Restaurant Stocks to Face Macro Headwinds

Summary

-

The service economy has been resilient, supporting stocks catering to consumer ‘experiences.’ We think several macro headwinds could change those dynamics. This week’s note provides an overview of the restaurant sector and a long/short basket to play this theme.

-

Student loan repayments are set to resume this fall, the surge in demand for ‘experiences’ is due for payback, excess savings are wearing thin, and the ‘bite’ from rate hikes/tighter credit is still to come. Additionally, as a negative side effect of all this macro optimism, Treasury yields and gasoline prices are again both rising.

-

We don't think a recession is necessary to pressure consumer discretionary stocks, like restaurants. Slowing to below-trend growth is enough. But any hint of rising unemployment would accelerate the downside- an asymmetric risk we like positioning for, given the soft-landing optimism now in the price.

-

We like shorting a basket of 10 restaurant names mostly within 'Casual Dining' ("BJRI", "CHUY", "DRI", "EAT", "BLMN", "TXRH", "FWRG", "CMG", "SHAK", "KRUS") against a basket of 6 defensive restaurant names ("WEN", "DPZ", "YUM", "JACK", "CBRL", "WING") as a way to express our macro view.

Introduction

Over the past year, despite macro and market volatility as well as dramatic price increases, US consumers have shown more resilience than many expected. In particular, the service side of the economy has outperformed expectations, supported by the post-Covid goods-to-services shift, as well as large excess savings stockpiles. This story is now well known, with primary beneficiaries of these consumer trends, such as restaurants, rallying ~19% year-to-date ("EATZ" ETF).

After this year’s rally, and the bullish sentiment that followed, we think the potential headwinds for this part of the economy are now less appreciated. To name a few - student loan repayments are set to resume this fall, the surge in demand for ‘experiences’ is likely due for payback, excess savings are wearing thin, and going forward, we think rate hikes/tighter credit will bite in a bigger way. Additionally, as a negative side effect of all this macro optimism, Treasury yields and gasoline prices are both again rising, at exactly the wrong time.

Given these headwinds, and the optimism built into the travel/leisure segment of the economy, we like shorting the ‘Casual Dining’ part of the restaurant sector, in particular. We present a short basket along these lines, against a basket of more defensive longs in the space, in case our view doesn’t play out or takes longer to do so. In the sections that follow, we briefly walk through some of the macro headwinds we note above, provide an overview of the restaurant industry, and discuss our trade recommendation.

The Macro Backdrop

The US economy has clearly benefitted from a surge in demand for travel/leisure/dining out in the post-Covid period. And while inflation skyrocketed, consumers had built up savings, in part as a result of pandemic stimulus, which drove some price inelasticity, at least for a time. We think the headwinds going forward are growing.

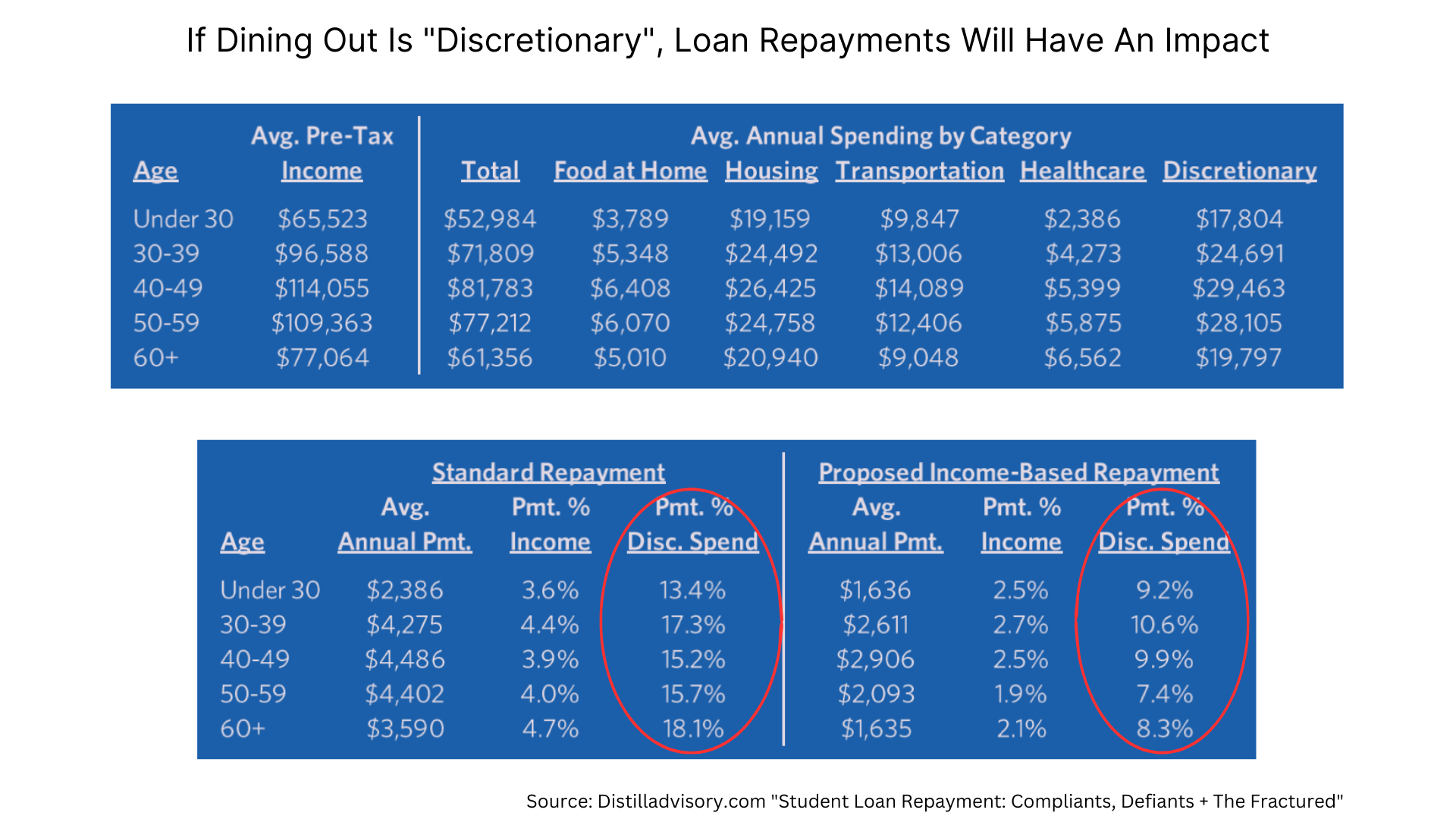

First, student loan repayments, in our view, are a meaningful issue for a large chunk of the consumer base. Since March 2020, borrowers have not been required to make payments on student loans due to a forbearance policy put in place during COVID. Starting September 1, these loans will start accruing again with payments due October 1.

The table below provides an estimate of the impact to discretionary spending and is part of an excellent report published by Distill Advisory. With $1.8 trillion in student loans outstanding and a payment as a percent of discretionary spend ranging between 7.4% to 18.1%, it is difficult to argue this will not have an impact.

