Yellow Corp ("YELLQ"): A Ch.11 Liquidation With Multiple Moving Pieces

Chapter 11 & Pre-Petition Equity

On August 6, 2023, Yellow Corporation filed for Chapter 11 under the US Bankruptcy code, case# 23-11069. For case information, a list of advisors, and all public documents you can visit the case management website here.

Given a long history of liquidity and union problems that we won't go into, the company is now liquidating. While Chapter 7 is usually associated with liquidations, companies can liquidate through Ch.11, which allows a more orderly sale of assets. And this is the route Yellow is taking.

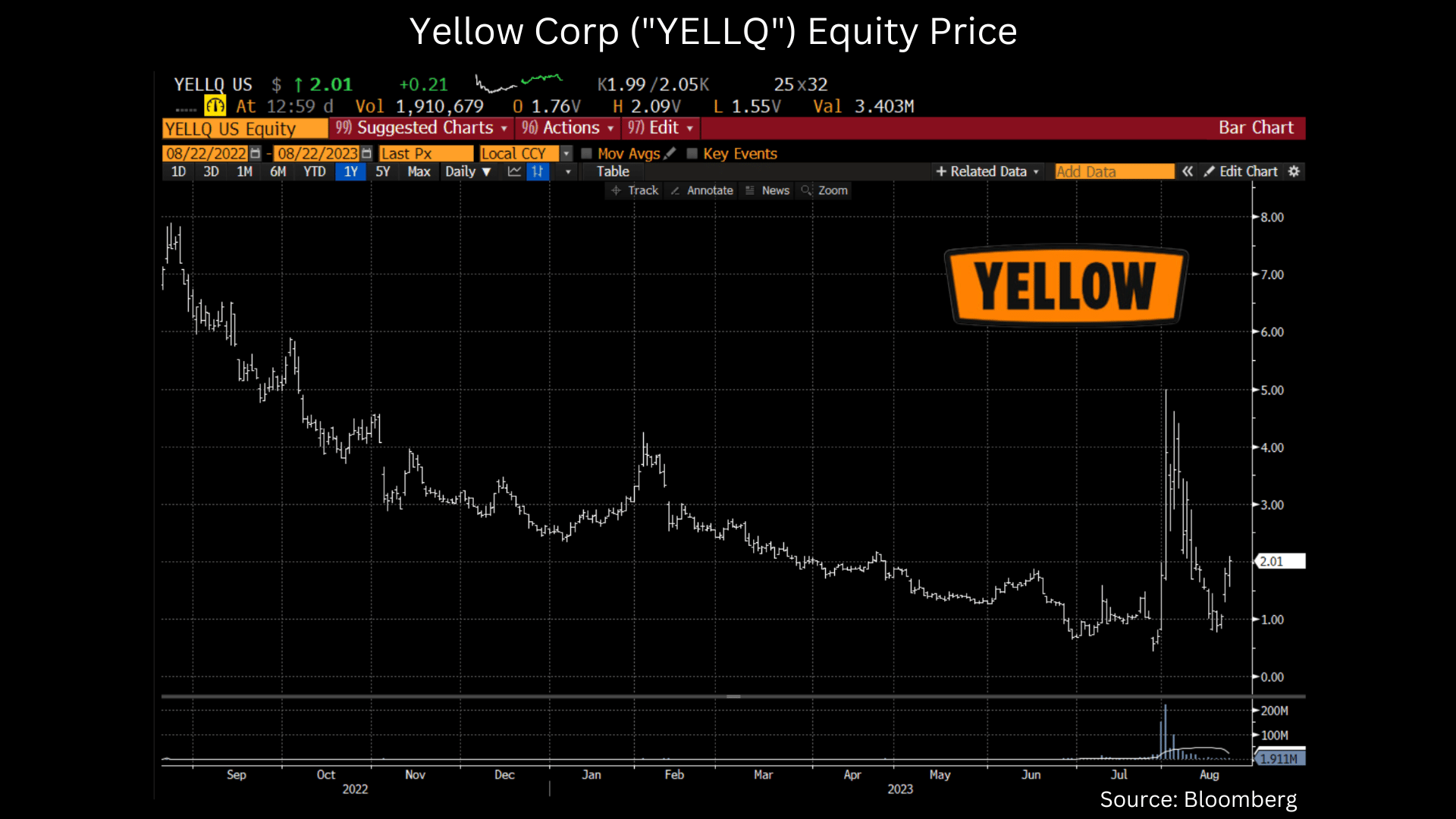

Bankrupt equities can also be conflated with "meme stocks", and while we acknowledge the run up to $4.00+ in early August was likely more in the meme camp, we want to illustrate the moving pieces that will indicate whether equity gets a recovery in this bankruptcy.

