Have a Playbook

Summary

- The market melt up continues, but the drivers have shifted. In Nov/Dec, markets were optimistic around declining inflation, more modest growth, less Treasury supply and this soft-landing optimism fueled a rally in both bonds and stocks. Small caps and banks led and Tech lagged.

- Since the start of the year, stocks have continued to rally but now with rising bond yields on the back of hopes for an economic acceleration. Large-cap tech has been the clear leader. If economic acceleration shifts to concerns around another inflation wave, the rise in bond yields would likely become more problematic. For now it’s still Goldilocks.

- Bigger picture, our view is that the macro data remains mixed. Yes, preventing a re-acceleration in inflation is important, but the Fed needs to have high confidence in that view to forgo cuts. If they get it wrong and wait to cut until unemployment is clearly rising – it’s too late, they missed the boat again.

- In the short term, we recommend having a clear playbook for what should outperform in various scenarios, and looking for trades offering asymmetric risk/reward. For example, at 316bp HY credit has much more downside in a hard landing or late-cycle re-acceleration than upside if we are in fact early in a new cycle.

Internal Shifts

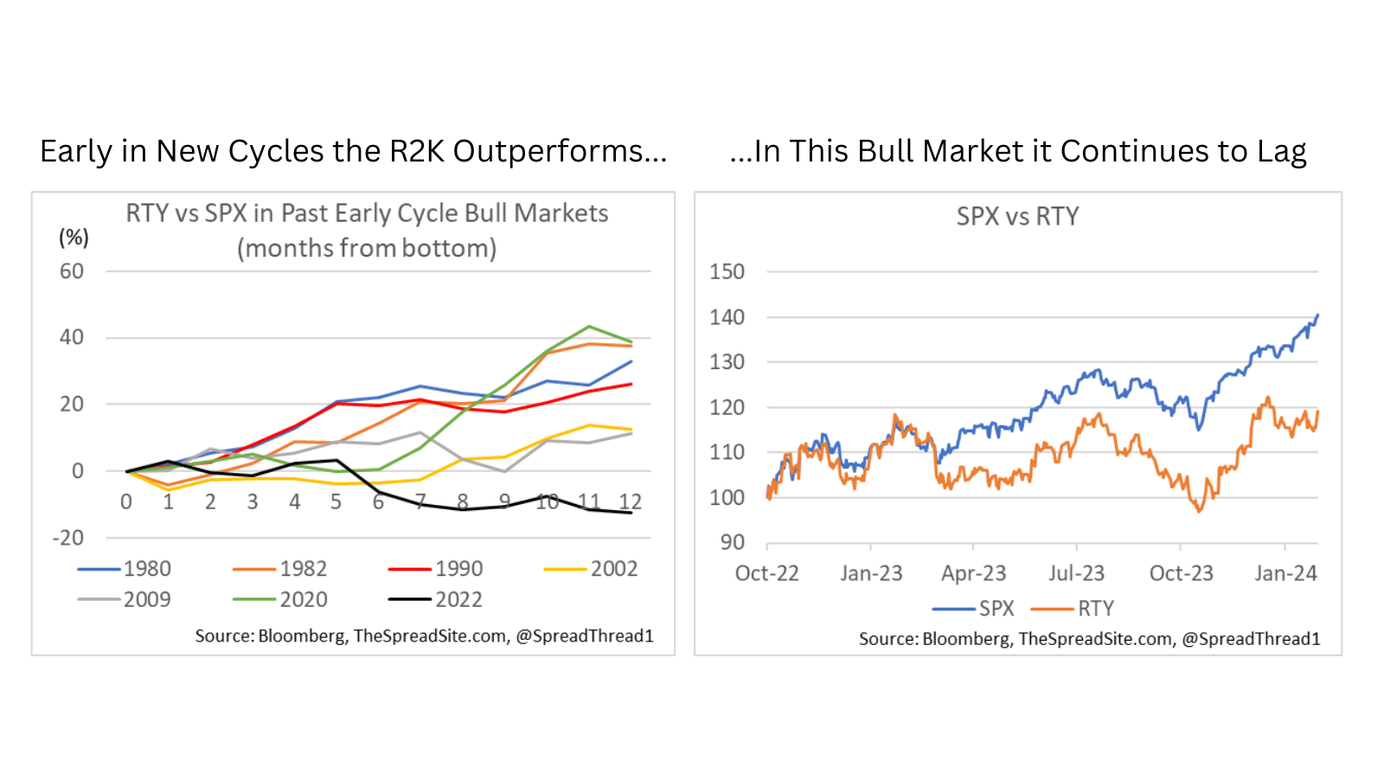

The melt up in markets continues, with the SPX surpassing 5,000, rallying over 22% since the end of October in nearly one straight shot. Looking under the surface, the drivers have arguably shifted since the beginning of the year. In Nov/Dec the equity rally coincided almost one-for-one with a sharp move lower in bond yields. In a nutshell, growth slowing from overheated levels, declining inflation, less concern around Treasury supply, and greater optimism on a soft-landing, supported both bonds and stocks. Over these two months, small caps (+26%) and banks (KBE +36%) led and tech marginally lagged (QQQ +19%).

Since the start of the year, markets have continued moving higher, after a small hiccup in the first week of Jan, but now with bond yields rising at the same time. Additionally, since the start of the year, small caps and banks have underperformed large cap tech in a big way, with cyclicals treading water vs defensives. What has driven this shift?