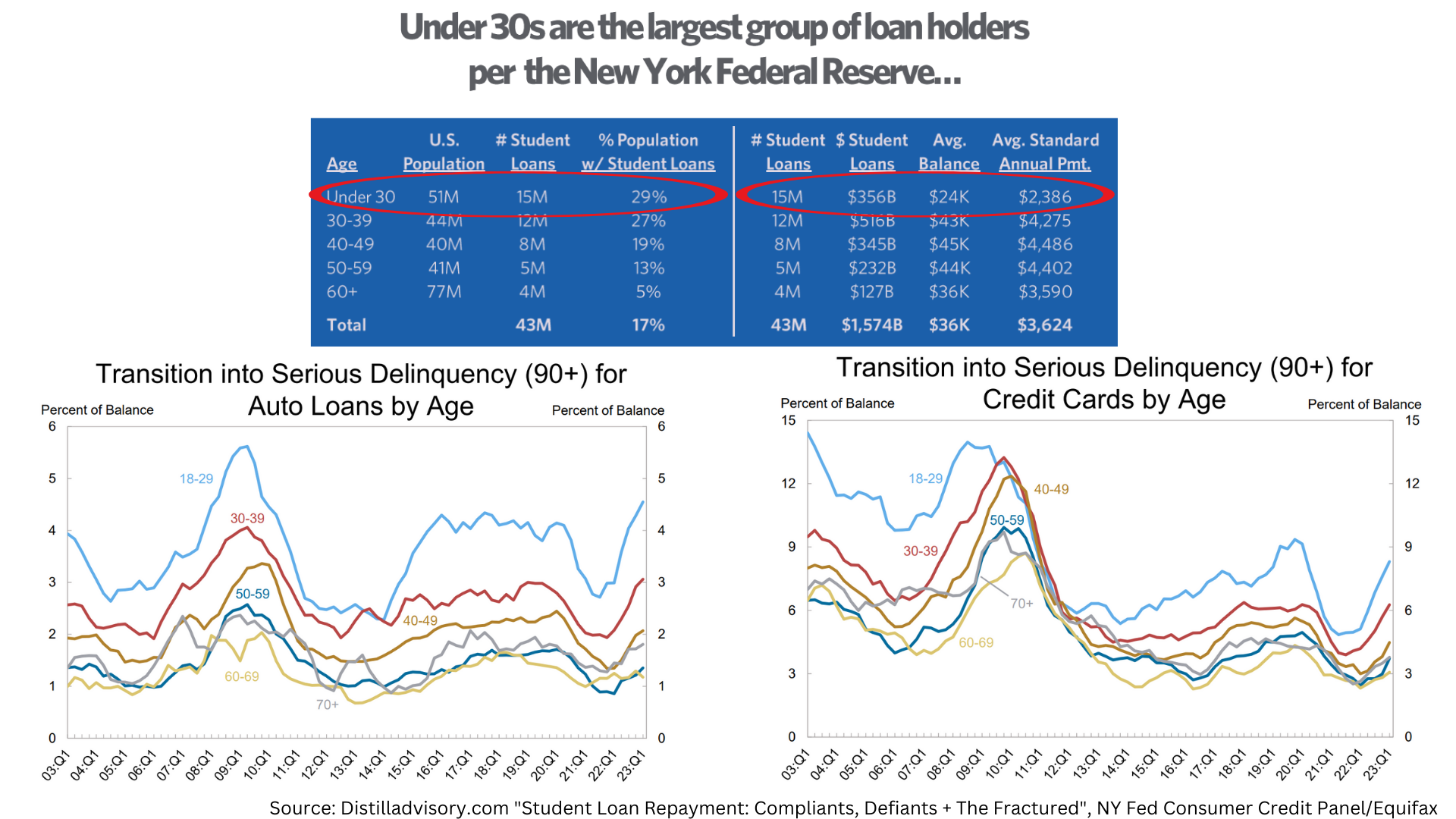

Many economists will add up the total hit from student loan repayments to GDP and come to relatively small numbers, concluding that it is no big deal. We think this misses the point: The impact of this headwind is not spread evenly throughout the economy. It is hitting a specific demographic group (younger consumers), the same cohort that is already struggling with high costs and higher debt burdens. And remember, all consumers don’t need to pull back to have a material slowdown. 43 million vulnerable individuals is enough to make a dent.

