UAW Strike: Shock Wave or Ripple?

The UAW’s contract with the Big 3 (Ford, GM, Stellantis) ended on 9/14/23 and targeted strikes began that day. Contract negotiations cover ~146k workers across the companies.

In this week’s note we discuss the key facts, impacts to the auto makers and their supply chain.

Given the combination of a highly unorthodox bargaining technique by the UAW and multiple moving parts within each company, our report uses ‘Back of the Envelope’ estimates.

Bid/Ask Between Big 3 and UAW

The UAW’s master agreement is redone every 4 years, and historically they would negotiate with each company separately. This time, however, is slightly different as the UAW is using targeted strikes at each company simultaneously.

The UAW is arguably asking for a lot. There is minutia given various types of workers and structures at each company, but generally they want:

- Removal of wage tiers (varies by company, but most problematic at Stellantis and GM)

- A 36% increase in compensation, phased in over 4 years

- Restoration of a Cost of Living adjustment (“COLA”) tied to inflation (went away in ’07)

- Job security protections (in other words, less ability to lay off workers during a downturn)

- Restoration of traditional pension and retiree health care payments

- Protection of wages and benefits for workers at EV plants (seen as major sticking point)

- 32 hour work week, down from 40hrs (recent headlines indicate they are softening here)

Media headlines state the Big 3 are closer to a 20% increase in compensation, phased in over 4 years. The other categories remain a moving target as the automakers are looking at their entire cost structure and as one piece moves higher, others may move lower. Additionally, costs like job security may not show up until a downturn ensues. For this reason, we are not focusing on any one specific number. As of Friday 9/22, progress has been made at Ford, but the two sides remain far apart at GM and Stellantis.

From the perspective of the Big 3, union heavy cost structures already place them at a cost disadvantage. Including wages and benefits, the Big 3 have total labor costs of $64/hr, on average. Non-union US plants, such as those owned by Toyota are closer to $55/hr and Tesla is $45 - $50/hr according to a recent Bloomberg article. Given this US labor cost differential and the highly competitive nature of auto sales, it is very unlikely the Big 3 could increase prices to offset cost increases. And keep in mind, short-term price increases at dealers from potential inventory shortages are not prices received by OEMs as the the latter is much less variable.

