Assessing the Damage

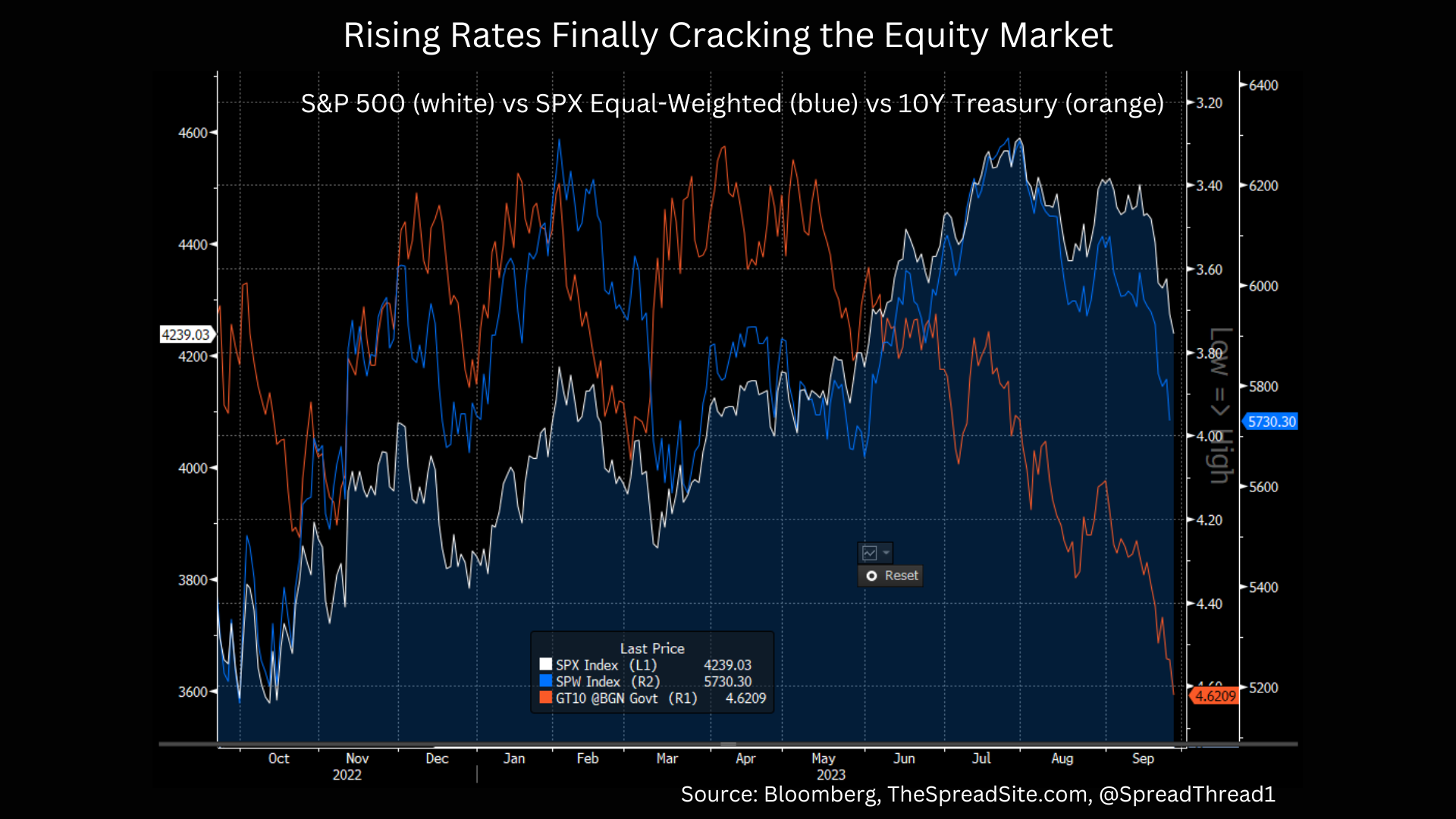

- Digging under the surface, we think markets are giving some important late-cycle messages. In short, any hint of an early-cycle re-acceleration is gone with sectors most sensitive to weakening credit, rising rates, and a slowing consumer rolling over– such as small-caps, banks, and consumer stocks.