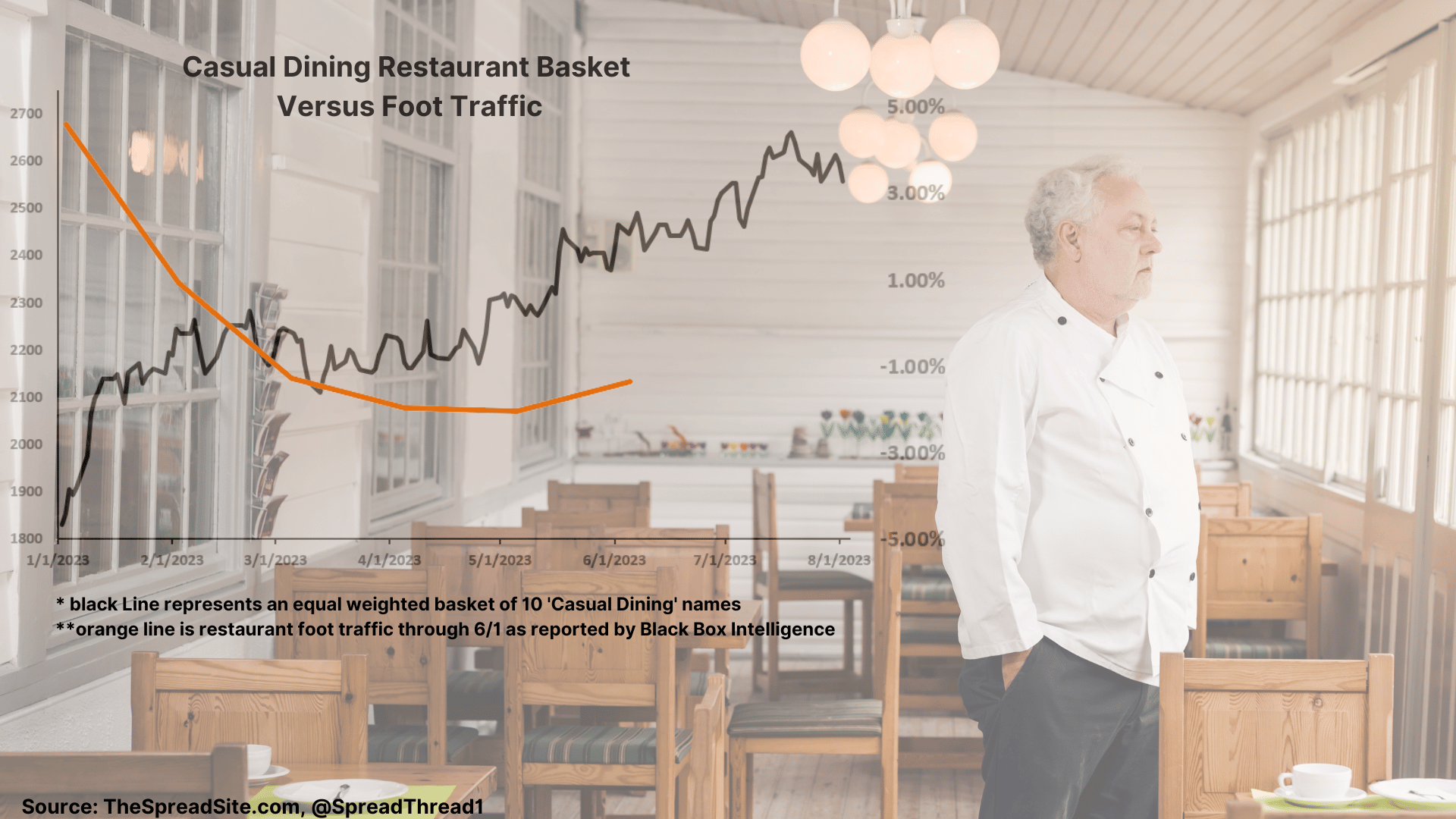

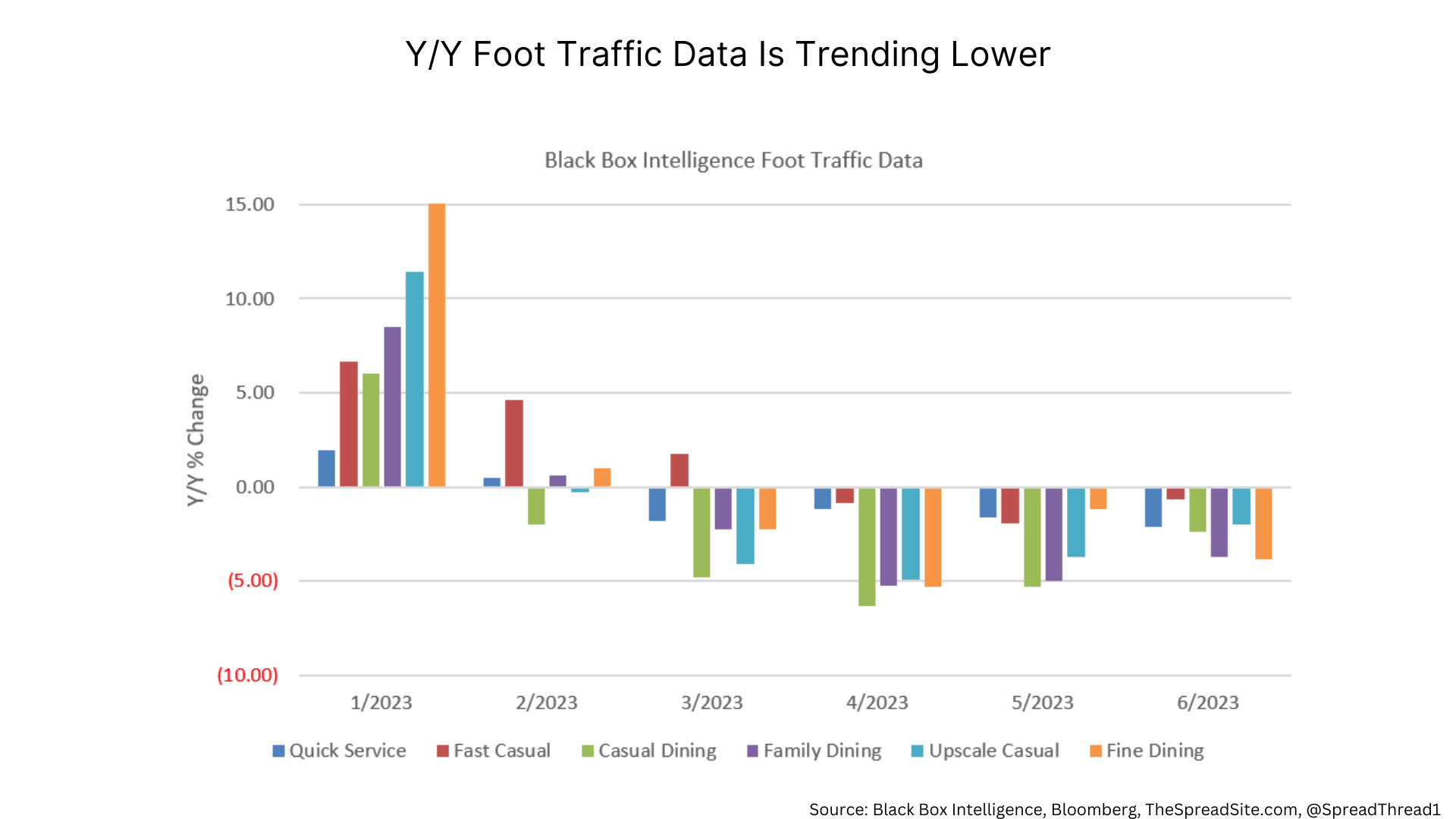

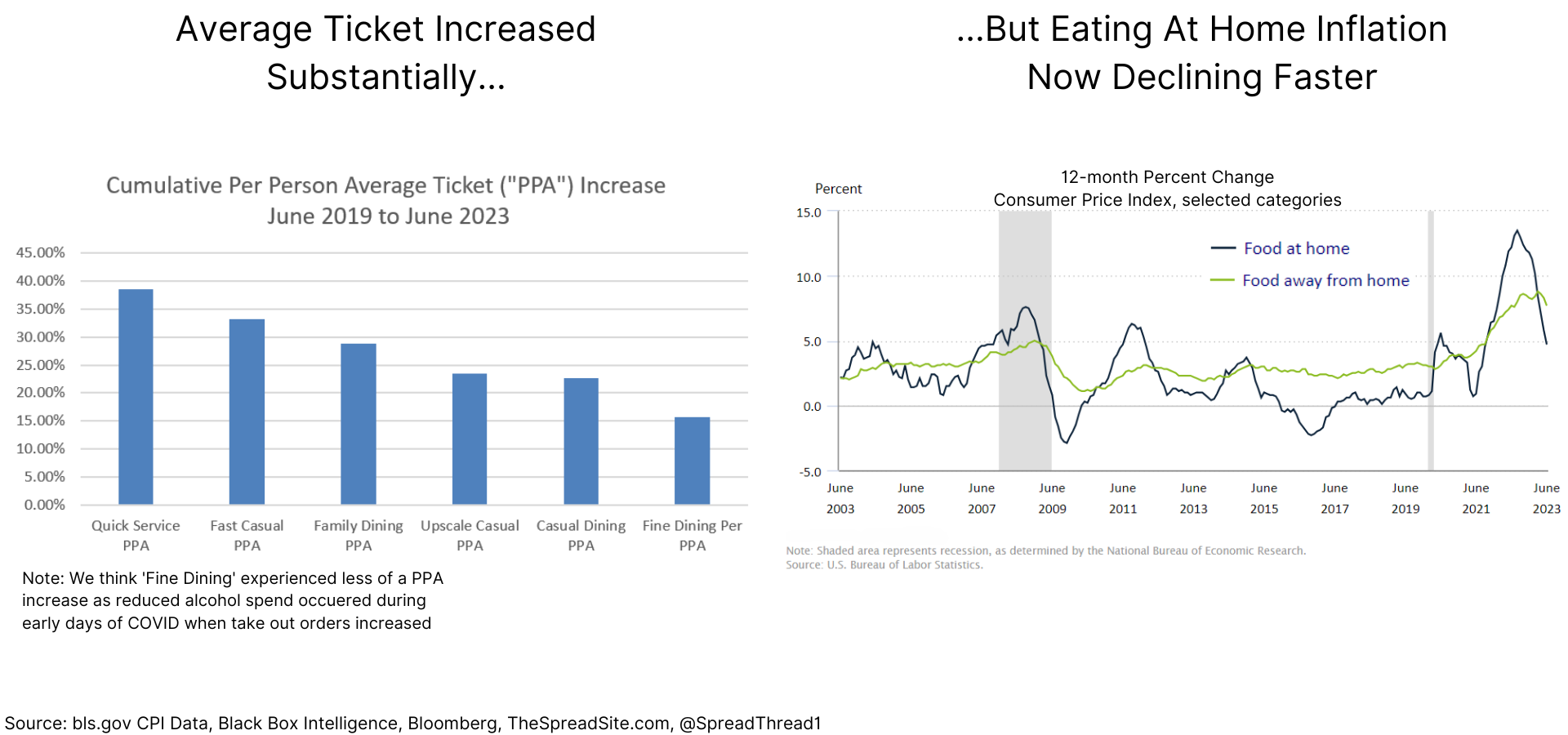

Second, in addition to student loan repayments, payback from the surge in ‘experience’ spending post-Covid, such as dining out, is just beginning, in our view. And this dynamic does not require a recession, just some reversion to the mean, which we believe is already taking place. For example, the exhibit below shows declining restaurant foot traffic through June from Black Box Intelligence (July not yet available).

We believe ‘Casual Dining’ restaurants are following the same pattern as other related sectors experiencing a payback from their post-COVID boom. For example, as Bloomberg reports, airlines are seeing a significant slowdown in domestic air travel with Alaska Air, Jetblue and American posting double digit declines in Q2 2023 domestic sales.

Additionally, part of the demand for dining out was arguably inflation related- simply, the cost of eating at home (“FAH”) rose faster than the cost of eating away from home (“FAFH”). That dynamic is also starting to change.

As we show below, eating at home inflation is now declining faster than eating away from home inflation, which may also make consumers wearier of the cumulative price increases of eating at a restaurant.

Third, we remain firm believers that 525bp of rate hikes (more if we include the impact of quantitative tightening), multi-decade-high consumer borrowing costs, and much tighter credit conditions is having an impact which will grow over time. As noted above, excess savings allowed consumers to offset some of these headwinds in the short run. However, we think that buffer is growing thin, at least for more vulnerable consumer cohorts.

Finally, with renewed macro optimism, interest rates and oil/gasoline prices are again pushing higher. A late-cycle surge in gasoline prices would not be out of the norm, the type of headwind that often comes at exactly the wrong time – a final straw to break the consumer’s back heading into a downturn.

As noted earlier, we don't think a recession is necessary to pressure consumer discretionary stocks, like restaurants. Slowing to below-trend growth is likely enough. But any hint of rising unemployment would accelerate the downside- an asymetric risk we like positioning for, given the soft-landing optimism now in the price.

