The Lesser Evil

Summary

-

For this selloff to become more than just a pullback, the narrative needs to break one way or another – accelerating inflation, or recessionary data. Rising Treasury yields are clearly a short-term risk. But we think weak data, including jobs, will be the ultimate factor that turns a small pullback into a bigger one.

-

The economy is in an unsustainable equilibrium - those who don’t need to borrow or with locked in low-cost debt are ok for now. As time passes, higher debt costs will touch a greater percentage of the economy - slowly, if financial conditions remain easy, or quickly, if credit markets again stall.

-

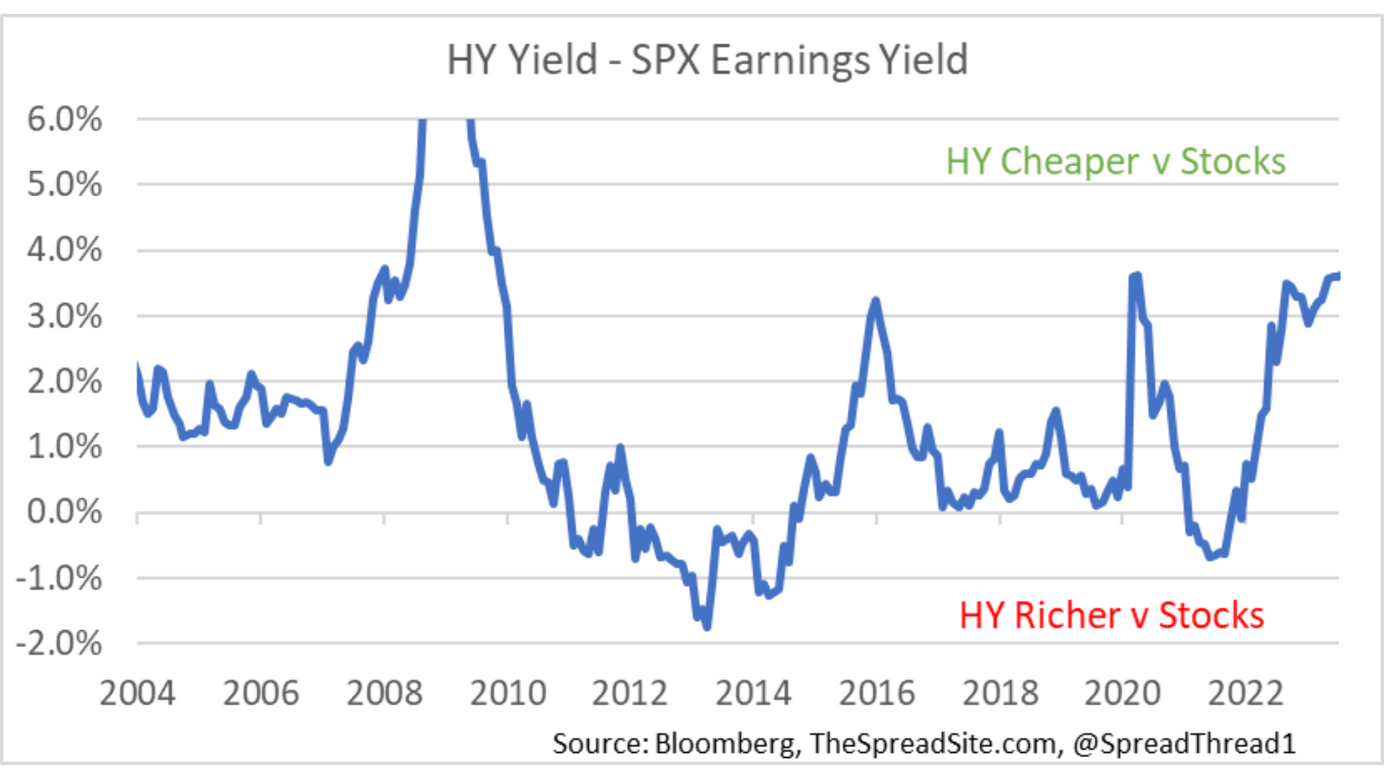

We remain cautious on credit and think spreads are way too tight. In fact, loss-adjusted HY spreads are approaching zero. But given how much equities have rallied this year, and the resulting valuation, we believe credit offers better RELATIVE risk/reward than equities.

-

The modest value in credit yields is coming from elevated Treasury yields, not spreads. While we respect the weak technicals in rates, we believe the demand for long duration fixed income at current yields or higher, will be substantial medium term, especially if the alternatives remain as rich as they are today.

Updated Market Thoughts

Markets are finally seeing modest volatility after months of a slow, steady grind higher, with the SPX now ~3% off its YTD high. While higher Treasury yields are likely the main culprit, the ‘Goldilocks’ narrative of a strong labor market and falling inflation is still mostly going strong. For this selloff to become more than just a modest positioning-led pullback, the narrative needs to break decisively in one direction or another – either accelerating inflation, or recessionary macro data.

The former seems less likely in the immediate term, after two consecutive benign CPI reports. It is certainly possible that despite this softer inflation data, long-end bond yields keep rising given accelerating growth expectations (if the Atlanta Fed 3Q GDP estimate of ~4% is anywhere close to correct – consider us skeptical), rising oil prices, and substantial Treasury supply. However, for bond yields to really break the market, we think the move needs to be significant.

We remain in the camp that recessionary data, including jobs, will be the ultimate factor that turns a small pullback into a bigger one. And while we continue to avoid getting overly precise on timing (which has helped us stay above water in 2023 – despite a cautious medium-term view) we think many signs point to sooner rather than later. To provide a few examples:

• Global data is weak and is arguably weakening – i.e., Europe and China.