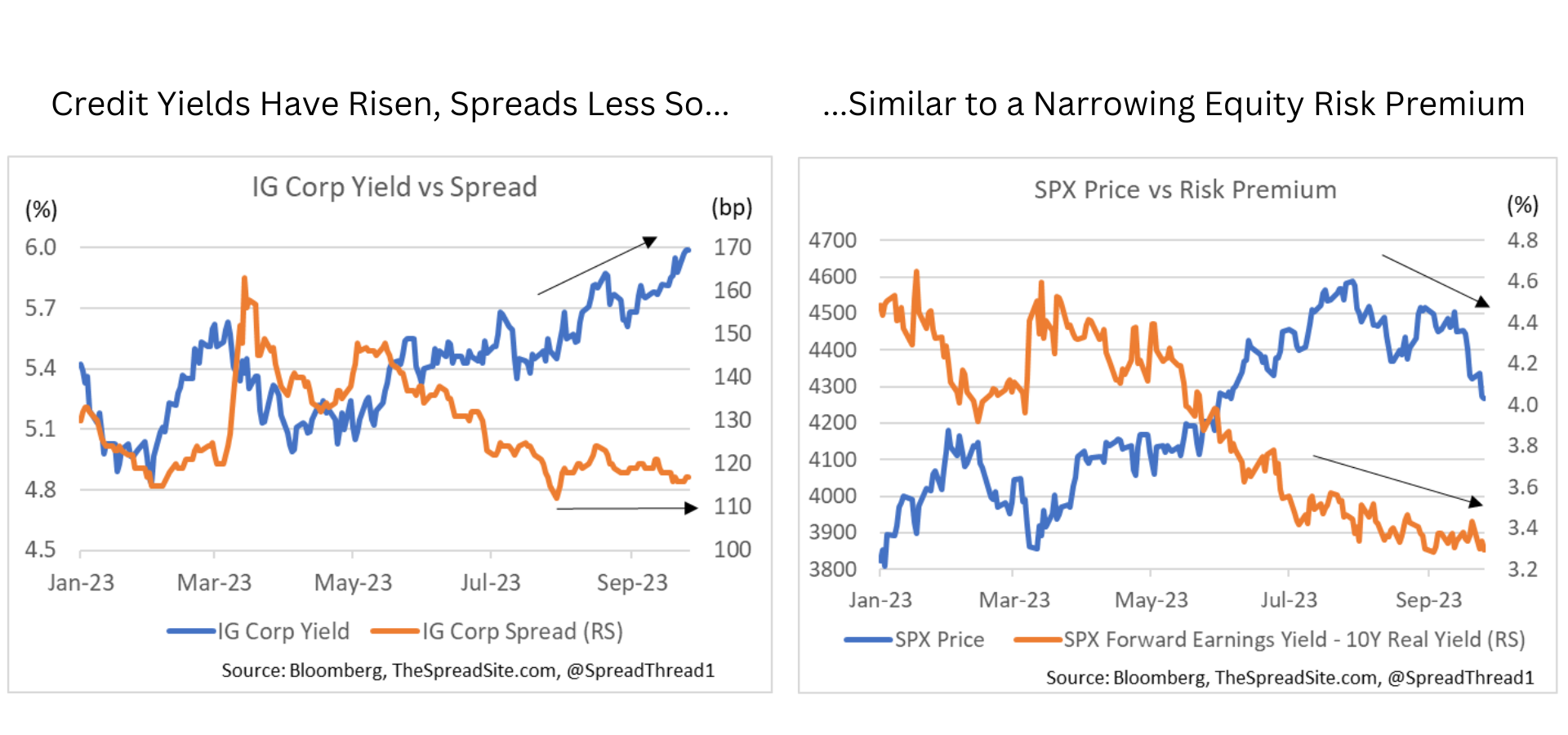

- In credit, IG yields are back near cycle highs, but spreads have been better behaved. This is actually not that different from stocks, where the decline in prices has also come from rising rates, not from cheapening relative valuations (i.e., the risk premium has fallen).

- The key question- was this just a correction, or a resumption of what began in early 2022? We still think this tightening cycle ends in a hard landing, and the final move lower will come when jobs crack, and the Fed is slow to react. That selloff will be driven by risk premium widening (unlike today), i.e., underperformance of stocks and credit vs Treasuries.