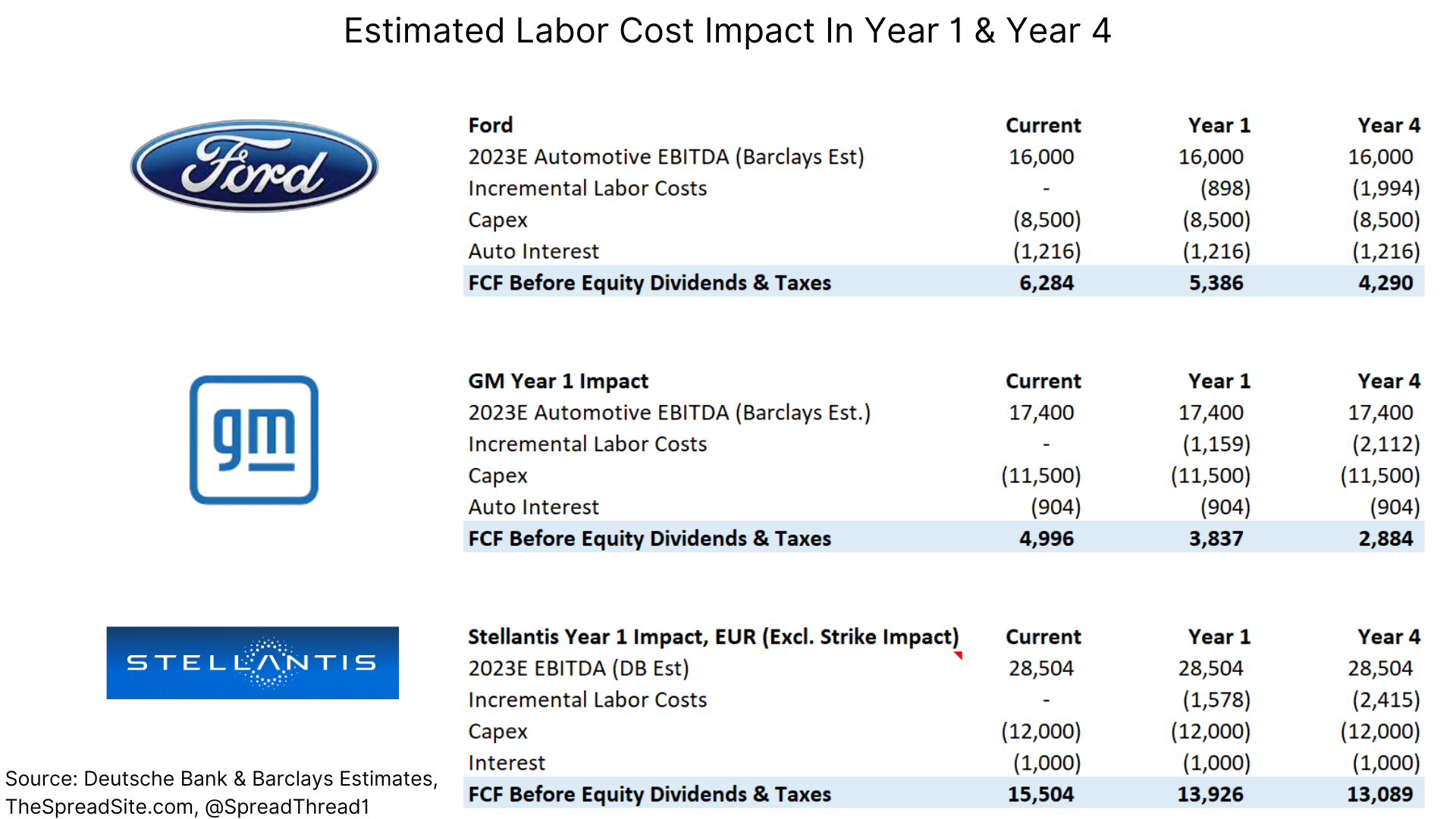

Below we attempt to put the increase in labor cost into context using estimates from Deutsche Bank. This scenario assumes a 20% increase in hourly wages in Year 1 going to 30% in Year 4. It also assumes elimination of a tiered wage system. Based on current UAW demands, this scenario should be seen as a big win for the UAW and close to a worse-case scenario for the Big 3.

Clearly this analysis is simplistic as we hold 2023E EBITDA estimates flat and don’t account for any cost cutting or other measures to offset the cost increase. We just want to show the possible cost increases relative to current operating conditions.

Generally, it is believed the incremental cost of contract negotiations will be highest for Stellantis' US business, then GM and lastly Ford. This is because Stellantis is seen as having the worst labor contract (highest temporary employees, highest tiered wage structure etc.). The impact to Stellantis on a total EBITDA basis is lowest as less than half of their EBITDA is produced from US UAW employees.

Strike & Cash Burn

Part of the problem with estimating the impact to each company is the UAW’s highly unusual strategy of targeted strikes by only a portion of their members without warning. Various media reports indicate this is partly to cause confusion among the Big 3 and to preserve the UAW’s $825mm strike fund.

With ~146k members, and each eligible striking worker getting $500/week from the union, they only have so much firepower. As an example, with half the union on strike, it would cost the UAW ~$36.5mm per week (they are nowhere near this level currently).