While rare, equity can retain value during a bankruptcy as was the case recently with Hertz ("HTZ"). But it is important to remember that pre-petition equity is the most subordinated piece of the capital structure with limited legal arguments on recovery unless all classes of creditors are paid in full (usually referred to as the Absolute Priority Rule).

We also want to be clear in saying that when evaluating bankrupt equities, they should be viewed as options as a probability must be placed on getting zero (the actual % is always debatable and influences the option value). The reason is that if under a Plan of Reorganization, pre-petition equity is ruled to get zero, it is game over and there is no chance of waiting on a recovery.

In this situation, we think it is too early to put a probability on getting zero, but we don't believe it is 100%, and walk through the moving pieces below.

Yellow Corp ("YELLQ") Assets

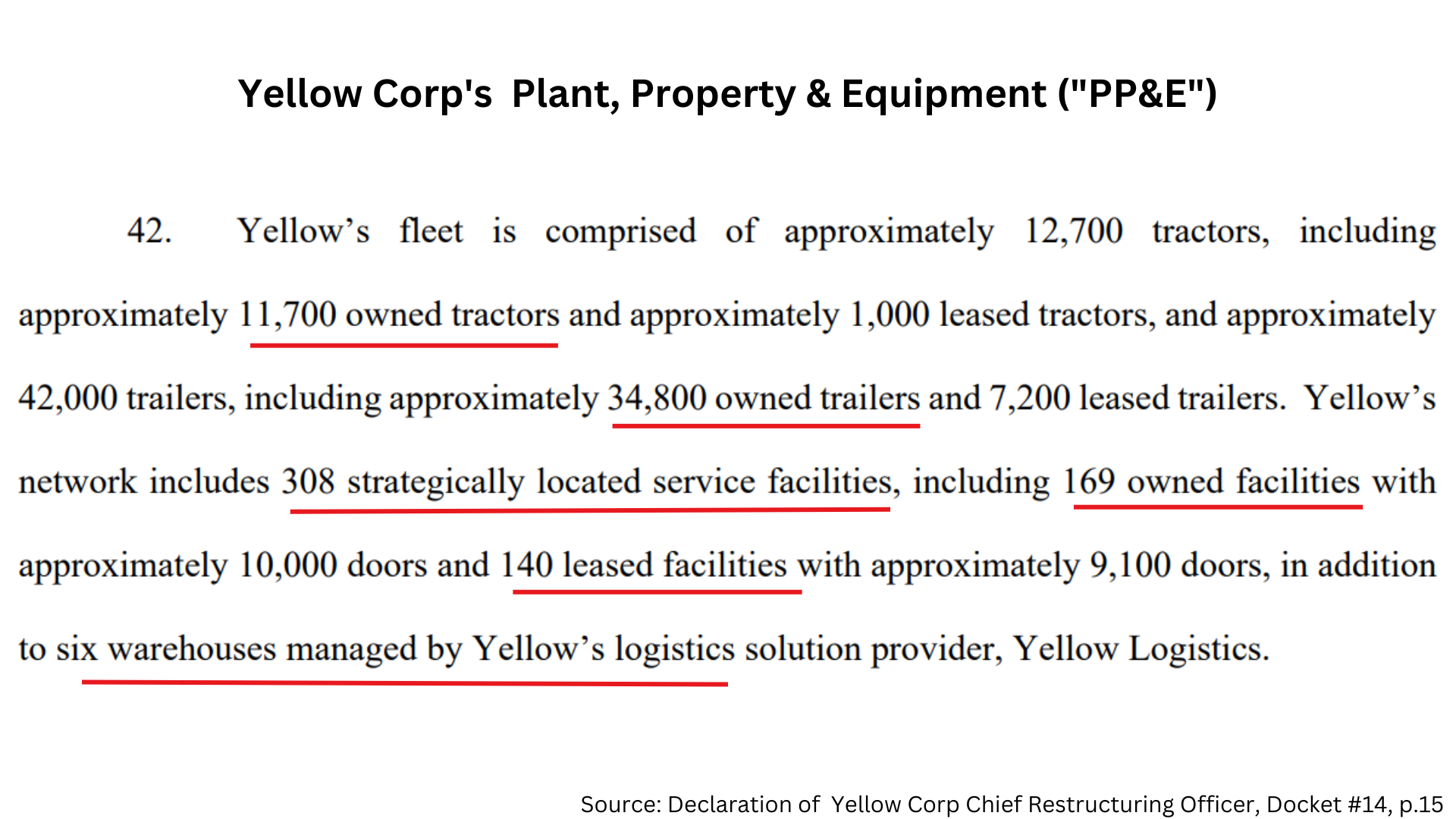

Let us first take a look at Yellow's assets, as described in court filings:

As can be seen, there are four major categories of PP&E:

- Tractors: 11,700 owned / 1,000 leased

- Trailers: 34,800 owned / 7,200 leased

- Service Facilities: 169 owned / 140 leased

- Warehouses: 6 managed by Yellow Logistics

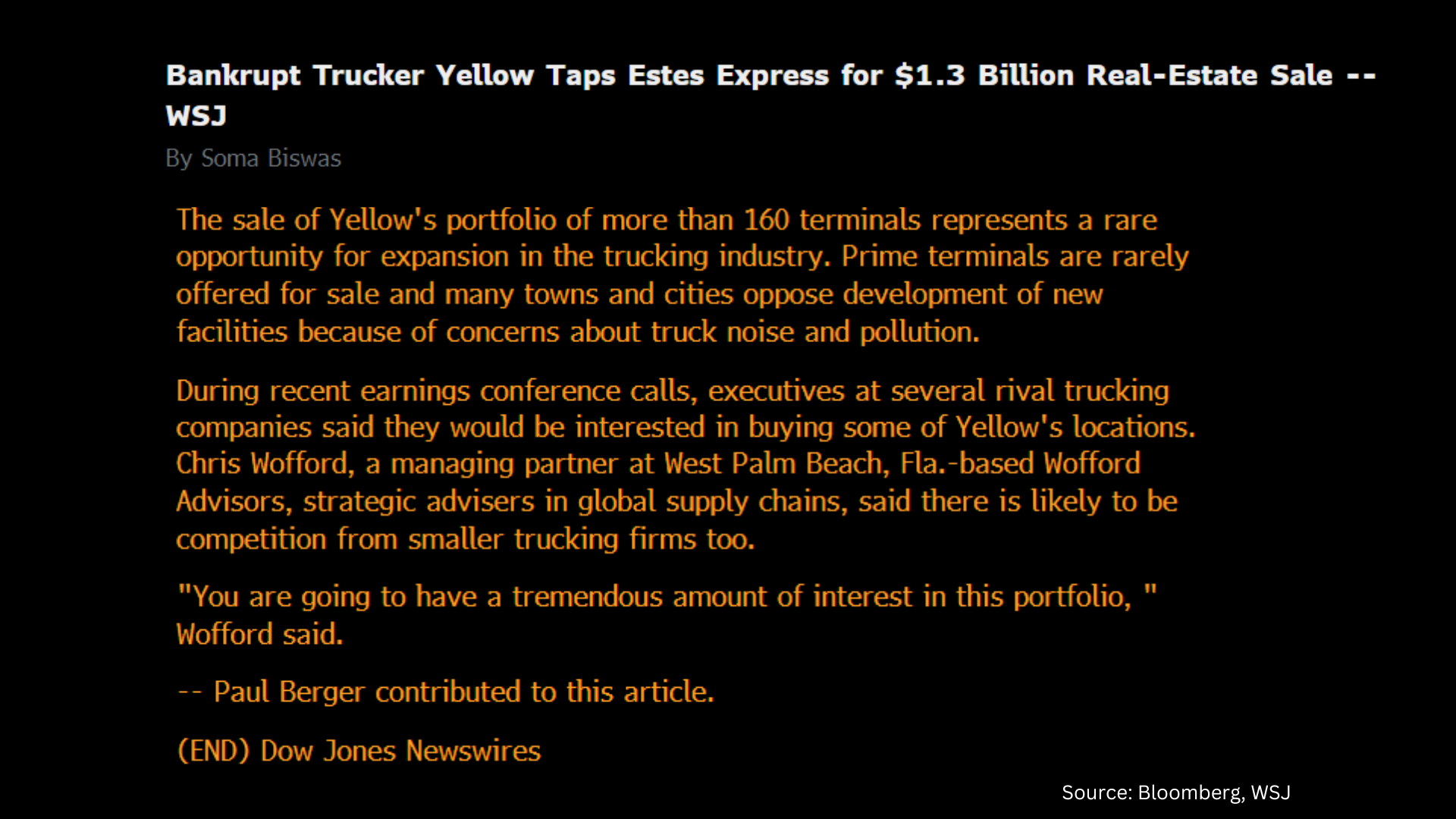

So far, the Service Facilities have received the most attention with two active bidders, Estes Express (private) and Old Dominion ("ODFL"). But, another 63 companies have executed confidentiality agreements and are also evaluating the assets.

Estes initially bid $1.3b for 166 owned terminals as FreightWaves describes here. And a few days later, their bid was topped by Old Dominion coming in at $1.5b as was described by the WSJ.

A Service Facility is a large piece of real estate where trucks can load and unload freight. We aren't experts here, but apparently they are very difficult to build and given their size, zoning and noise issues are an impediment to new construction.

A few trucking executives even highlighted their value on recent earnings calls, as the WSJ describes below.