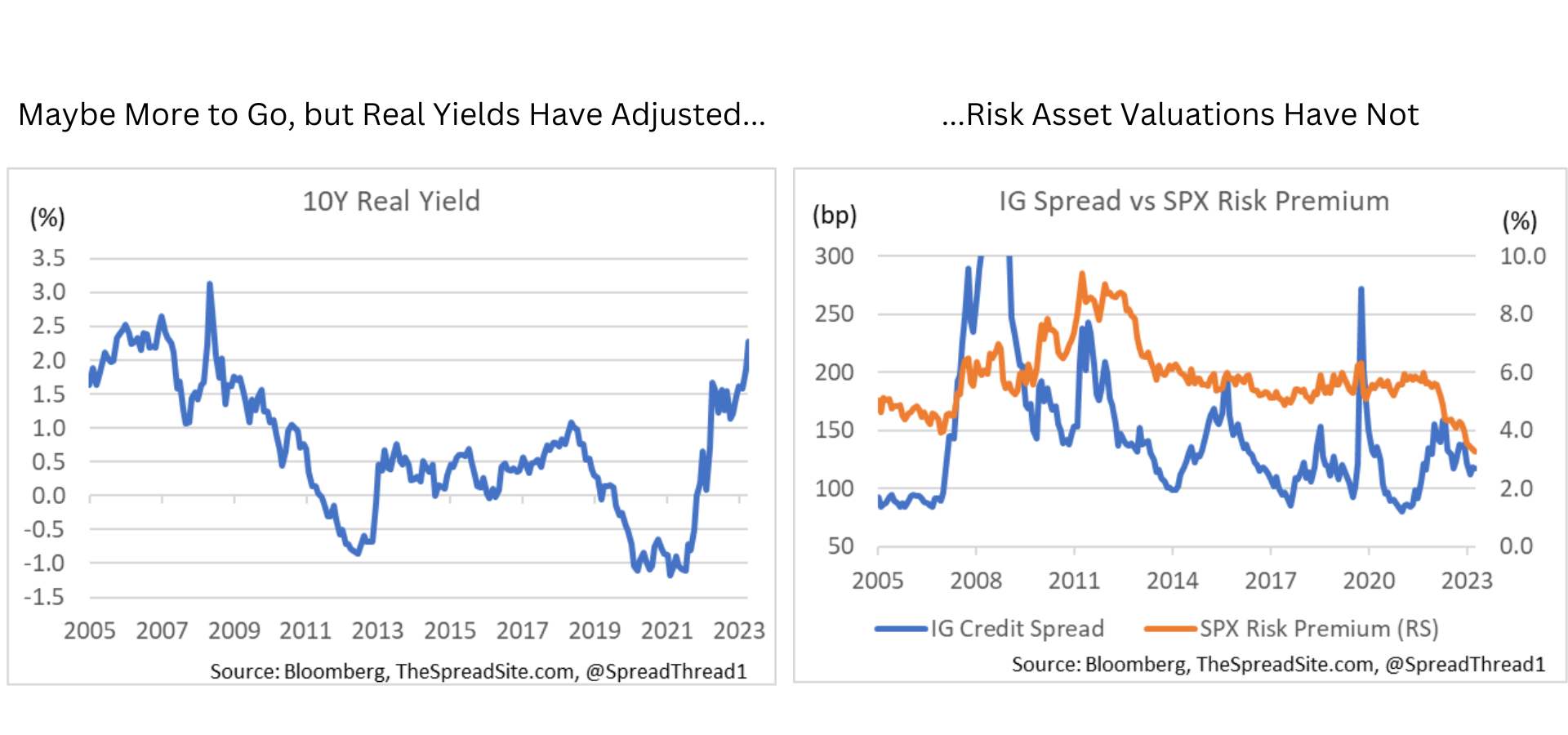

- Treasuries may be rich in absolute terms (not our view) but any way you slice it, we think risk assets are richer. Despite our cautious view, we have covered some of our shorts, looking to re-engage if markets bounce. Lastly, we think defensive sectors are decent buys after this recent pullback.