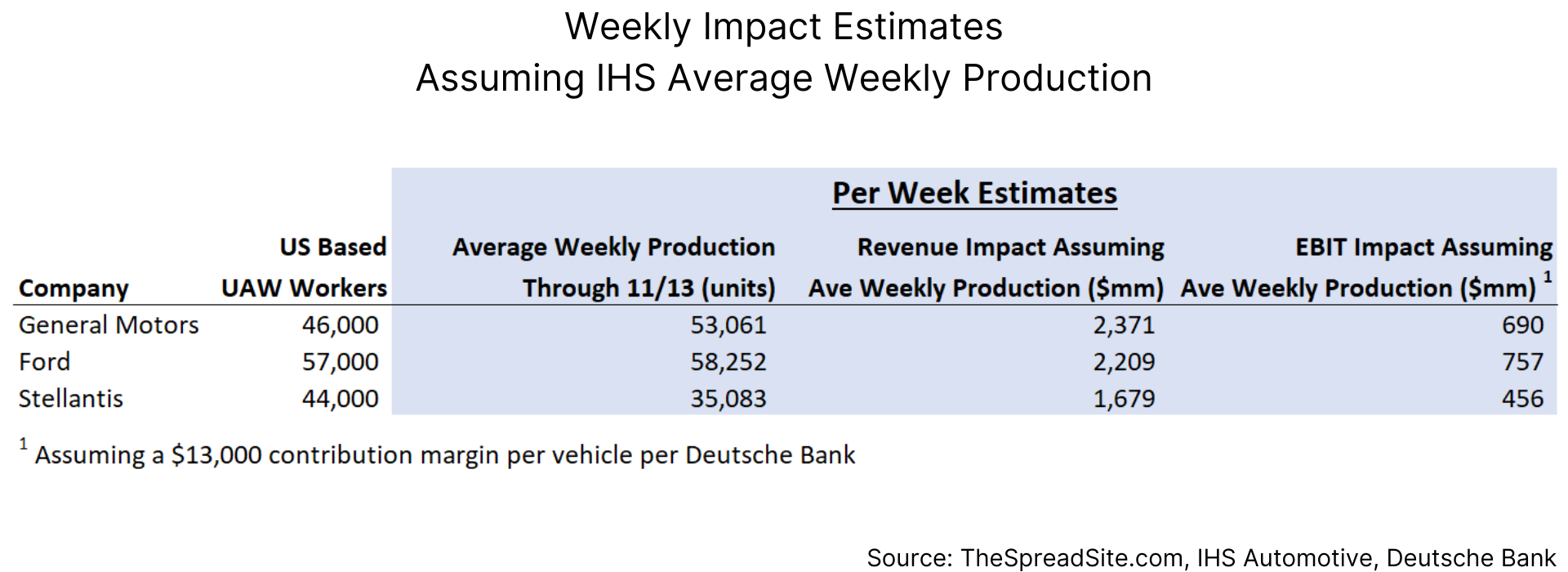

In terms of the impact to the Big 3, using IHS production data, estimated average selling prices and a $13,000 contribution margin per vehicle (per Deutsche Bank), we show a quick summary assuming a total work stoppage (i.e., all union workers strike). We note this is a worst-case scenario and do not believe lost production, revenue or earnings will be nearly this bad, with some estimates indicating closer to a $400-500mm per week EBIT impact.