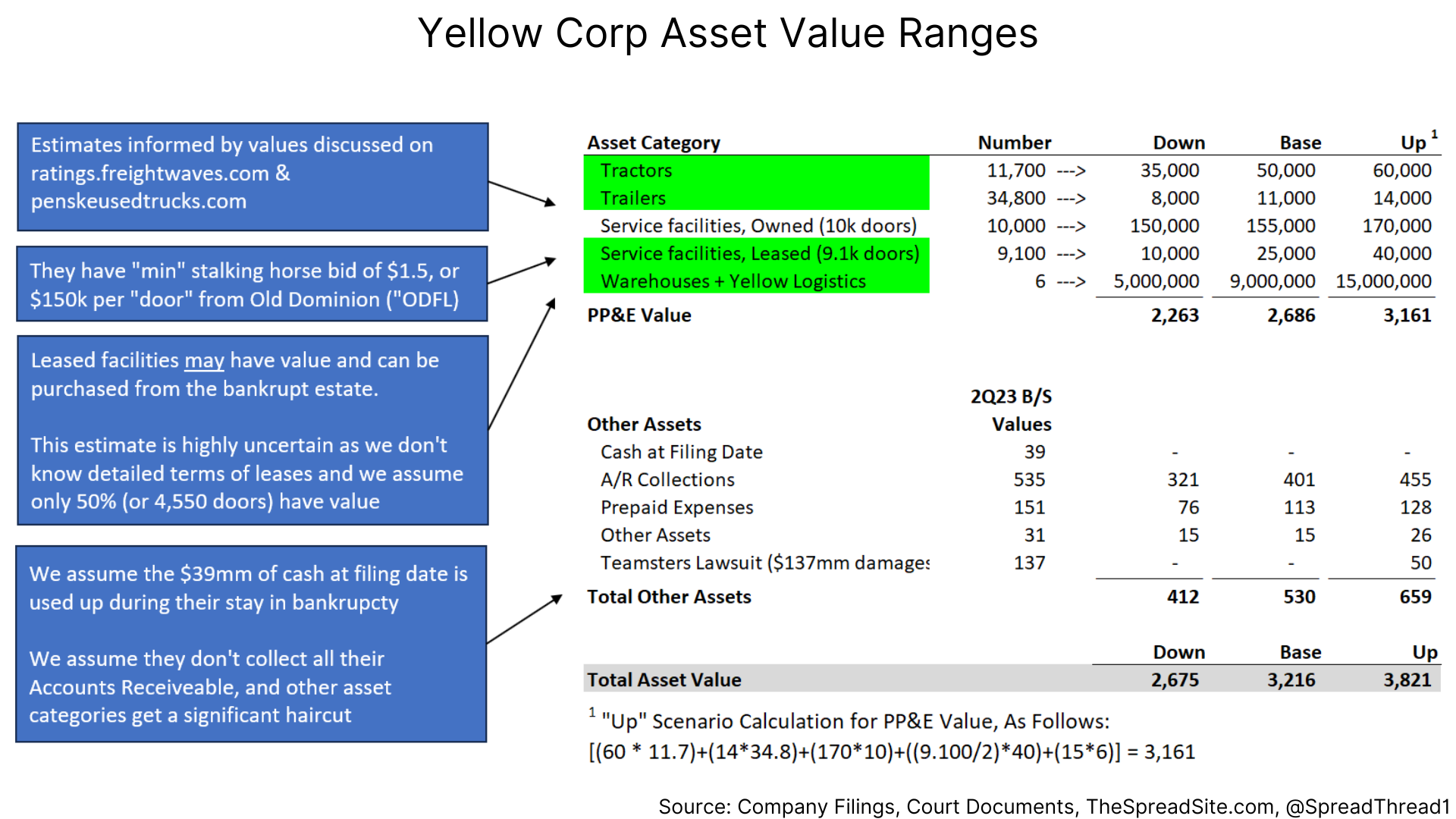

The leased terminals may also have value and could be purchased out of bankruptcy. However, it is very difficult to assess these assets given we don't know the terms of the leases.

Their tractors and trailers have value too, but there is probably less fluctuation here. Again, we don’t know details around their average age, mileage, or quality, so there is more uncertainty. However, there are a few online resources such as Penske and FreightWaves that we used to provide goalposts around unit values.

Putting it all together, we show a range of asset values below, noting that the case is at early stages and we have limited disclosure on some large categories that will dictate sale proceeds.