The Lay of the Land

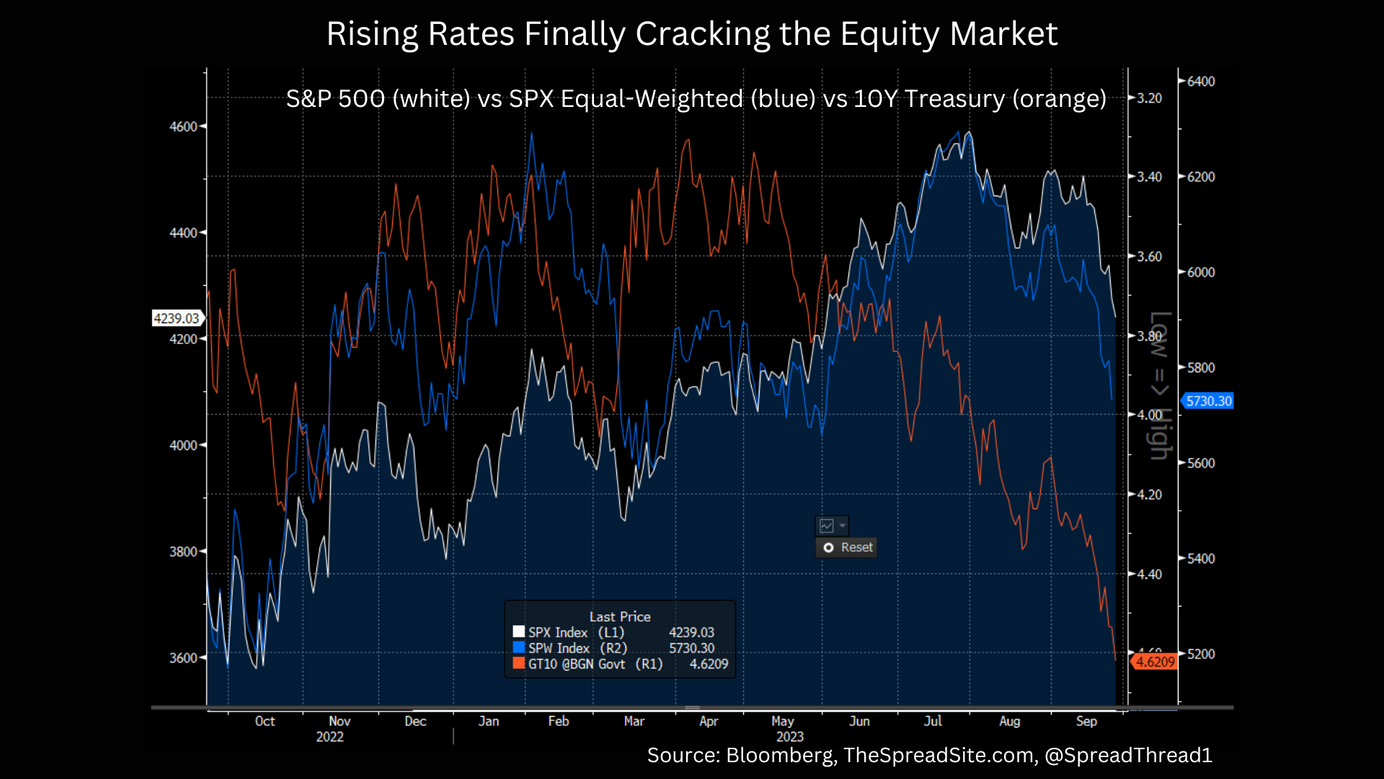

Risk assets continue to correct, driven by a sharp move higher in bond yields, with the S&P 500 down 7% from YTD highs as we write. The S&P equal-weighted index has dropped 9%, giving up all YTD gains.