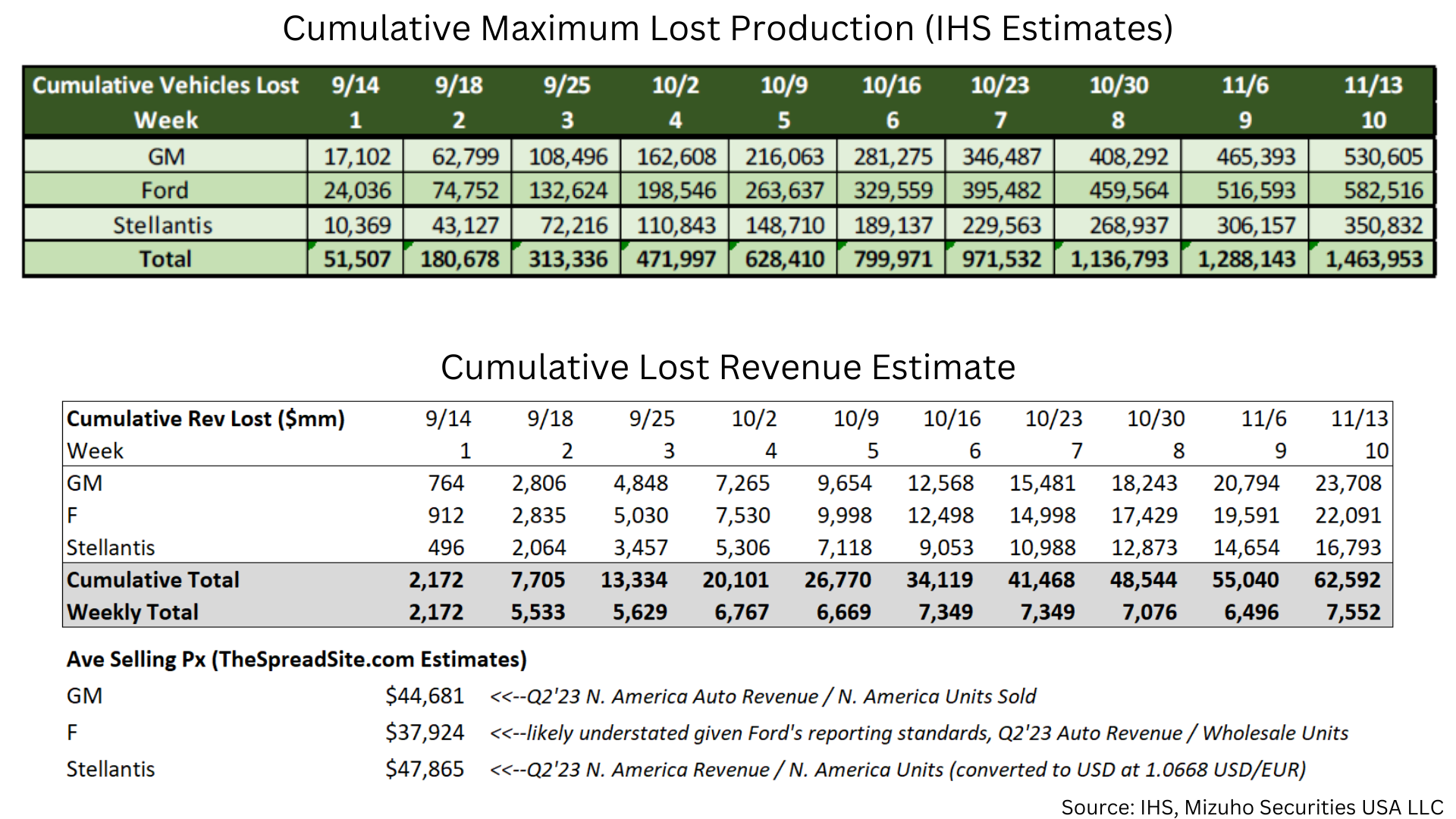

For more granularity on the above averages, the tables below provide data by week. Again, we are looking at averages between 9/14 and 11/13. The first few weeks of lost production will be less impactful.