Sector Overview

Before detailing our trade recommendations, we first provide a quick overview of the restaurant sector, which is typically broken down into a few broad categories, as follows:

- 'Quick Service' (“QSR”) is generally considered fast food and includes names like McDonalds and Yum Brands

- 'Fast Casual' includes names like Chipotle or Shake Shack where you can dine at the restaurant, but you do not have a server

- 'Casual Dining' includes full-service names like Chili’s and Olive Garden

- 'Fine Dining' would include upscale restaurants like Ruth’s Chris (recently acquired by Darden as part of their fine dining segment)

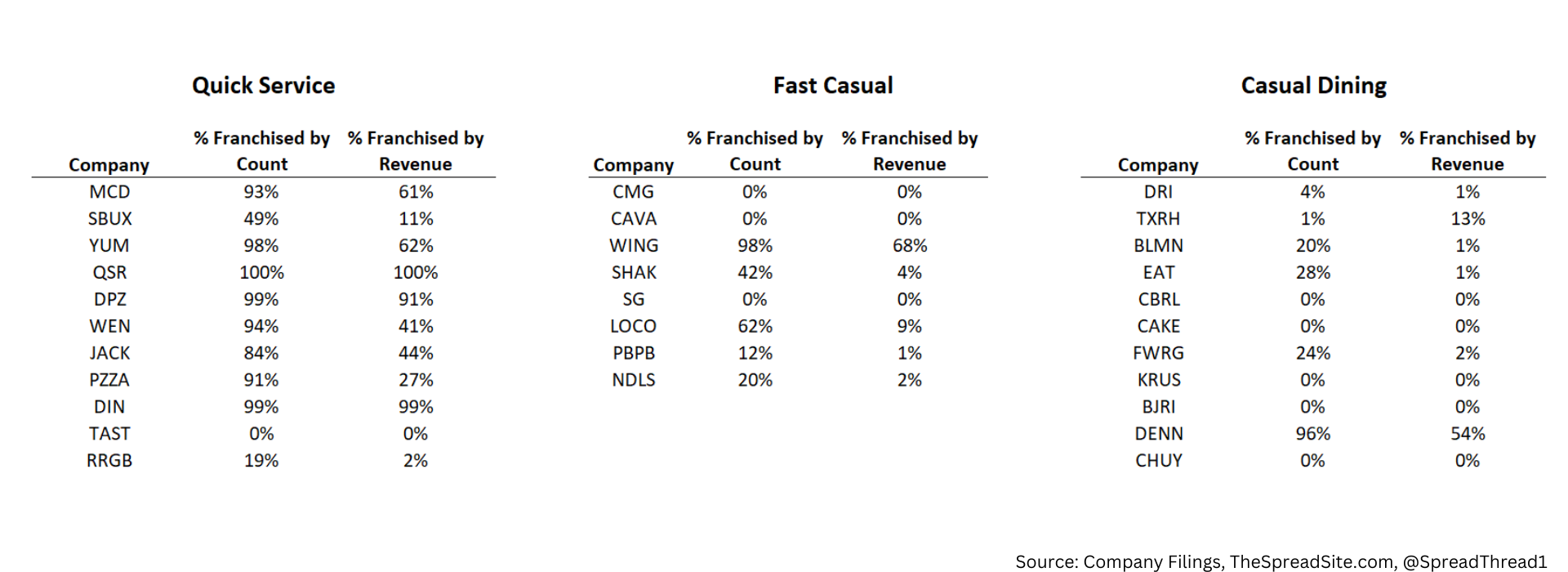

There can be some variation within categories, but the ones above are the broad segments. Within each, restaurants can choose to franchise their business or not. And as we show below, the mix varies. As a franchisor, the corporate entity receives fees from franchisees who operate under a proven business model and pay licensing fees as a percent of revenue or profit (each license agreement varies). Below is a breakdown of the sector in terms of franchise locations and revenue.

The mix of revenue from franchisees is important because a well-run franchisor (like "MCD" or "QSR"), will typically trade at a higher multiple than non-franchisors. This is because franchise revenue tends to be higher margin and requires less investment in physical assets. When done right, franchisors have very high margins and very little capex. But it is important to remember, this is an ideal scenario. If franchisees cannot generate profits, they eventually go bust and cease making payments. Additionally, it becomes very hard to grow as a franchisor if there is no demand for additional franchised locations.

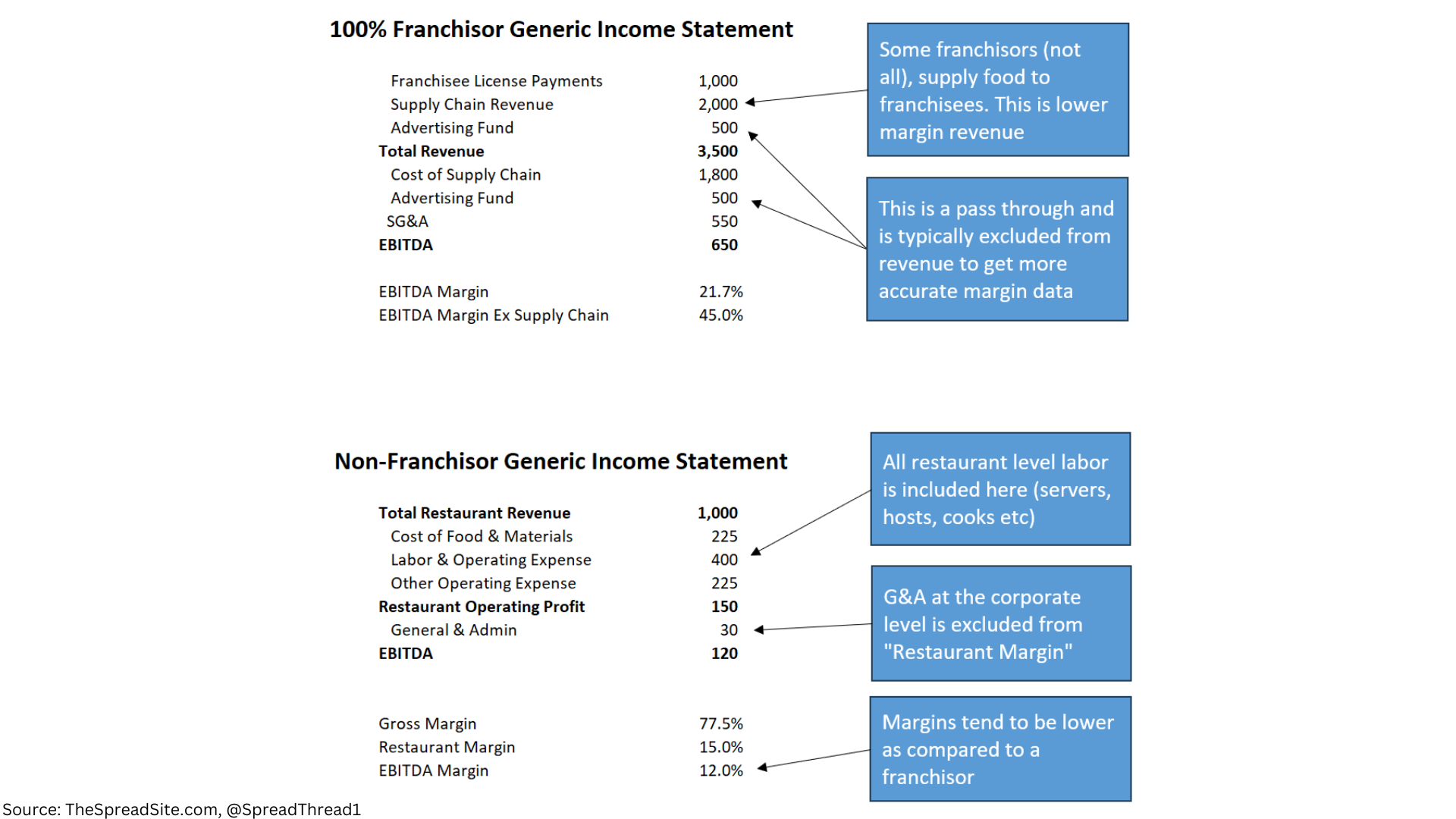

A generic income statement of a typcial pure-play franchisor vs a non-franchisor is shown below.