Yellow Corp ("YELLQ") Liabilities

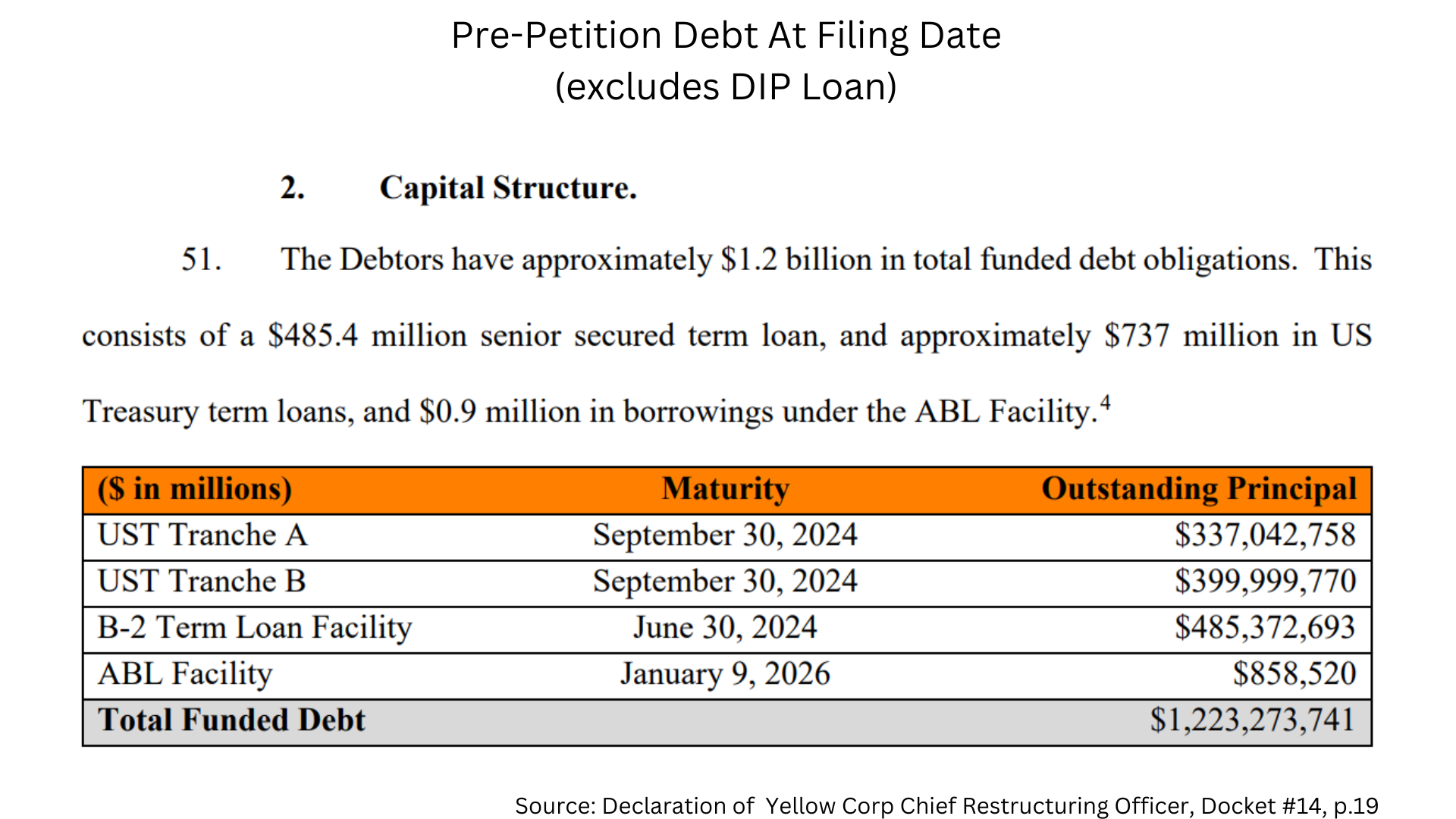

We know the amount of secured debt owed as of the bankrupty filing date, which is described in court documents and shown below.

In addition, Yellow will get a Debtor-In-Possession ("DIP") loan, which provides funds so they can operate and pay professional fees while assets are liquidated. This DIP loan is being provided by Citadel and MFN Partners, both of which are hedge funds. There are a few moving parts to the loan and we assume the initial piece of $142.5mm will be fully drawn without subsequent draws (for now).

A few key terms, per Petition are as follows:

- Amounts: $100mm from Citadel, $42.5mm from MFN Partners

- Interest Rate: ABR+8.5% for Citadel, 15% for MFN, both are per annum

- Fees: 4% on amount funded, paid to both Citadel and MFN

- Term: 6 months

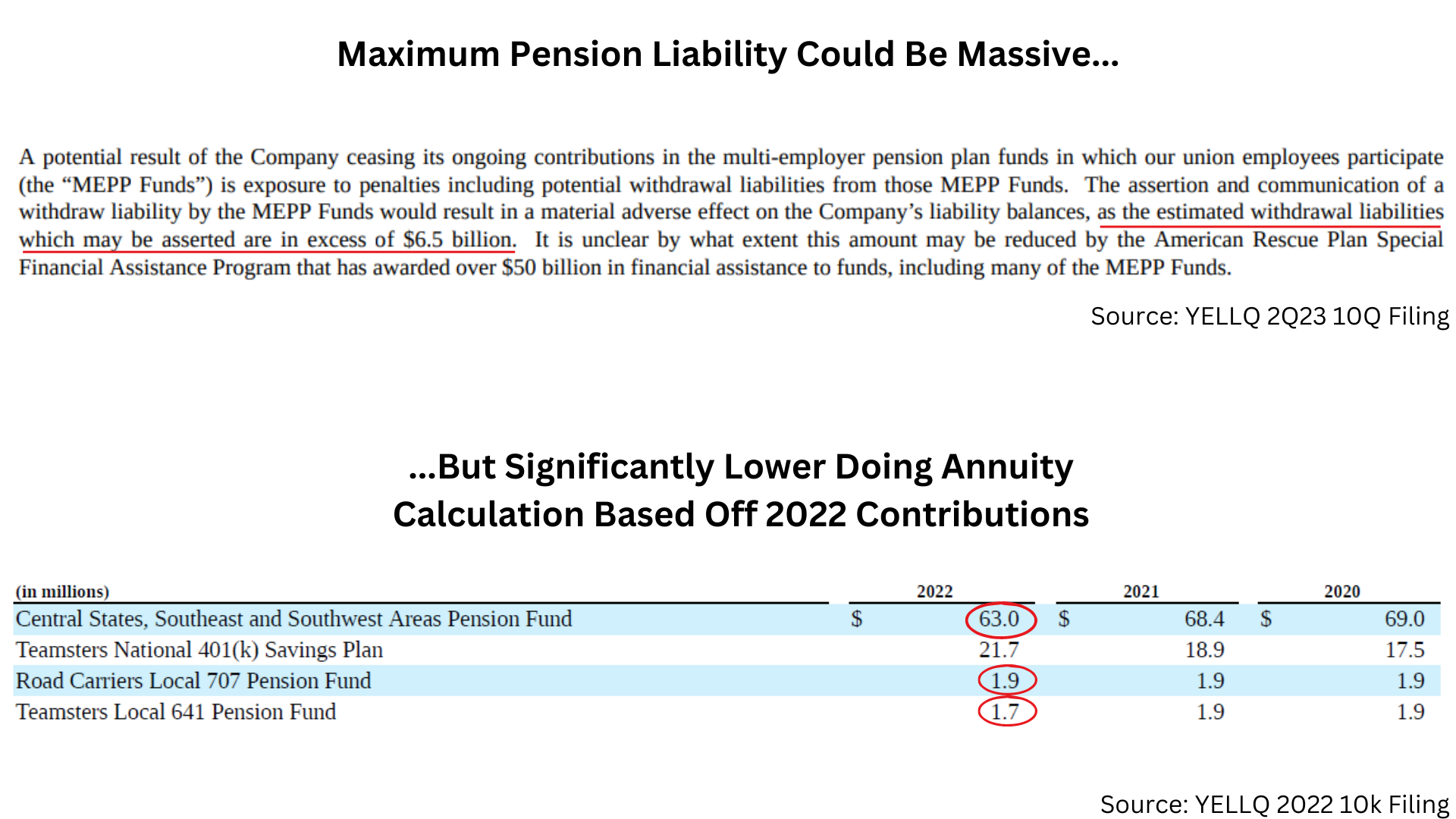

In terms of other liabilities, the most impactful will be the withdrawal liability from their multi-employer pension plans ("MEPP"). This is a very complex issue and will certainly be a bitter fight during the case.

When Yellow withdraws from their union pension plans, they will face a liability owed on future funding payments (capped at 20 years) that will not be paid. This liability will be an unsecured claim and increase the size of the unsecured claims pool. If large enough, it could reduce recoveries for unsecured creditors and (potentially) leave nothing for equity.

The liability debate centers on Yellow's largest pension plan, Central States, receiving $35.8b in funding from the American Rescue Plan Act of 2021. This infusion allowed the pension plan to be nearly fully funded and lowered Yellow's annual contribution requirements. However, the PBGC has stated that funding from the American Rescue Plan should be phased in over time when calculating a withdrawal liability, as the lawfirm Morgan Lewis describes here. In other words, both the PBGC and Central States will argue that Yellow's liability is higher. Again, We are not pension experts, but it is clear there is a massive bid/ask spread on this withdrawal liability.

At the high end, the claim could be $6.5b (as we show below).

At the low end, the claim could be <$782mm, depending on the assumptions used. We get to this number based on 2022 payments of $66mm and using a discount rate of 5.7% (Yellow's non-union pension plan discount rate estimate). This gives us an annuity value of $782mm.