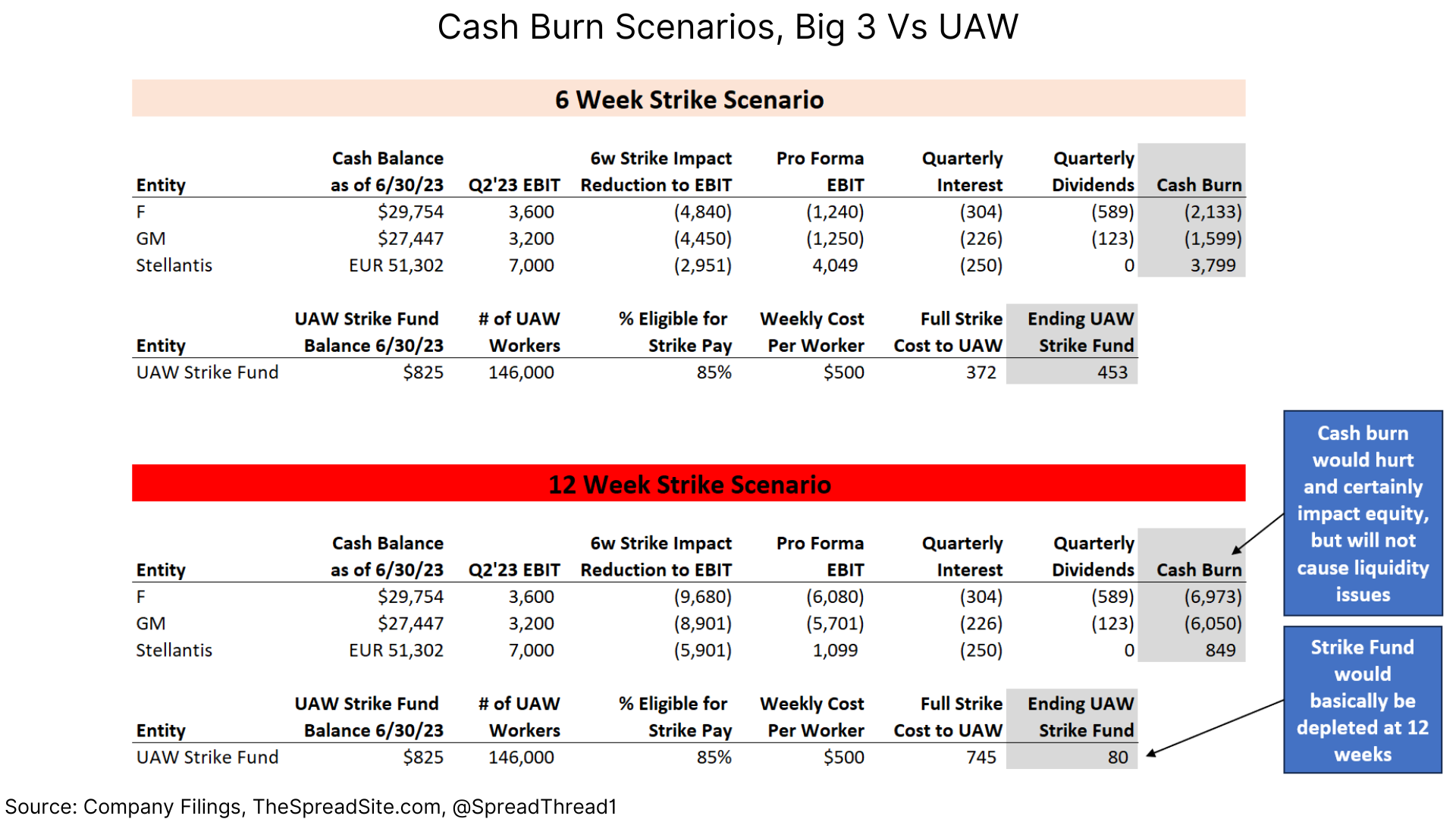

Even assuming a 12-week strike, the cash impact to the Big 3 will be manageable. The automotive divisions at F, GM and Stellantis have cash positions of $30b, $27b and EUR51b, respectively. In terms of context, the last major UAW strike was in 2019 at GM and lasted 6 weeks with a cost of $3.6b in lost EBIT.

As we show below, the Big 3 can “outlast” the UAW in terms of liquidity as the latter would essentially run out of funds in their strike fund in a 12 week “full strike” scenario (all union workers walking off the job). Furthermore, UAW workers receiving $500/week for striking would be taking home less than 50% of their normal pay.

Again, this analysis is very high level given the myriad of moving parts. It is simply meant to frame the discussion. And note that Stellantis does not actually burn cash given their limited overall exposure to the US market.