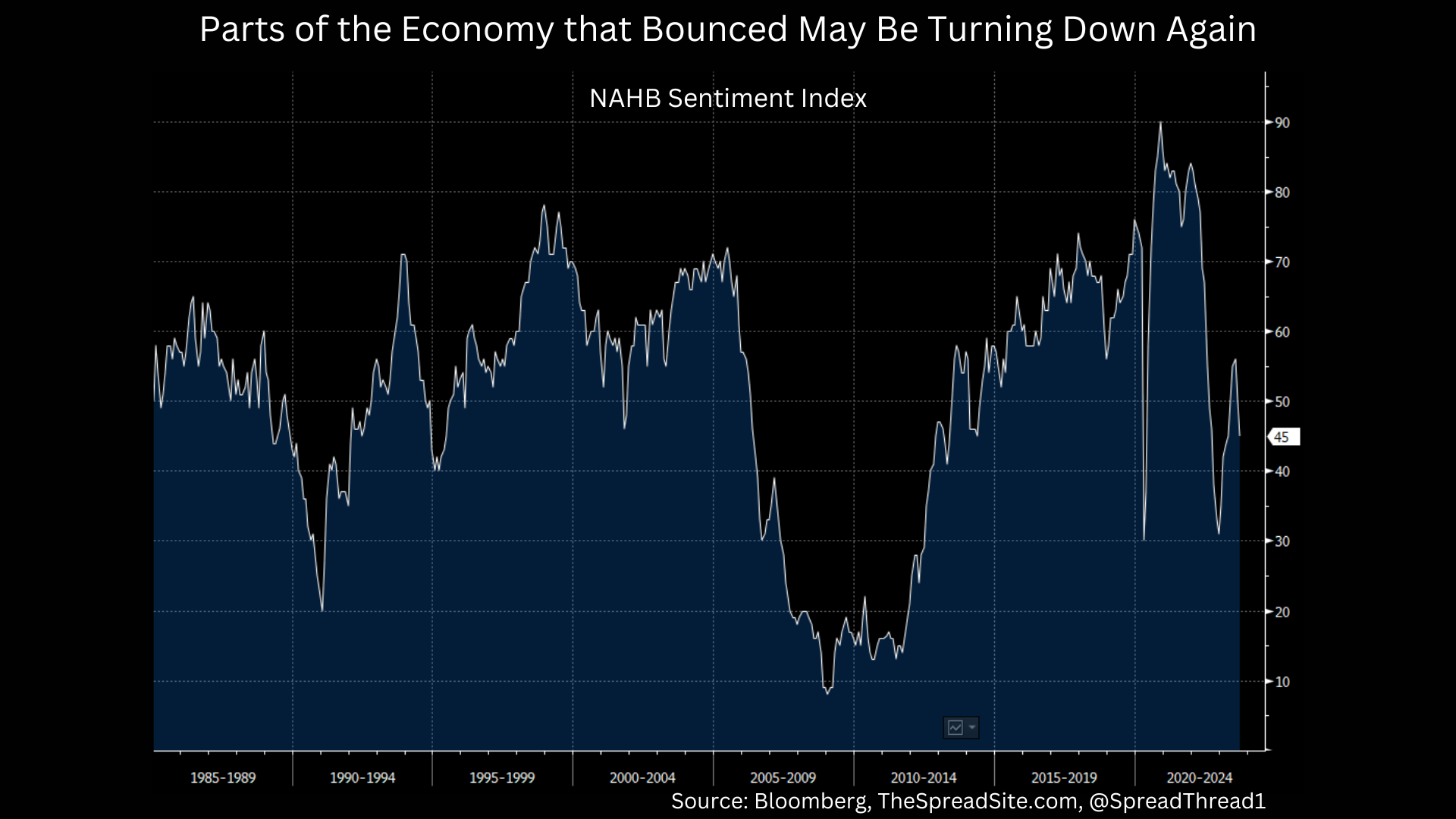

However, the various cross-currents under the surface are more important than moves in the broader indices, in our view. Through the end of July, markets were arguably giving some signs of an earlier-cycle, re-acceleration in the economy. That price action has almost fully reversed. For example, in an early cycle economy where credit is easing and rates are falling, small caps (more economically/ credit sensitive companies) almost always outperform. Small caps looked like they were trying to break out of their long-standing range in late July, but have rolled over, back towards cycle lows.