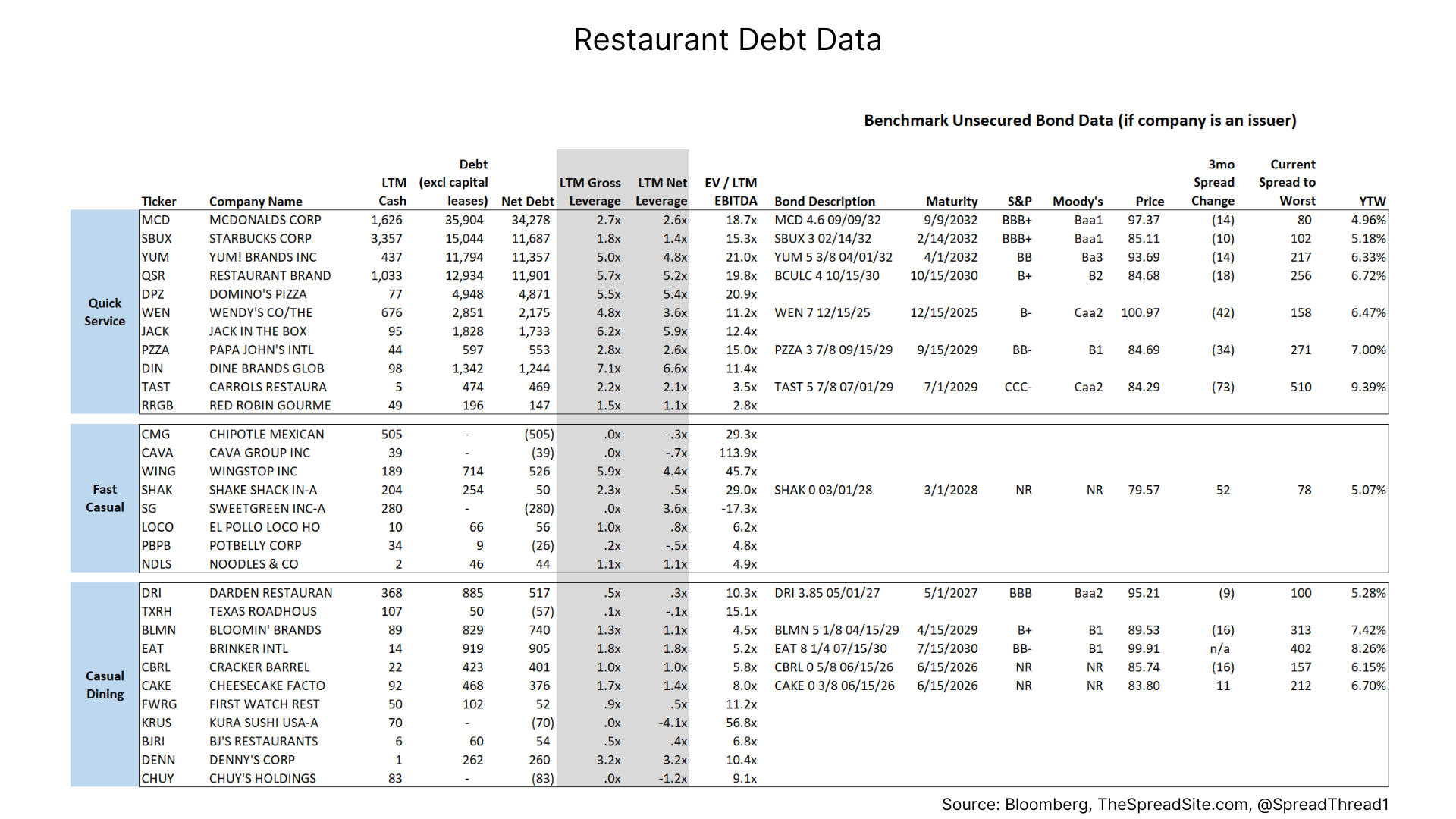

Successful franchisors are also able to carry more leverage given the stability of high margin license payments (see Appendix for debt details). Franchisors can also choose to securitize these payments and issue debt against them.

Whether a restaurant is a franchisor or non-franchisor, food and labor cost always matter since it impacts the health of the operating business. But typically, non-franchisors that own physical locations feel the impact of inflation much quicker.

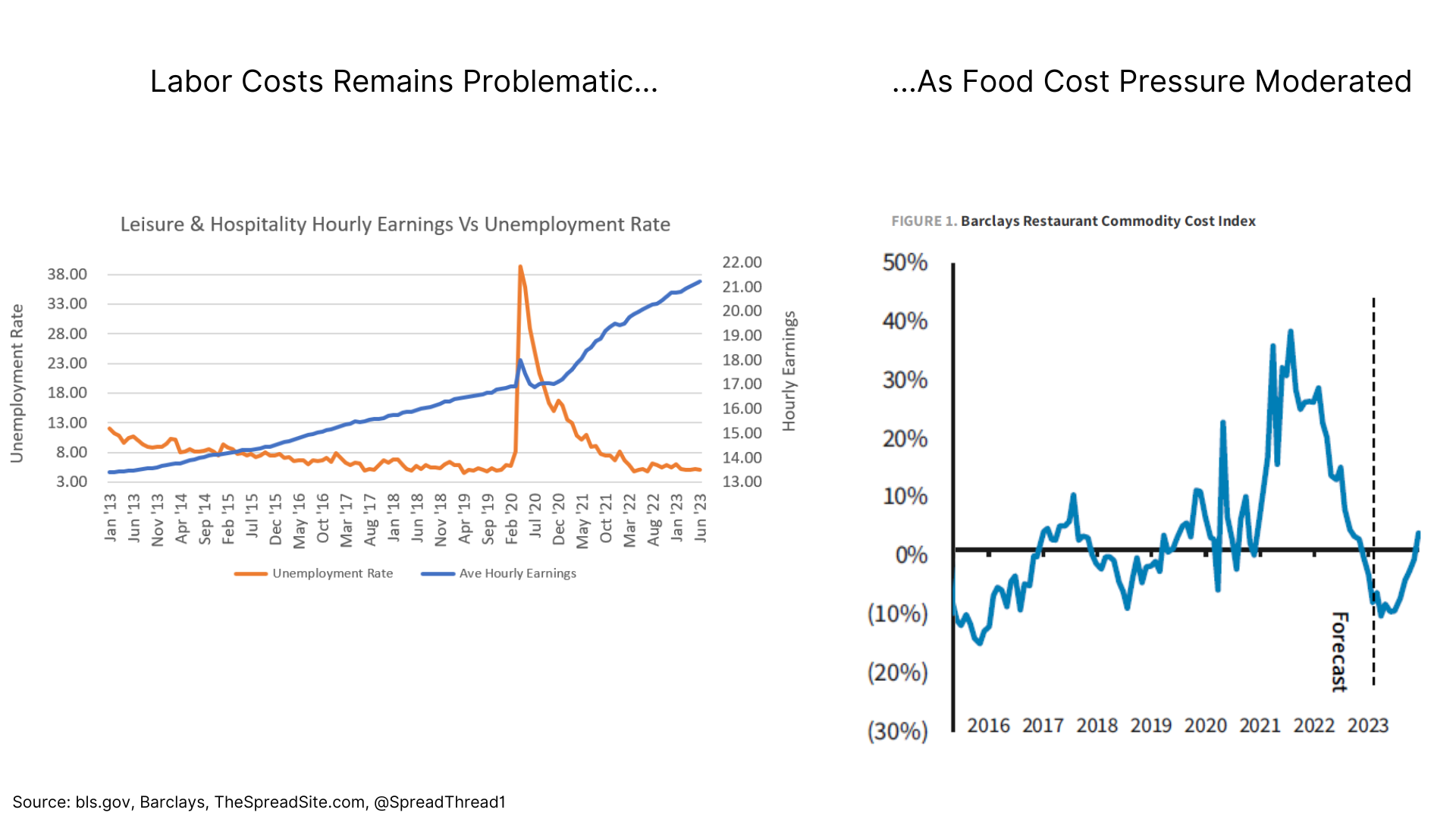

To put food and labor inflation in context, for a typical restaurant company that owns its locations, food cost represents ~28-30% of sales and labor ~30-32% of sales, generally speaking.

Labor remains a bigger issue than commodity prices (for now), as leisure and hospitality wages show, while overall food cost inflation has come down notably.