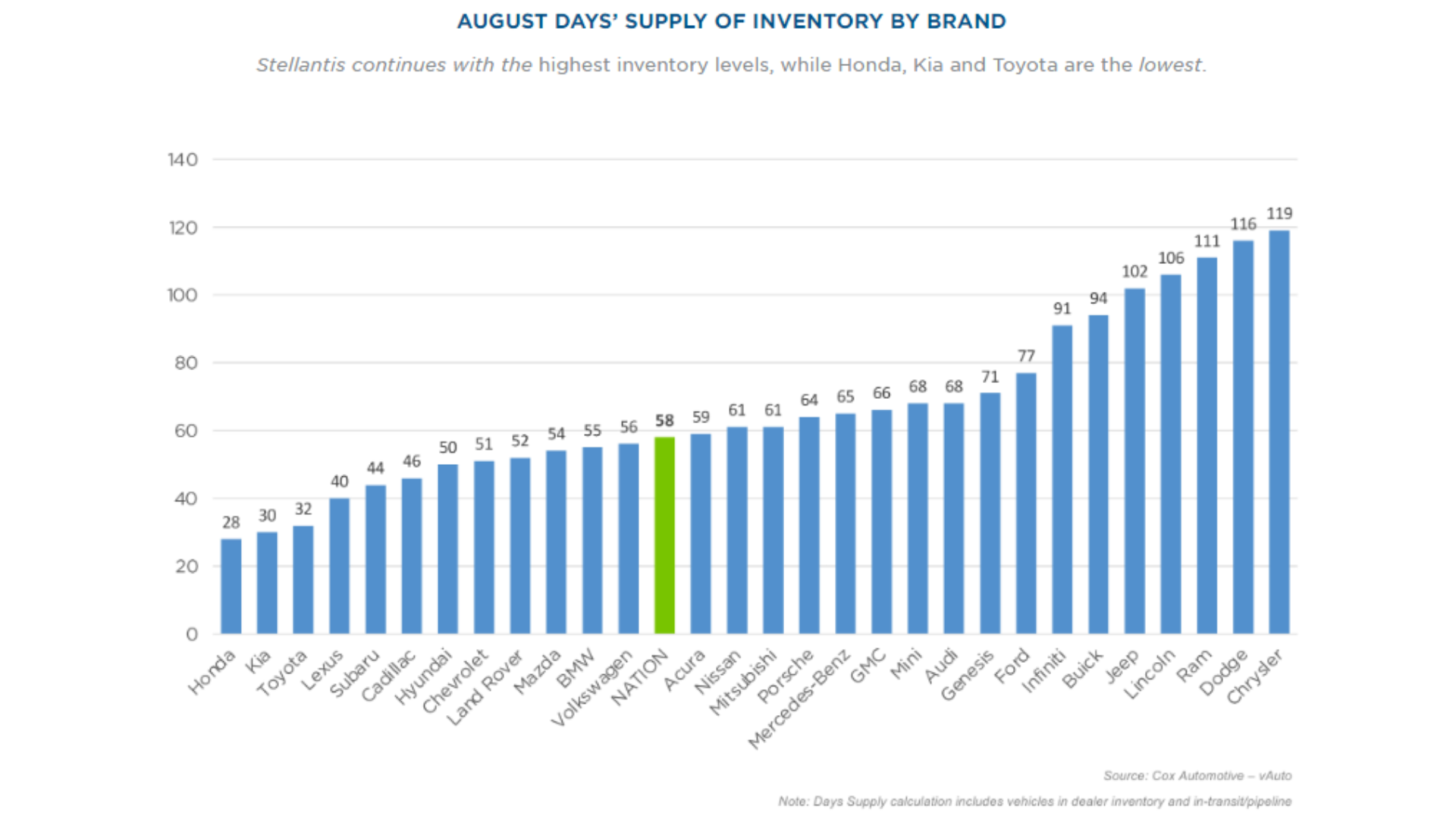

Inventory does not appear problematic, for now. According to Cox Automotive, inventory levels nationwide are around 60 days, which is average. Overall, the Big 3 are slightly higher than this with differences depending on the vehicle. But Cox notes higher priced vehicles (more profitable) are higher in terms of days of supply. However, media outlets are already reporting new and used prices at dealerships already moving higher in anticipation of future inventory shortages. And to reiterate the point made earlier, higher prices would be realized by the dealer and not the automaker.