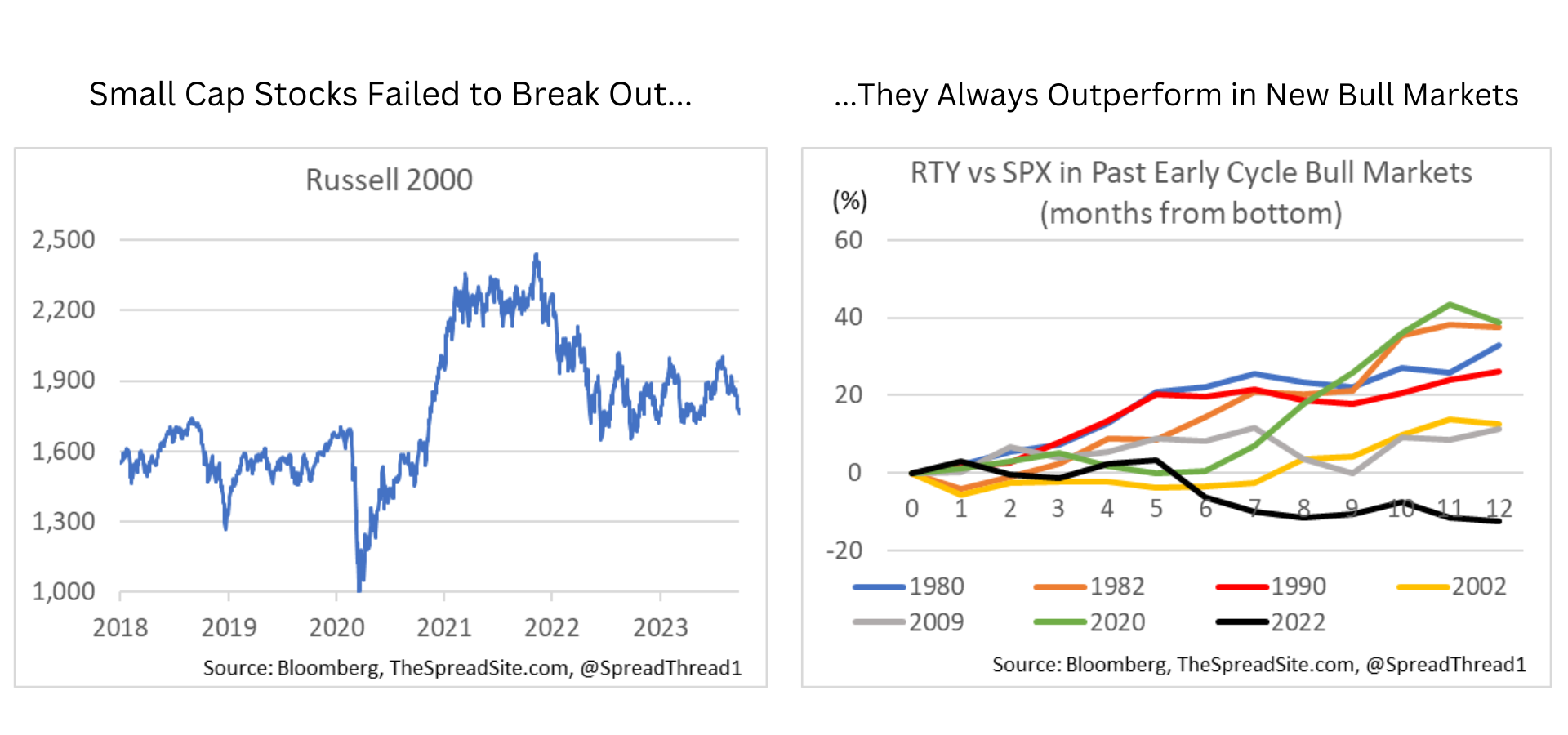

Similarly, most consumer-oriented subsectors also rolled over. XRT, the retail ETF is back near cycle lows, potentially a sign of slowing consumer spending. And note, it’s not just a consumer goods story anymore. Airlines are down 24% since mid-July, and the restaurant sector, which we pitched as a short ~2mo ago (Restaurant Stocks to Face Macro Headwinds) is 16.5% off the highs, all signs the once booming service sector may also be turning.