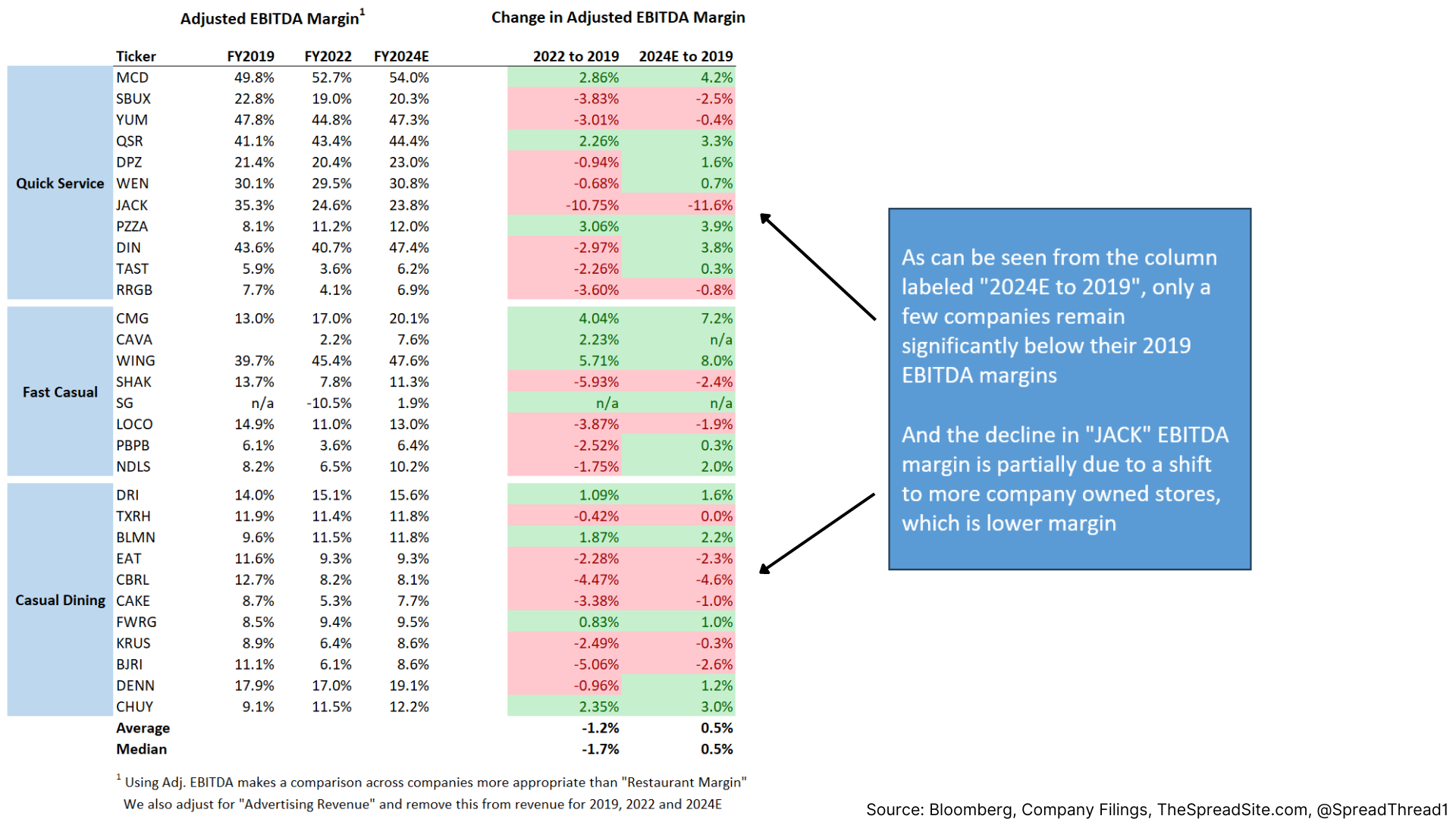

As restaurants felt the pinch from inflation in late 2020, they started raising prices to recoup margin. So far, there has been fairly little pushback from diners to significantly higher prices – though recent declines in foot traffic could indicate a shift in trend to come. And as we show in the table below, through 2022, margins were still below the 2019 level. However, given 2024 consensus estimates, margins are getting closer to 2019 levels, with some companies now higher.

The bull case within casual dining is that sales trends will continue as dining out remains an affordable luxury. And as inflation subsides, restaurants will continue improving margin, driving further momentum in EPS growth.

For example, in terms of revenue, consensus estimates for 2023 assumes median growth of 7.3% and another 6.5% for 2024. For EBITDA, consensus estimates for 2023 assumes median growth of 13.4% and another 10.9% for 2024.

The more realistic scenario, in our view, is that consensus is pricing in a continuation of the strength seen in 2023 and fails to account for the macro headwinds we outline. And while valuation on 2024 numbers looks reasonable within our short basket, this can quickly change if 2024 numbers start moving lower.

Furthermore, casual dining is a highly discretionary category. And as we have seen with other discretionary sectors like retail and domestic travel, consumers can change spending habits quickly. We believe ‘Casual Dining’ restaurants will be the next sector to face headwinds.

Trades

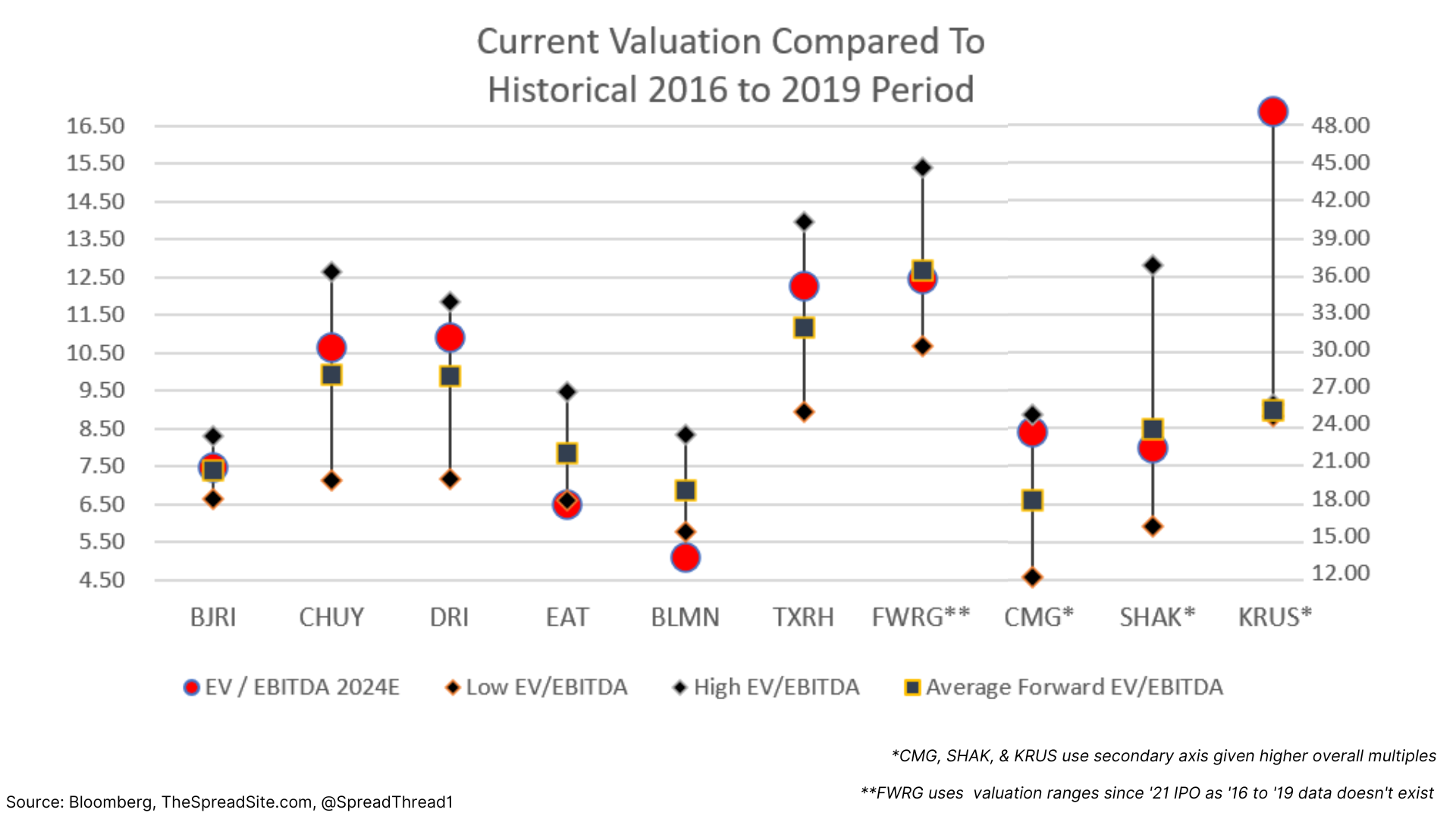

To express our view, we prefer going short a basket of casual dining companies that were disproportionately impacted in the last recession, have minimal franchise revenue and generally represent a higher overall ticket cost as compared with 'Quick Service.'

This basket comprises 10 names and includes; “BJRI”, “CHUY”, “DRI”, “EAT”, “BLMN”, “TXRH”, “FWRG”, "CMG". “SHAK”, and “KRUS”. Year-to-date, this equal-weighted index is up 39% and carries a weighted Beta of 1.19 versus the S&P500. While "CMG" and "SHAK" are considered 'Fast Casual' we believe they will face the same pressure as the 'Casual Dining' names.

In order to reduce the risk of shorting too many cheap ‘Casual Dining’ names, we exclude “CAKE” and “CBRL." In addition, “CAKE” has short interest comprising 20% of its float which is another reason we remove it.

As for “CBRL”, we chose to include it in our long basket as it trades cheap to a historical range, should see less impact from a student loan payment restart and was less impacted during the last recession.

In terms of valuation, there could be significant debate on the correct metric (EBITDA vs P/E), our chosen historical timeline and the nuance involved for each company. We chose to compare current valuations with the 2016 to 2019 period as it represented a more normal timeframe. In addition, we like a basket of both longs and shorts to help diversify idiosyncratic risk within any individual company.