Corporate Credit Implications

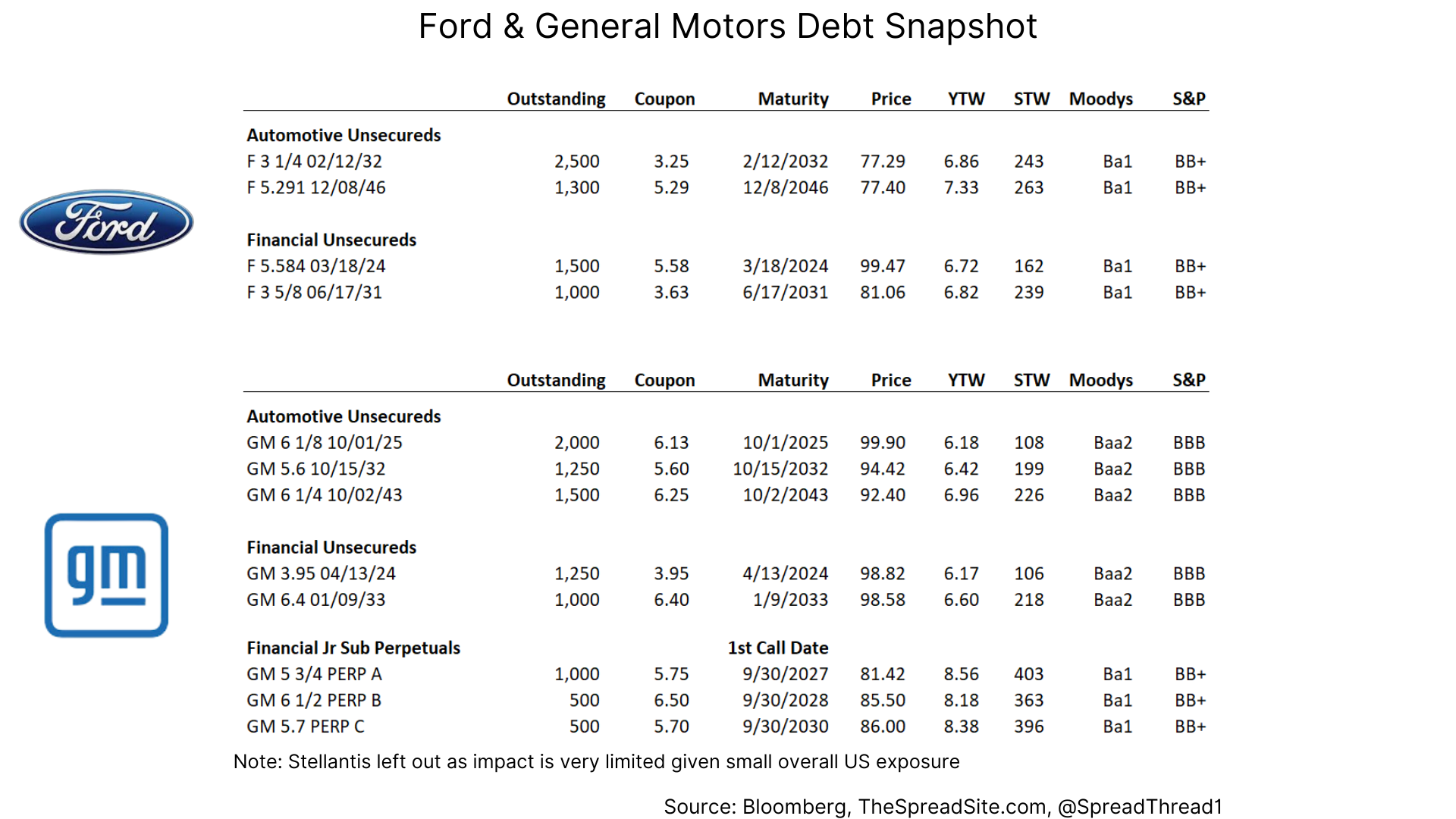

In terms of what this could mean for the Big 3 securities, as always, it depends. Generally, we don’t think any scenario will significantly impact shorter dated fixed income securities. The Big 3 have significant liquidity and very low leverage. The equity, however, is a different story. A prolonged strike will impact EBIT, and a big win by the UAW will significantly increase cost structures. As to what is priced in, we are not close enough to any of the companies to opine on the equity. But unsecured bonds at Ford and GM have not reacted in any meaningful way and we think this makes sense given leverage and liquidity.