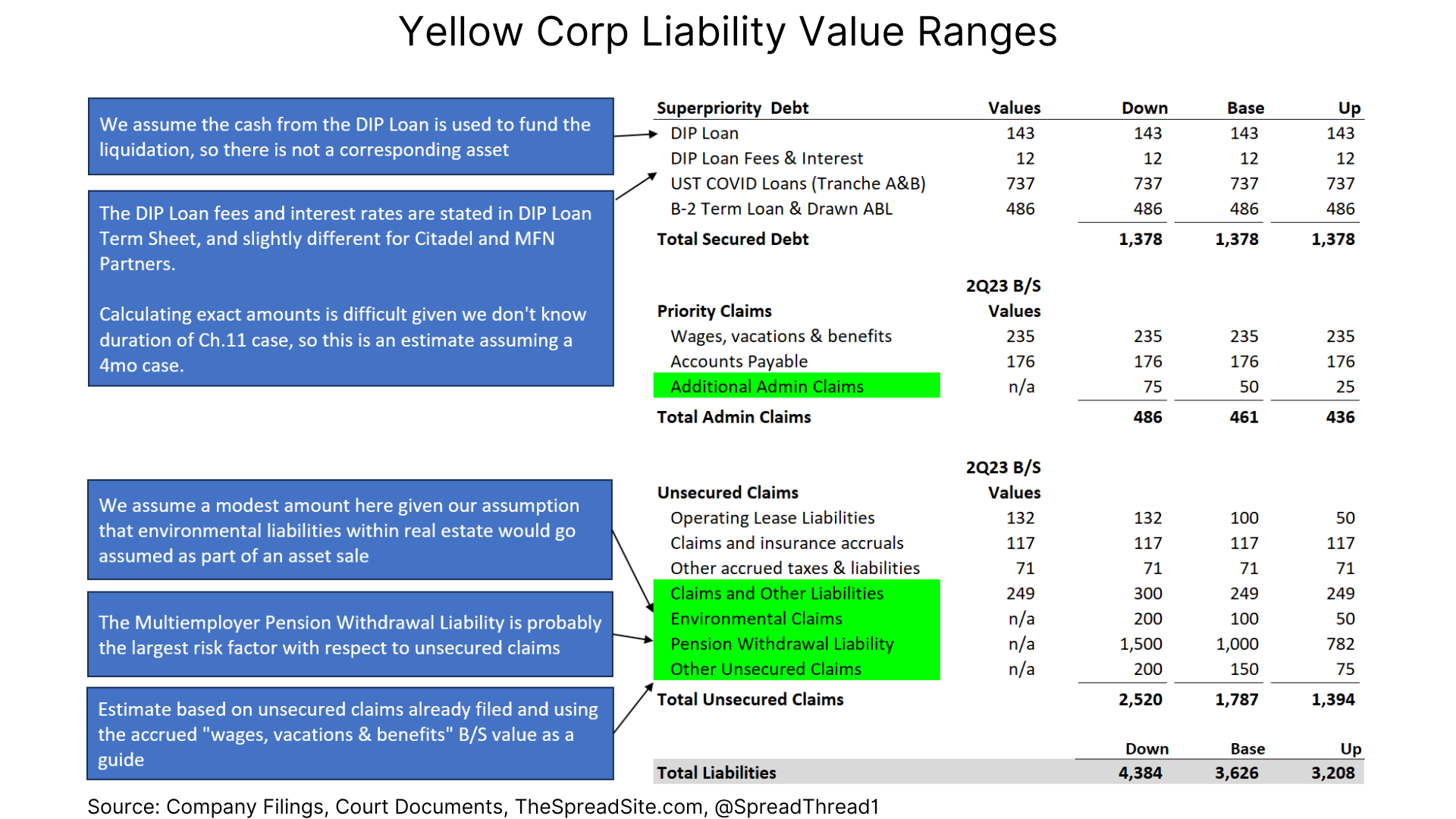

So attempting to put the liabilities together, we get the set of ranges shown below. Again, take note that the case is at early stages and we could be off on multiple categories.

However, we think the pension withdrawal liability will be the key unsecured claim to watch.

Hope For Equity?