The chart below shows valuation ranges within our short basket.

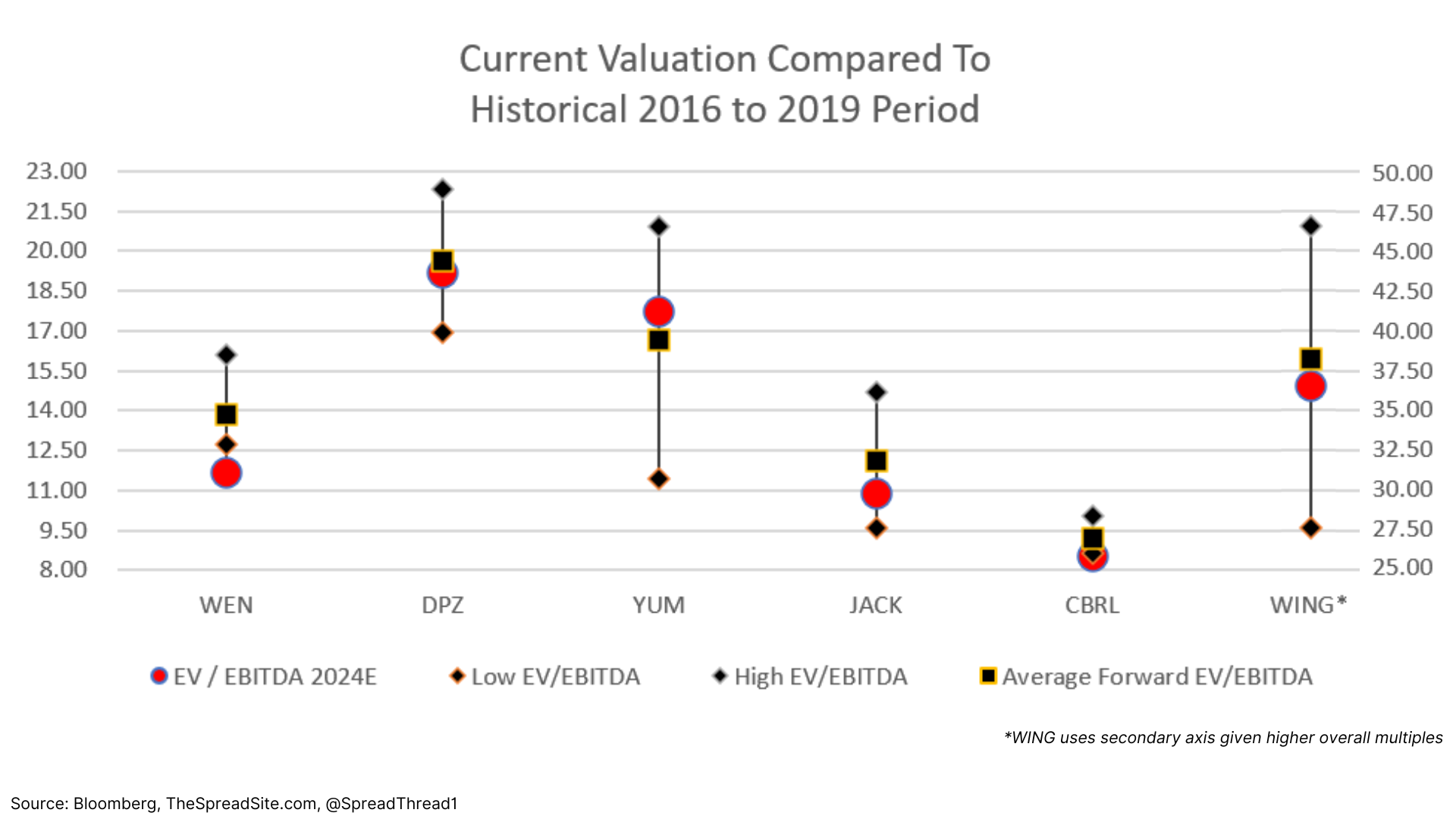

In order to offset the risk that we are wrong or early, we like going long a basket of defensive names.

Our long basket comprises 6 companies including; “WEN”, “DPZ”, “YUM”, “JACK”, “CBRL” and “WING”. This basket, equal weighted, is up 10.7% year-to-date and has a weighted Beta of 1.0 versus the S&P500.

Additionally, these names are mostly in the ‘Quick Service’ category and have a significant amount of franchise revenue (excluding “CBRL”). We show valuations of our long basket in the chart below.

You may wonder how “WING” with a 37x forward EBITDA multiple could be considered defensive. We highlight that they are primarily a franchisor, have best-in-class margins, and have sector leading same store sales (“SSS”) and unit growth. And since it is part of a basket, it is hedging long names like KRUS at 50x.

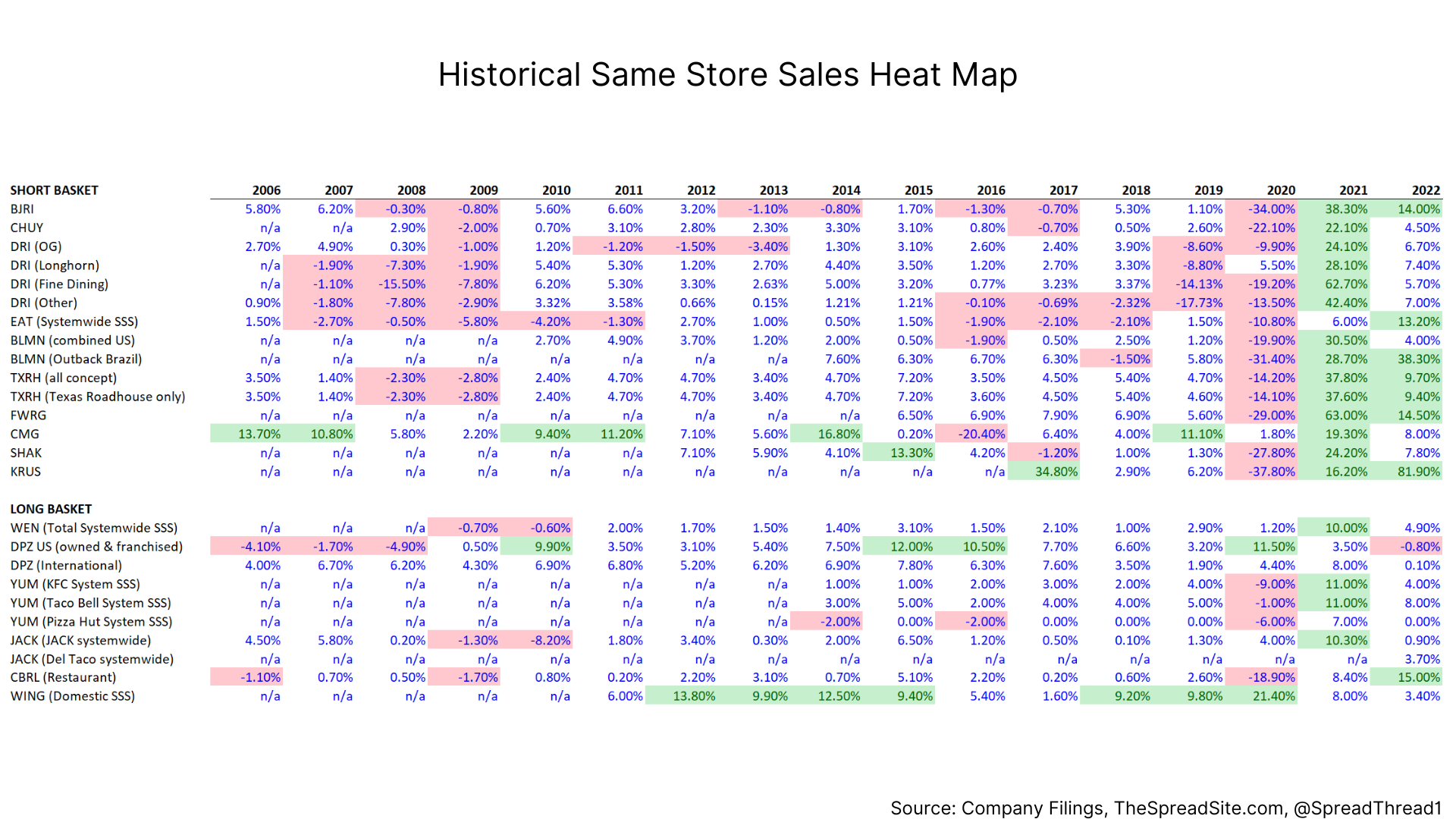

Comparing SSS trends during the last downturn, you can see why the long basket is considered defensive. And while data didn’t exist for some names going back to 2009, our general view is that casual dining concepts will perform similarly on the short side. For example, we assume BLMN, SHAK and KRUS will also see a decline in SSS if we are correct on our macro view.