The longer-term risks of higher cost structures also depend on contract terms. GM, for example, fought very hard during their bankruptcy to make their cost structure more variable. To the extent the UAW wins major “job protections,” this could limit the ability of each automaker to reduce costs during a downturn and increase the likelihood of a future bankruptcy, in our view.

Reverberations To Supply Chain

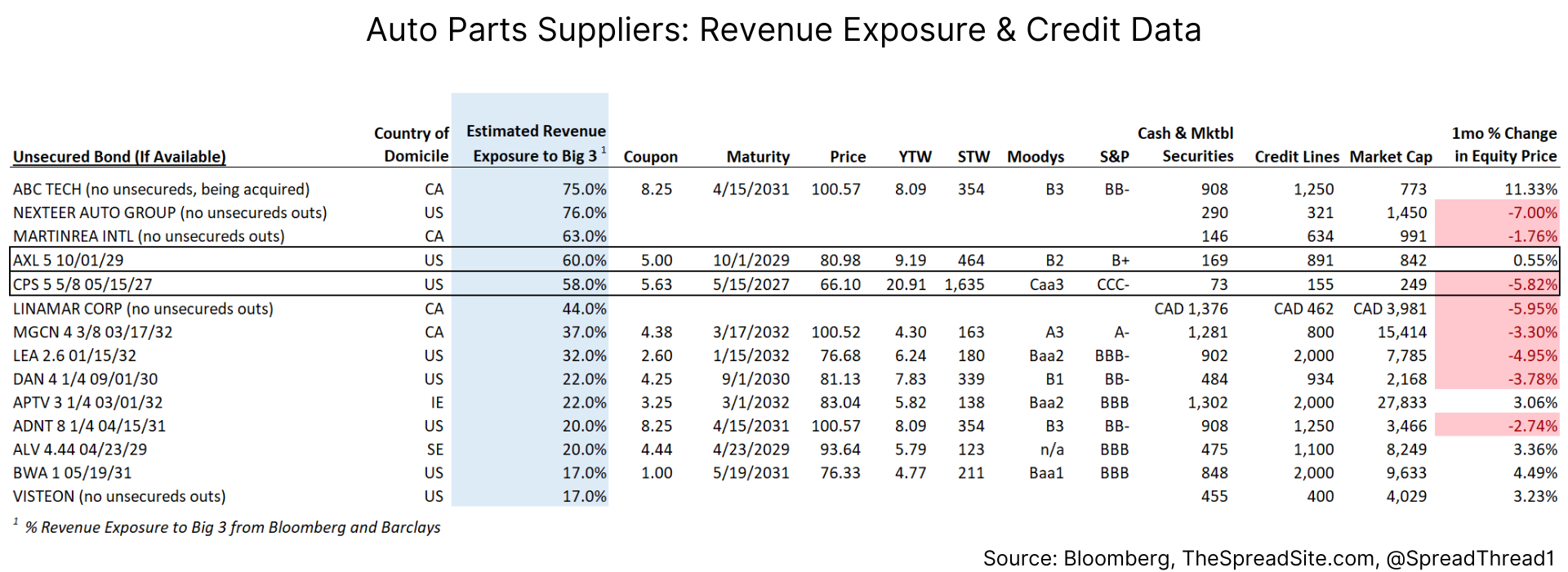

The automotive supply chain is exceedingly complex and news reports have indicated everything from auto parts to steel and semiconductors could be impacted. While we don’t have enough information to discuss the entire supply chain, we can show some of the parts suppliers with significant UAW exposure.

Judging by some high level credit metrics, it appears most companies will be able to manage. Cooper Standard (“CPS”) and American Axle (“AXL”) do stand out as suppliers that may run into trouble.

Conclusion

In such a competitive business, cost structure is vitally important. We do not have a strong view on where negotiations ultimately land, but it is fair to say the labor costs for the Big 3 will go higher. We do not see significant liquidity impacts to the Big 3 based large-scale strikes or extended production impacts. In terms of longer-term impacts, it will depend. From a credit perspective, we would view major concessions on job protection in a downturn as most concerning.

Disclosures

Please click here to see our standard Legal Disclosures

The Spread Site Research

Receive our latest publications directly to your inbox. Its Free!.

{kind=link}