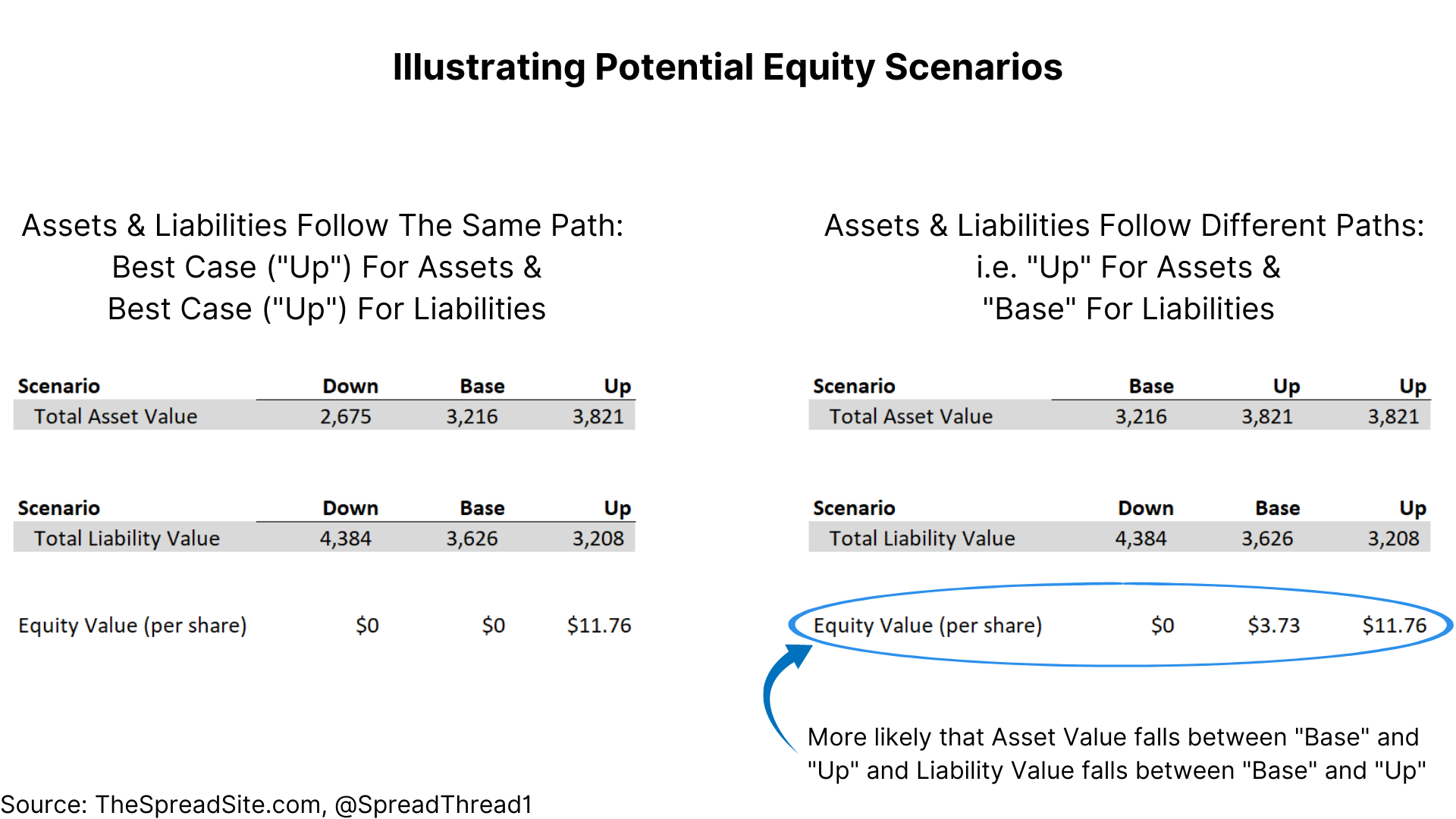

With ranges on both the assets & liabilities, we can see the moving parts that may allow an equity recovery, which we show below.

In our example, we have scenarios for both asset and liability values. While the table on the left assumes both values follow the same path (i.e. best case outcome for assets ("Up") and liabilities ("Up")), this is unlikely.

In reality, the scenarios will likely be mixed (i.e. "Up" on asset values, "Base" on liabilities), or any combination of down/base/up.

Based on our understanding of the pension withdrawal liability so far, Yellow would need the "Up" scenario on asset values for any hope of an equity recovery. But we are eager to learn more once documents are filed debating how this claim should be treated.

Yellow has 52.1mm shares outstanding and at ~$2.00/share, a market cap of ~$100mm. As the table above illustrates, small changes in assumptions will have a big impact on share price and any recovery.

Given how sensitive equity value is to these assumptions, we want to caveat that our liquidation analysis is simplistic. We are not using a true waterfall or rolling 13 week cash flows to more accurately model the duration of the case and we are not probability weighting the scenarios. We are simply trying to illustrate the main drivers behind any chance of equity seeing a recovery.

Yet, hedge fund MFN Partners does own 42% of the equity and a portion of the DIP Loan, so they will be able to steer the process and are incentivized to maximize asset values and minimize liabilities. Furthermore, the DIP Loan Term Sheet, filed on 8/18/2023, mentions the allowance for professional fees may provide up to $1mm for an equity committee. And we expect one to form in this case.

As to why MFN Partners has been buying the equity; they likely know freight logistics very well since ("XPO") is their largest position and see upside in YELLQ’s assets. With their holdings at <1% of the overall fund, it will not be catastrophic for them if the equity goes to zero.

Disclosures

Please click here to see our standard legal disclosures.

The Spread Site Research

Receive our latest publications directly to your inbox. Its Free!.

%3A%20A%20Ch.11%20Liquidation%20With%20Multiple%20Moving%20Pieces){kind=link}