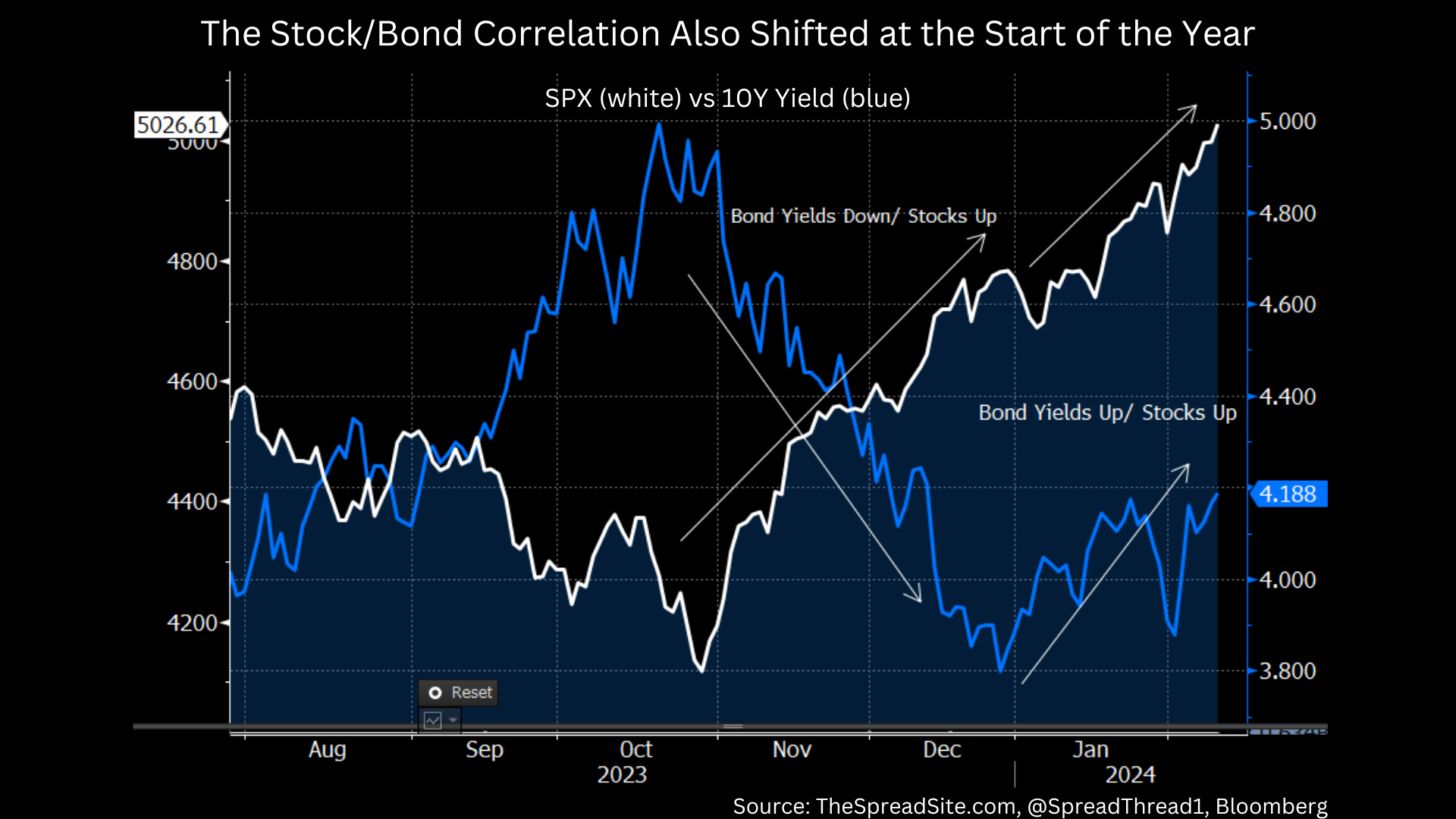

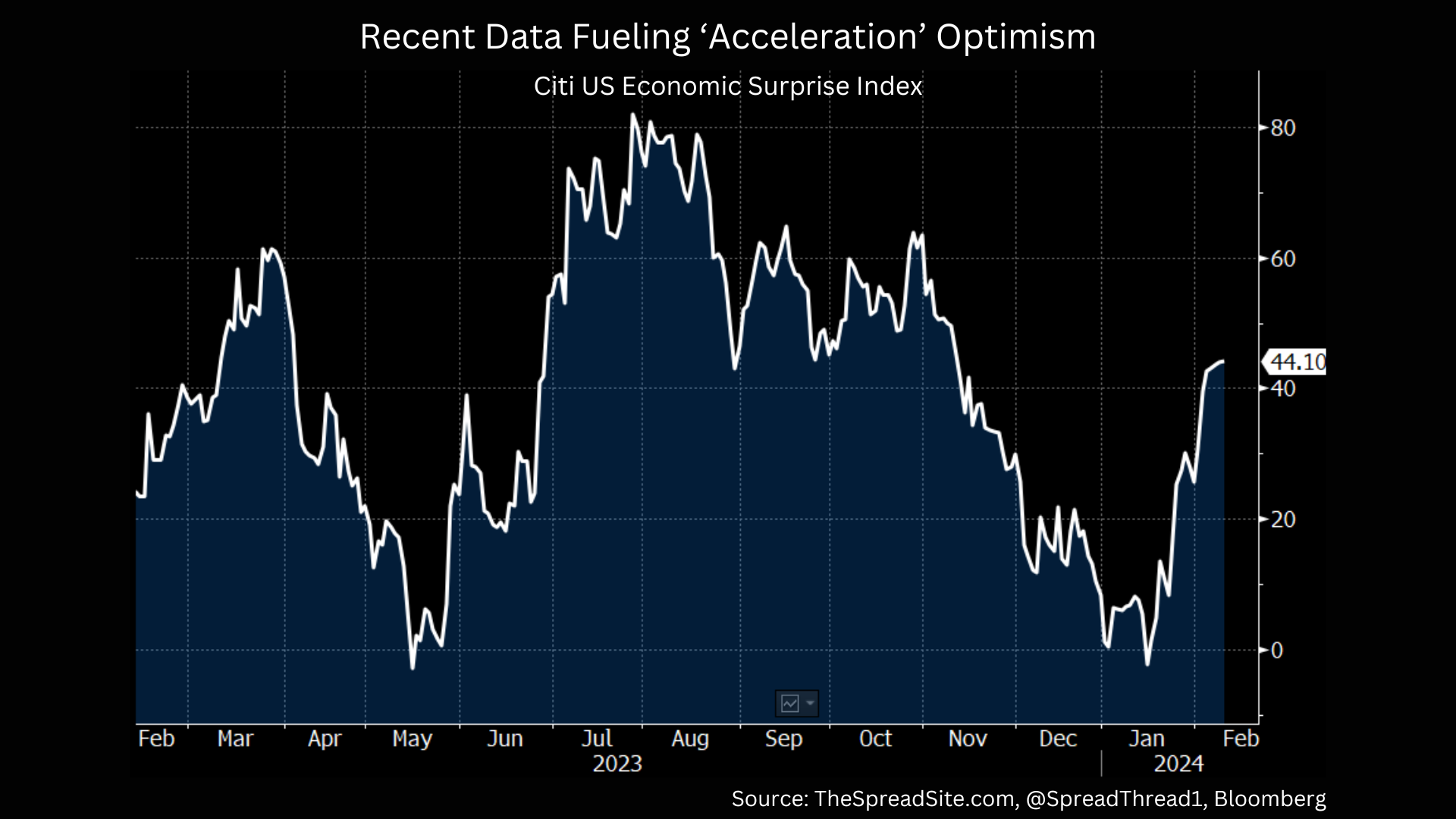

While a soft-landing remains a consensus view, a greater number of investors are now calling for a re-accelerating economy. Better growth expectations, and marginally more hawkish Fed rhetoric, have led to a modest move up in bond yields across the curve. However, the rise in yields hasn’t hit risk assets in aggregate, with the correlation between bond and stock prices flipping negative.

