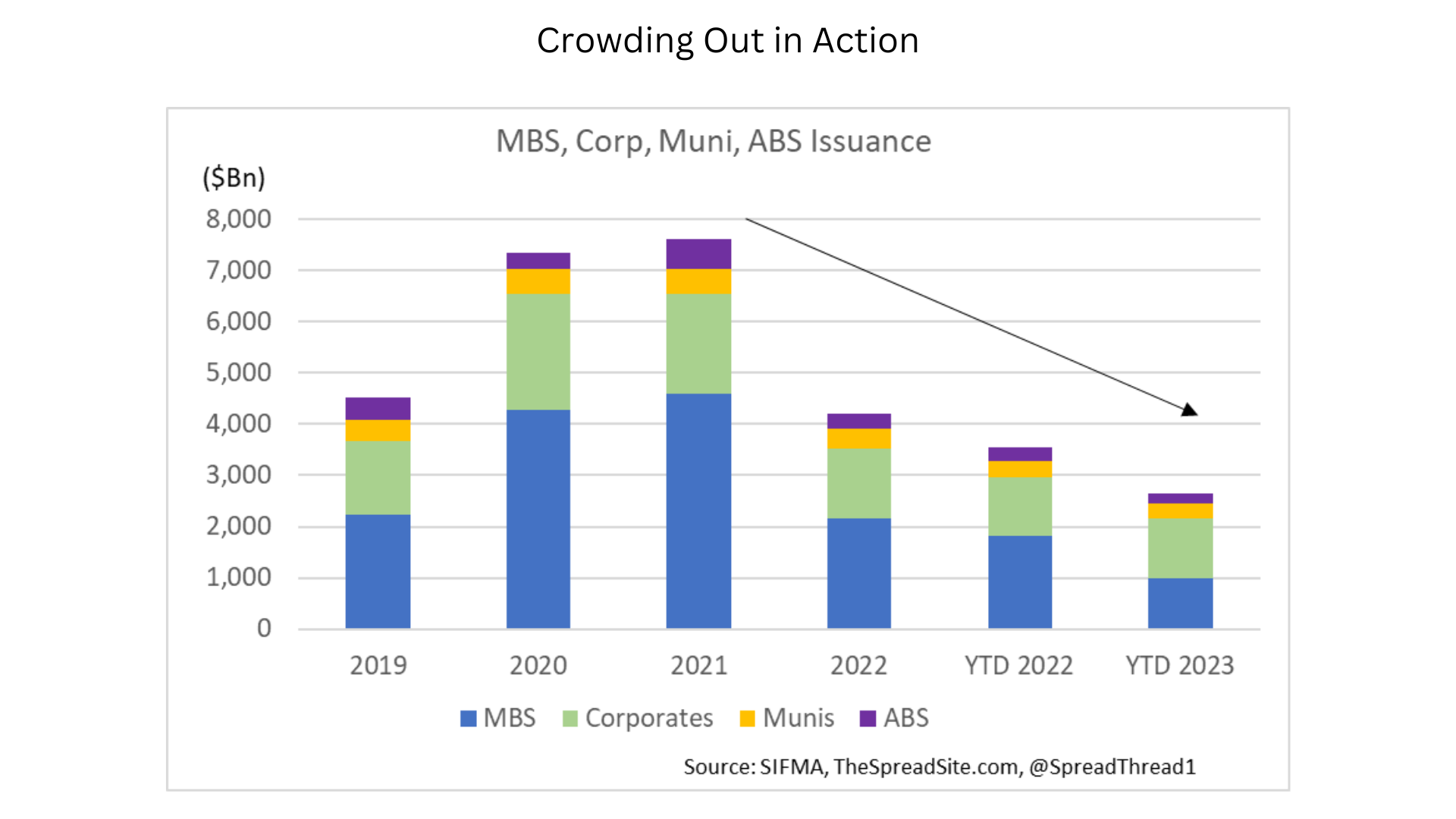

In our view, the increase in borrowing costs was already starting to bite with bonds at 3.5-4%, and in a matter of weeks, rates are up another 100bp. Where can we see the impact? First, delinquencies, defaults, and bankruptcies are rising across the board. Rising rates and tighter lending conditions are predominantly the culprit because unemployment is still low (at least for now). Second, outside of Treasuries, other key fixed income markets have seen a meaningful reduction in issuance volumes over the past two years – i.e., crowding out. We think this continues in a big way for non-financial corporates in 2024 (our main area of expertise). In other words, when it becomes more expensive to borrow, the private sector borrows less, which translates into less spending, investment, stock buybacks, real estate activity, etc…