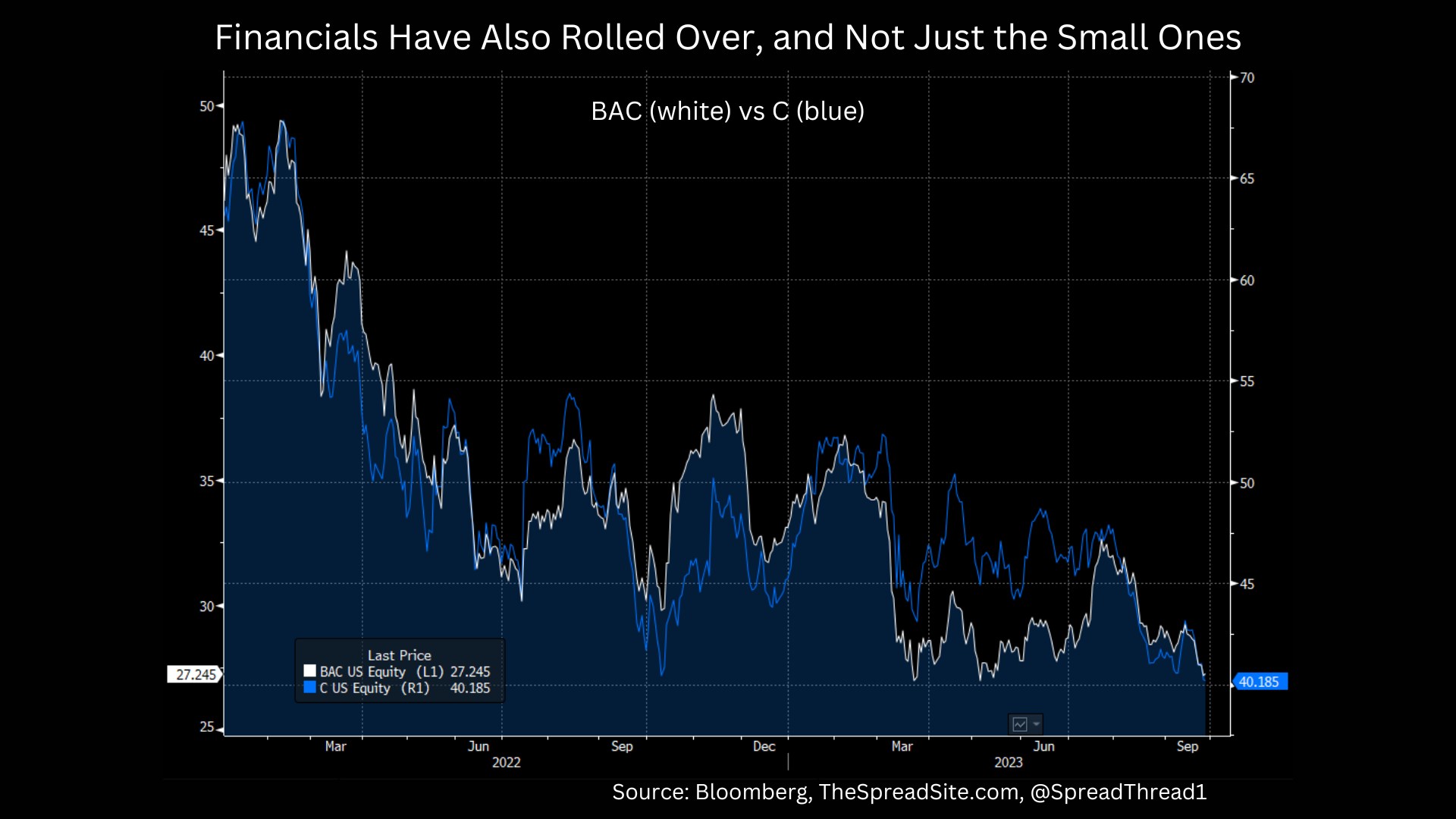

Lastly, we think it is notable that banks are rolling over as well, after staging a modest rally off the March lows. Banks don’t have to lead off the bottom in a new cycle. But recent price action is not a sign of a recovering economy with improving credit. And note, it is not just weaker regional banks or consumer lenders performing poorly. Large banks, like BAC and C, are now sitting at cycle lows.

Adding everything up, we think markets are giving a clear late-cycle message. Energy is leading, with the recent rise in oil prices. And, in fact, a pop in oil late in a cycle is not abnormal - often the last straw that pushes the consumer over the edge. On the other hand, the parts of the markets most sensitive to weakening credit, rising rates, and a slowing consumer, have clearly turned down.

Unlike some of the volatility in stocks, corporate credit markets have been more subdued, with spreads widening only modestly since the recent tights. However, digging in, we think dynamics in credit are quite similar to stocks. In other words, prices are dropping, with all-in yields (in the case of IG) back near cycle highs. However, the price decline has been driven by rising rates, not by widening risk premium (i.e., wider spreads), as we show below on the left. In equities, the story is the same, arguably even more extreme. Prices have fallen, but because rates have risen materially, the equity risk premium has actually declined (right chart below). Said another way, the equity decline has also come from rising rates, not from cheapening relative valuations.

What Now?

Stocks and Treasuries are both oversold and could stage a small bounce, to state the obvious. But more importantly, we think markets are at an important crossroads. Was this pullback just that - a correction in a new bull market? Or is it a resumption of the bear market that began in early 2022? Our view is the latter, but it won’t be that simple.

To begin with, at 4600 on the S&P 500, investors were not paid to bet on a soft landing. However, below 4300, if you are still in the soft landing camp, it makes sense to take some shots, especially in the more beat up cyclical parts of the market. We have been very vocal on our view that this Fed tightening cycle ends in a hard landing. But we’ve also argued the path to get there will be slow and frustrating for bulls and bears alike – with many sharp swings in sentiment along the way. If our endgame is right, at the very least we believe markets will ultimately retest the low (in price) and wides (in spread) from 2022. As discussed earlier, some markets (i.e., smaller cap companies) are nearly already there.

We maintain our conviction in this call for the following reasons. 1) We think credit stress is building under the surface everywhere (corporate, consumer, CRE) and this is while unemployment is still low and fiscal support has been ample. That should tell you something about the vulnerability of many pockets of this economy. 2) Treasury yields are gapping higher, and financial conditions are again tightening, which should put added pressure on levered borrowers, as well as raise the hurdle for new spending/investment. And 3) we believe consumers are slowing as are several areas of the economy that bounced off the bottom earlier this summer.

More specifically on markets, clearly stocks can no longer handle further increases in real yields. That said, we continue to believe that the final move lower in this bear market will come when the economic data cracks, especially jobs, and the Fed is slow to react. That last move lower will be the markets way of forcing the Fed to respond, which they will eventually do, setting up the stage for an actual early-cycle recovery. And unlike the current pullback, the final selloff, in our view, will come from risk premium widening, i.e., underperformance of stocks and credit vs Treasuries.

A Few Words on Positioning

First, we argued a few times recently that there is relative value in Treasury bonds. We have not taken a view on whether bond yields have peaked. Nothing has changed from us on this front. Our issue is that many investors are making the case that even at current levels, bonds are still not cheap. Our follow-up question, “ok, but what then do you buy?” In other words, we understand the view from the higher-for-longer camp that bonds don’t offer enough value in absolute terms, but we have yet to hear a compelling argument that bonds do not offer enough value vs riskier asset classes. For those who are deciding where to put their marginal dollar, and are maxed out on cash, we continue to believe Treasuries > Credit > Equities longer-term. Treasuries may be rich in absolute terms (not our view) but risk assets are richer.