But it has impacted leadership in the market, with sectors most impacted from higher rates (i.e., small cap stocks) underperforming, and secular growers/quality balance sheets (i.e., large cap tech) outperforming. In a sense, since the start of the year, markets have much more of a late-90s feel - stocks melting higher, led by a small subset of large cap stocks, coinciding with expectations of better growth/rising productivity, and therefore tolerating higher bond yields.

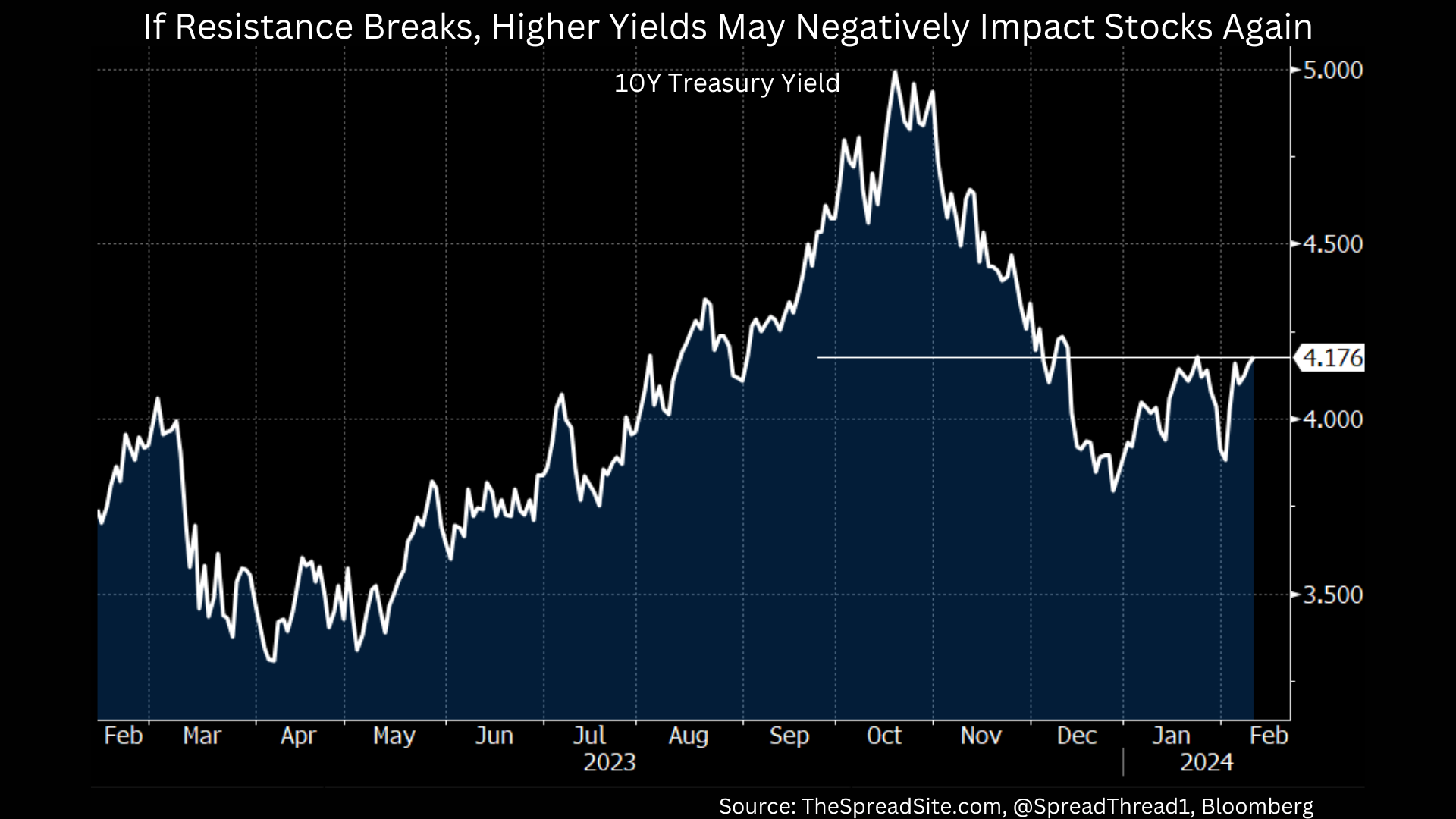

We have argued since the start of the year when 10Y yields dipped below 4%, that the stock/bond correlation was likely to shift in this way (i.e., to a negative correlation). Our view was that yields declining well below 4% would no longer be a positive for markets, signaling underlying problems in the economy. Whereas a modest rise in yields after the big Nov/Dec rally, as well as 1 or 2 rate cuts coming out would be fine initially.

What will it take for bond yields to matter in a bigger way again? Maybe it is simply a certain level – for example rates breaking out of the current range, where investors again start to worry about tightening financial conditions. More likely, we think optimism over accelerating growth needs to transition into fears over a re-acceleration in inflation. The strong January payrolls report had the potential to re-ignite inflation concerns, but did not do the trick. Maybe a hot CPI print this week will be enough. Until then, ‘Goldilocks’ is still clearly winning.

Acceleration Optimism

Bigger picture, our view is that the macro data remains mixed, with a little something for everyone. However, we continue to think the labor market is softening, January payrolls notwithstanding. We have pushed back against the idea that the economy is about to reaccelerate in a big way. And while a handful of datapoints may be signaling that risk is growing, it is still not our top concern. However, the Fed believing the economy is re-accelerating is probably not an ideal outcome.

Without getting into all the details, a growing consensus believes solid (even accelerating) growth is a sign Fed policy isn’t all that tight. In our view, there is a lot of mistaking short-term shifts in the economy (i.e., the increase in deficits in ’23) which warrant higher rates ‘for now’ from true long-term changes. We continue to believe that the reason this economy can seemingly handle high rates is because most of the economy is not experiencing high rates – still locked into ZIRP-era debt costs. And remember, it is normal for the consensus to believe that tightening isn’t working late in a cycle just as it is normal for investors to argue rate cuts aren’t working in a recession.