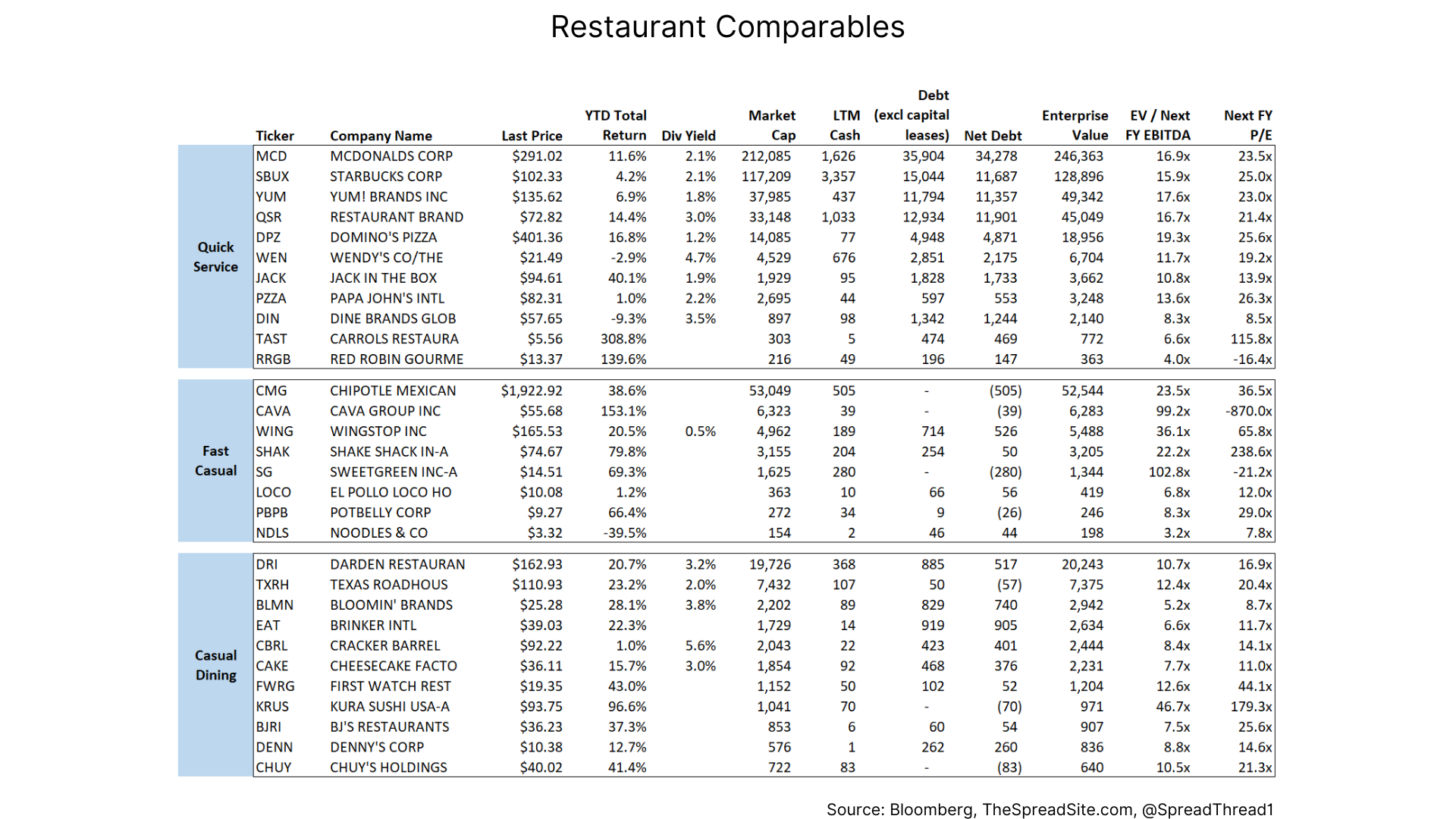

For full comparables data on all restaurant names, please see the Appendix at the end of this report.

Appendix

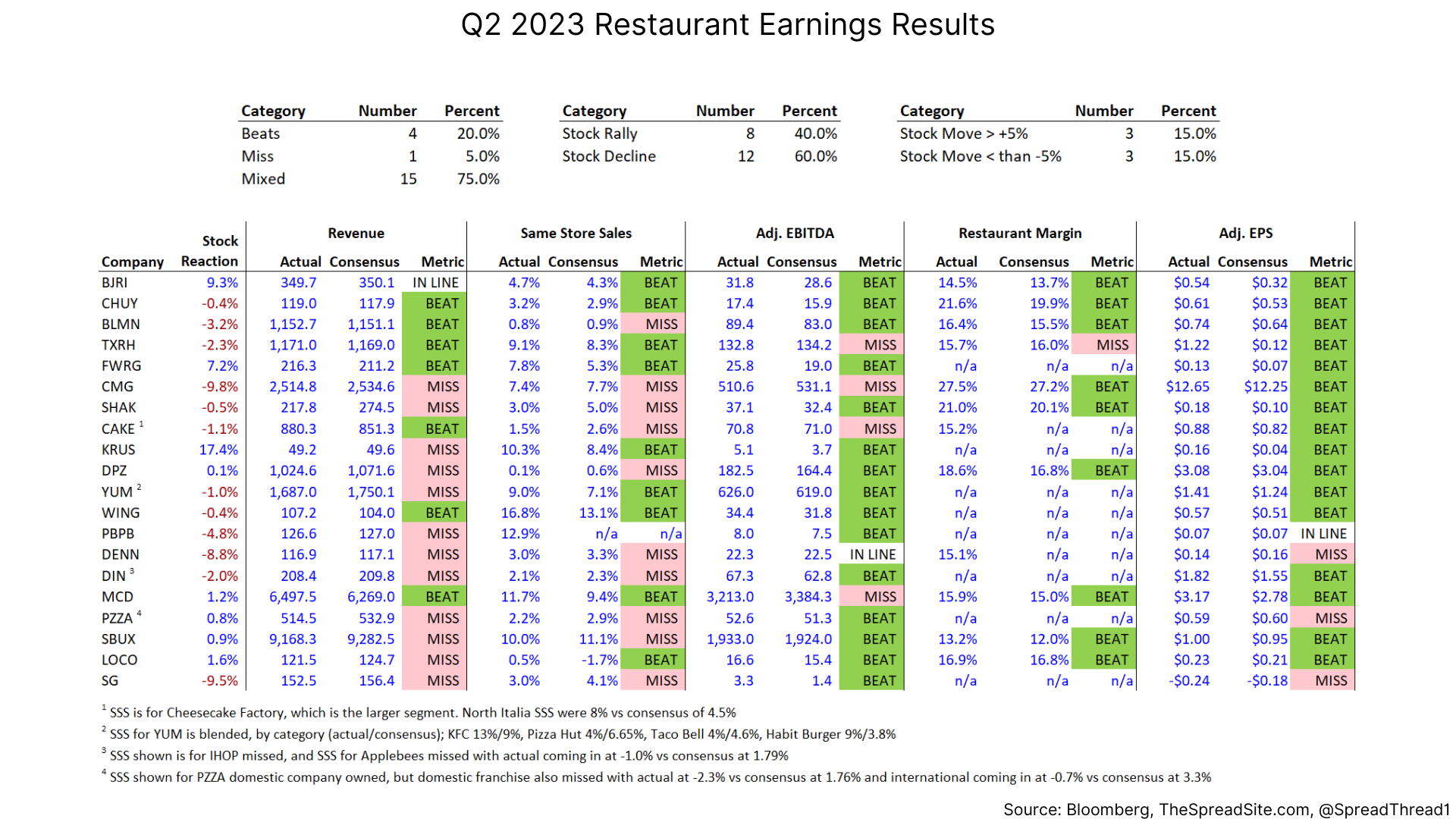

Q2 2023 Restaurant Earnings Scorecard

It is worth mentioning that US restaurants are tracked by companies that aggregate consumer credit card data and then sell this data to investors (among others). Consequently, there is usually a 'Whisper' number for sales and SSS that is different from consensus and you can get odd stock reactions on earnings releases.

Comp Sheets

Disclosures

Please click here to see our standard legal disclosures

The Spread Site Research

Receive our latest publications directly to your inbox. Its Free!.

{kind=link}