Second, despite our cautious view, we have covered some of our shorts, just in the name of profit taking, while looking to re-engage if markets bounce. For example, we covered the restaurant short (cited earlier in this note), down 13% since our publication.

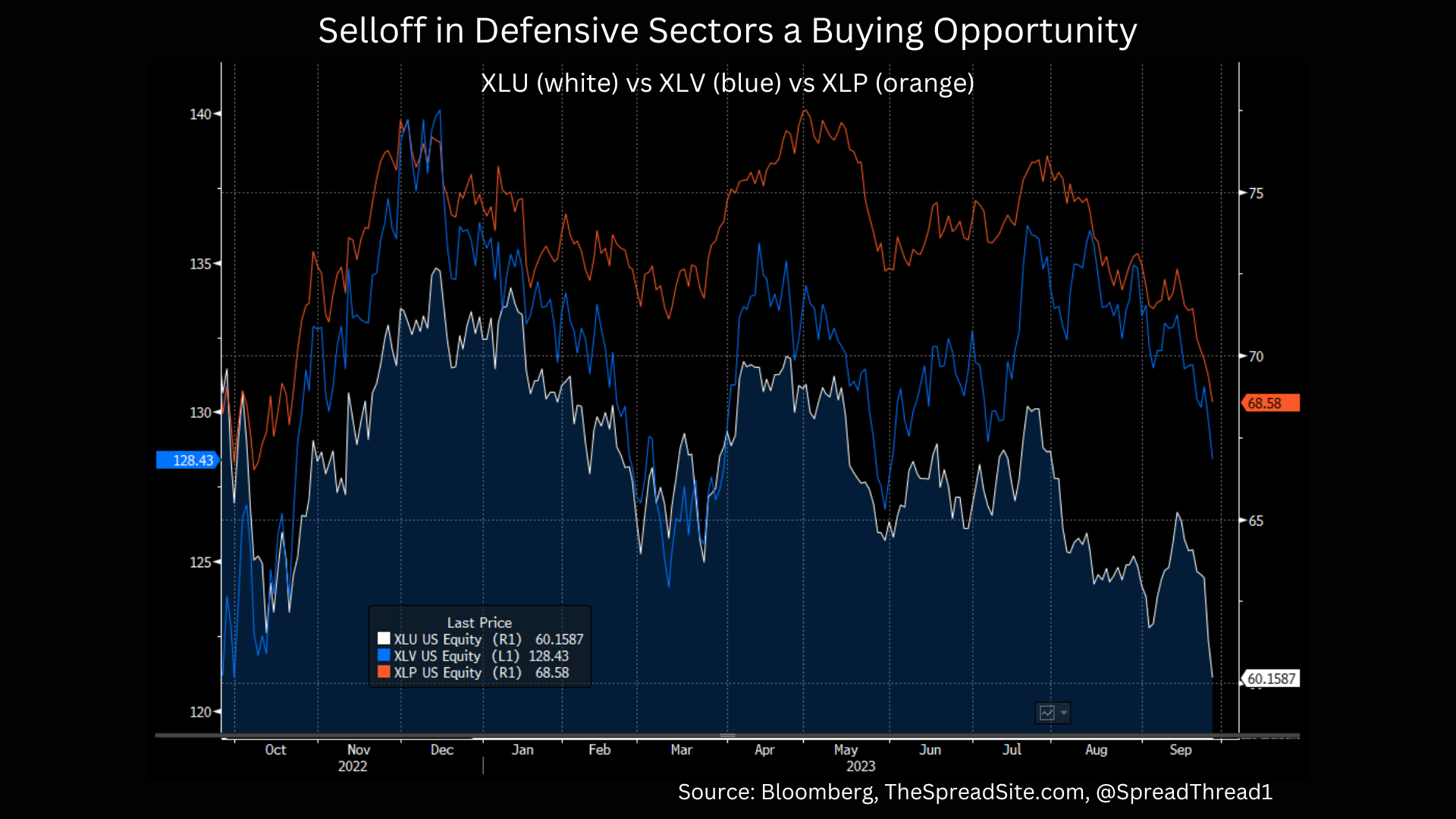

Finally, defensive sectors have sold off with the market, in part given their interest rate sensitivity. That is an opportunity, in our view. We think now is a good time to add some Utilities, Consumer Staples and Healthcare, preparing for a tougher economy over the next six months.

Disclosures

Please click here to see our standard Legal Disclosures

The Spread Site Research

Receive our latest publications directly to your inbox. Its Free!.

{kind=link}