The problem is that if the Fed now thinks policy may not be as restrictive as they initially believed, and as a result, they wait for clear signs of weakness to cut, they decrease the likelihood of re-accelerating inflation, which is a positive, but they also make a soft landing less achievable. Why? Just as it takes time for rate hikes to slow the economy, rate cuts also do not boost growth instantaneously. If the Fed waits to cut until unemployment is clearly rising – it’s too late, a recession has already begun and once again they are behind the curve.

A Playbook

Admittedly, we see several cross-currents in markets today, and don’t have high conviction on how the narrative shifts over the next few months. Easier financial conditions may be boosting growth temporarily. However, restrictive Fed policy is still hitting the economy, and rates are again rising. All it takes is one weak payroll print to change the conversation from upside to downside risks. In the short-term, we are not taking a strong view on direction (macro or markets) but instead, prefer to have a clear playbook for what should outperform in various scenarios, and structure trades based on the parts of markets that are most aggressively priced for one scenario or the other.

Below is a somewhat simplistic playbook, as an example. Keep in mind all these scenarios are path dependent, for example, if policy makers are slow or quick to respond.

Hard landing/Growth Scare:

Curve: Bull steepens

Yields: Lower

Credit: BBs>CCCs

Stocks: Defensives (Utilities, Staples, Healthcare) > Cyclicals

Early in New Cycle/ Soft Landing:

Curve: Steepens

Yields: Mixed

Credit: CCCs > BBs

Stocks: Small Caps/Banks/Retail/Homebuilders > Defensives & Tech

No Landing/ Late Cycle Acceleration:

(initially)

Curve: Bear flattens

Yields: Higher

Credit: Long Bs

Stocks: Large Cap Tech, Energy, Industrials > Small Caps/Banks/Retail/Defensives

(eventually)

Hard Landing playbook

Look for Asymmetric Trades

Based on this rough playbook, we are looking for asymmetric trades, given what is in the price, even if that trade runs counter to our core views. Remember, the ultimate destination for the economy may be a hard landing (still our view), but the consensus will likely continue to bounce between various narratives for a while, as it has over the past year, before the endgame is obvious.