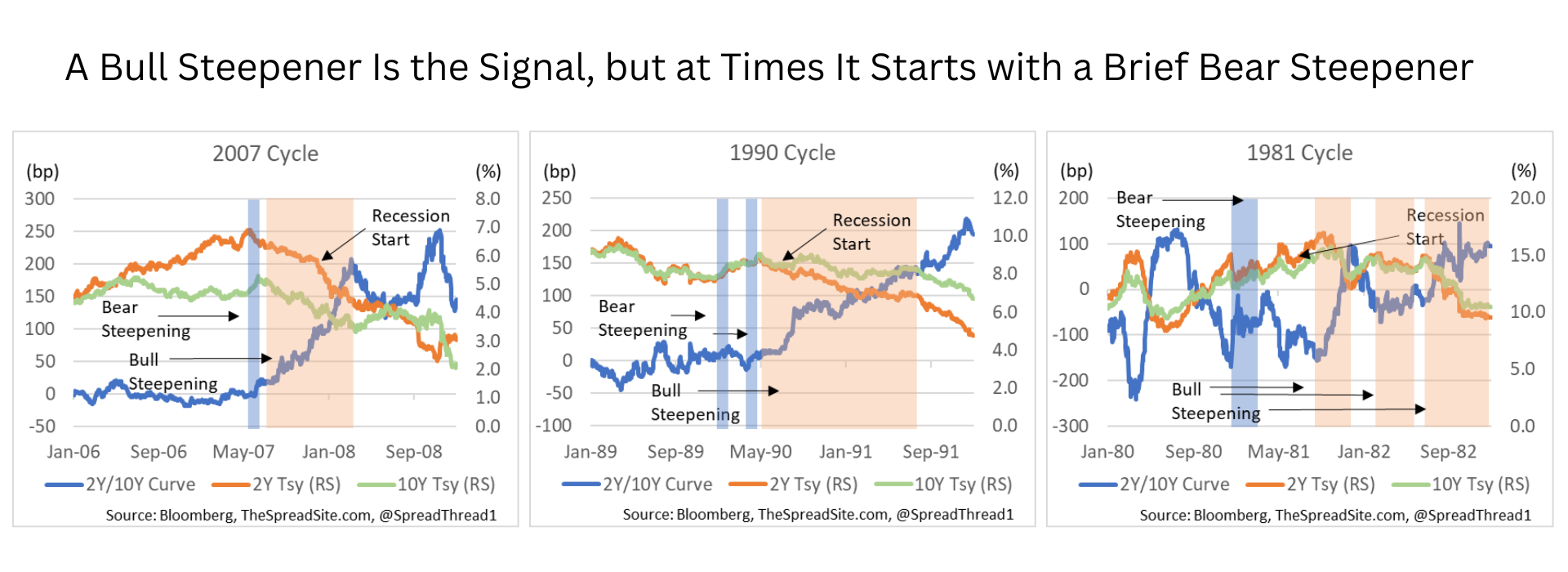

And importantly, we think the initial rate rise in 2022 was easier to handle, because the economy had a bigger “buffer.” Consumers had excess savings, defaults were low, it was easier for companies to ‘wait it out’ in hopes for lower rates to come, etc… But that is changing. Now rates are surging with consumer delinquencies already beyond ‘normalization,’ the time to maturity on lower coupon debt shrinking, banks in a weaker position, and the jobs market starting to soften. This dynamic is exactly why a late cycle bear steepening can be so painful – the straw that breaks the economy’s back.

Next Steps in the Process

The stock market has finally reacted to the sharp selloff in bonds, though until very recently, we could argue the selloff in equities has been modest. That said, a market down ‘only’ ~10% from recent highs masks quite a bit of weakness under the surface, especially in economically-sensitive sectors, as noted above. Ultimately, for stocks and credit spreads to react in a bigger way, we still think markets need to see the impact of higher rates. In other words, while growth is holding up it is easy for investors to sweep the ‘cracks’ under the rug. Once expectations shift from 12% EPS growth in 2024 to -12%, that changes. And it especially changes if the Fed is slow to respond to a weaker economy, which we think is likely.

In our view, dynamics around earnings may be just starting to shift as this earnings season progresses. As we show below, EPS estimates lag the market. We think there is a good chance they are now be peaking, several months after stocks potentially peaked, with earnings revisions breadth rolling over hard.

What will drive a more material shift in growth/earnings expectations? The obvious answer is rising unemployment. The less obvious is another credit event. Our view is that things are breaking all over the place – commercial real estate, ‘locked in’ homeowners causing a collapse in supply, the bond market, regional banks, small cap stocks, subprime consumers, etc… Obviously none of these are big enough to matter right now, at least while unemployment is still low. That could change quickly. The signal we would watch for is when the recent bear steepening shifts to a bull steepening. That’s often a sign a downturn is imminent or has already begun, with the shift in the curve indicating rate cuts are on the way.

Timing that turn is difficult, a reason we have stayed away from trying to call the exact start date of a recession. However, over the course of the past two years, shifts in financial conditions have tended to precede shifts in macro data (vs expectations). With the sharp tightening in financial conditions over the past two months, on top of very strong 3Q GDP supporting growth expectations, conditions are ripe for material downside surprises over the next two quarters.

Finally, with stocks now down 10%, and much higher credit yields, there is modest value emerging in places. We will follow up with specific trade ideas in future notes. Generally, the most cyclical parts of the market are very oversold, and we wouldn’t be surprised to see a several week bounce, led by some of the weakest links, such as the Russell 2K. We would mostly avoid these areas other than for a quick trade. Even though they may be valued better today, we doubt cyclicals sustainably outperform until the economic data weakens and rate cuts are around the corner. For now, we would still stick with quality. Defensive sectors like Utilities and Staples have some idiosyncratic challenges, but should still outperform in a rocky macro backdrop. Alternatively, while spreads are far from cheap, we think long duration IG at ~6.5% is very attractive for long-term, total return focused investors.

Disclosures

Please click here to see our standard Legal Disclosures

The Spread Site Research

Receive our latest publications directly to your inbox. Its Free!.

{kind=link}