A few specific examples:

-

HY credit has much more downside in a hard landing or even no landing than upside in a soft landing, based on current spreads levels (316bp).

-

Similarly, defensive sectors (i.e., Utilities, Healthcare, Staples) have much more potential for outperformance in a weak economy vs underperformance in a soft landing.

-

Homebuilders have more potential to underperform in a hard landing vs outperform in a soft landing – pricing in a very ideal environment of a healthy consumer indefinitely, rate cuts, and limited existing home supply.

-

Energy has asymmetric upside in a ‘late cycle acceleration,’ in our opinion.

-

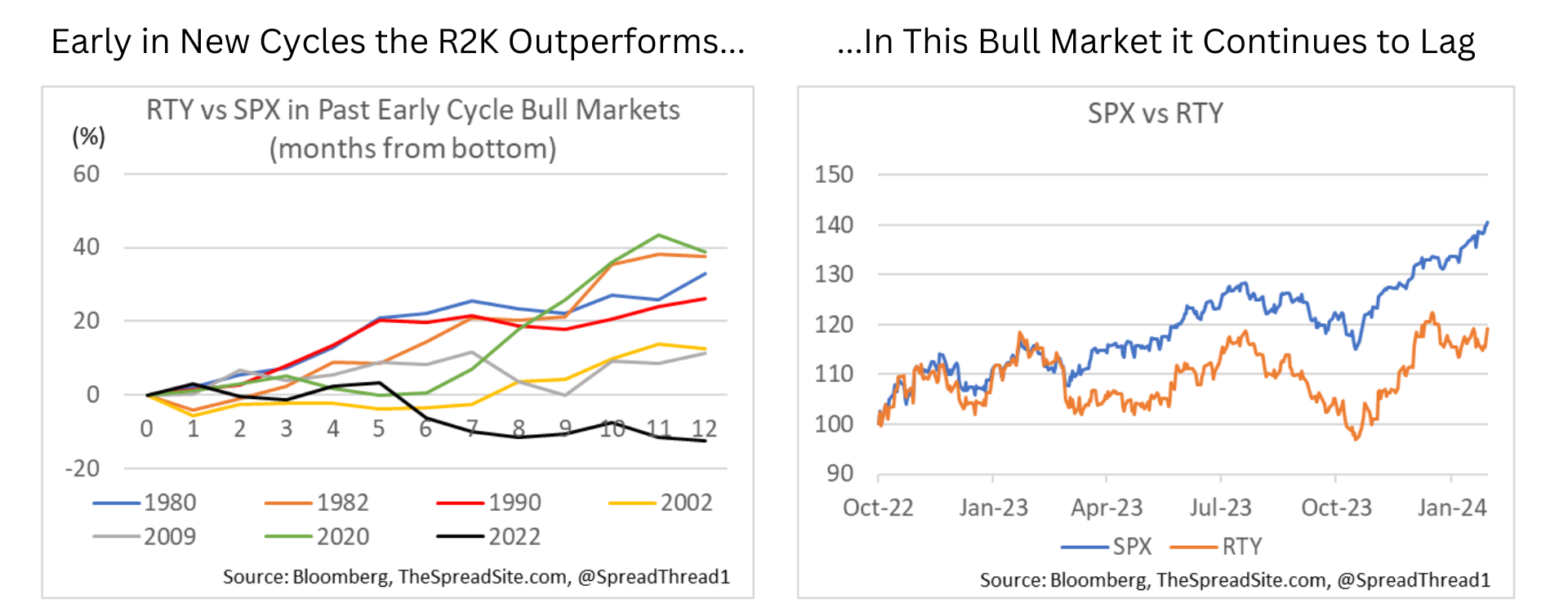

Small cap stocks have asymmetric upside in a soft landing, as they tend to outperform in a big way early in new cycles.

-

Gold also has attractive risk/reward – modest downside if we remain in this ‘Goldilocks’ environment for a while, solid upside if investors start to fear a behind the curve Fed with inflation breakevens rising, and also upside in a hard landing.

-

We don’t think there is an obvious trade in rates at current levels. We are waiting for Treasury yields to break higher as this acceleration narrative gains more momentum, and would then look to take the other side of it.

Disclosures

Please click here to see our standard legal disclosures.

The Spread Site Research

Receive our latest publications directly to your inbox. Its Free!.

{kind=link}