• Cracks are finally forming in the service side of the economy, such as declining restaurant foot traffic and reports of weaker domestic air travel, as we discussed last week (Restaurant Stocks to Face Macro Headwinds)

• The job market is clearly slowing, and we think the slowdown may be greater than the headline numbers suggest. As ZipRecruiter noted, “The ongoing trend of reduced demand for recruiting services continues, and we believe this is a reality that companies across the recruiting category are facing.”

• Consumer headwinds are growing, in our view, most importantly the repayment of student loans scheduled to hit October 1st.

• Falling inflation is a double-edged sword. It could mean a soft landing. But it also means reduced pricing power and higher real rates, assuming the Fed holds policy steady.

Ultimately, time is on our side. The economy right now works for those who do not need to borrow or those with locked in low-cost debt. Consumers who bought a house pre-2022 are likely fine. Companies with a high percentage of fixed rate debt are also likely okay. But many cannot survive if their balance sheets are refinanced at current debt costs. And a large amount of new spending that must be financed (homes, auto purchases, corporate capex, etc…) is now less viable. That is an unsustainable equilibrium. And it WILL serve as a headwind to growth as higher debt costs touch a greater percentage of the economy – either slowly, if financial conditions remain easy, or quickly, if they tighten and credit markets again stall.

Positioning: HY vs Stocks

With these views in mind, we remain cautious on credit and think spreads are way too tight for the macro backdrop that we envision over the next year. But given how much equities have rallied this year, and the resulting valuation, we believe credit offers better RELATIVE risk/reward than equities, for investors primarily focused on total return (as opposed to excess return or spread changes).

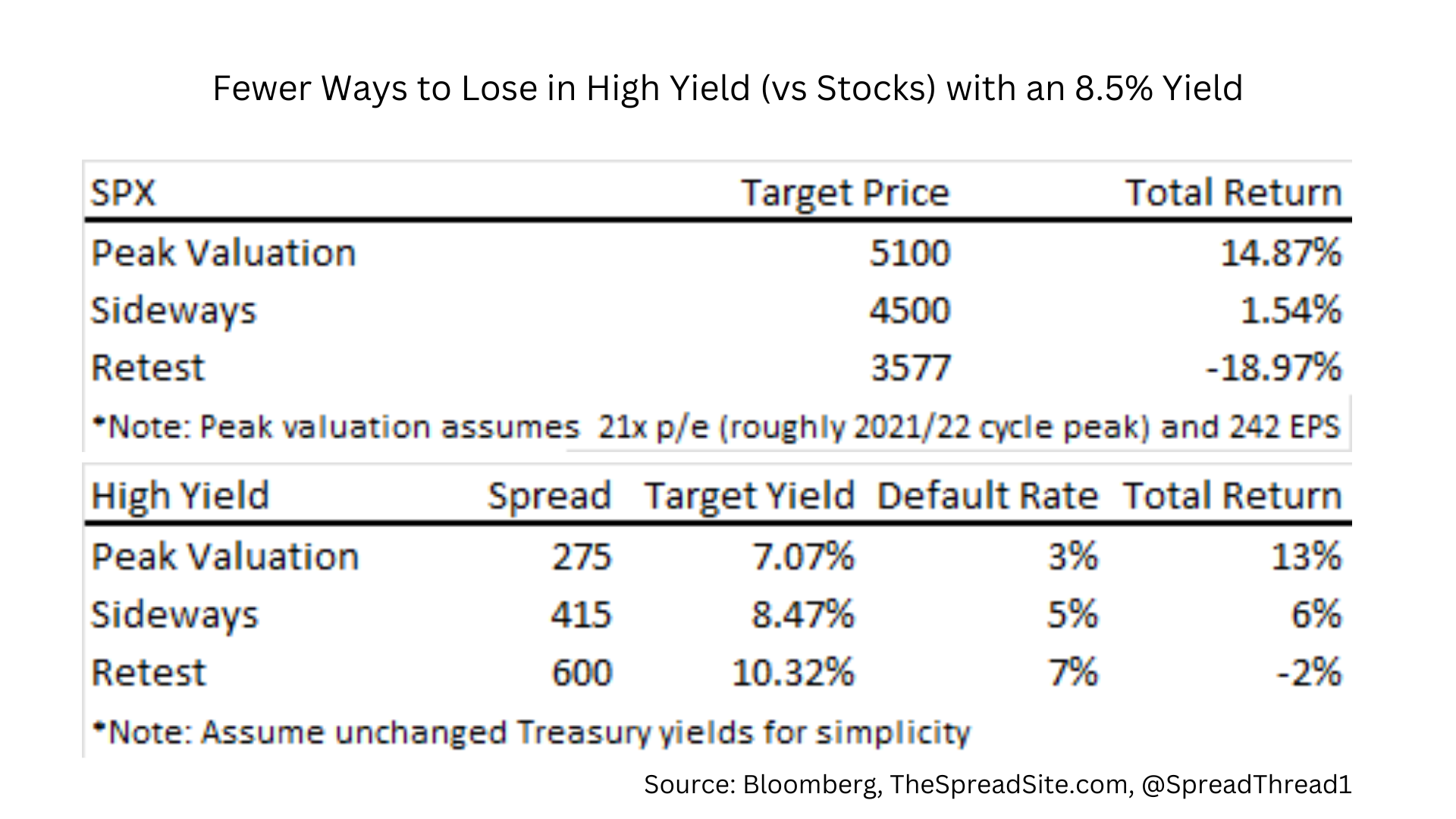

For example, below, we show rough returns for equities and high yield credit in three scenarios, assuming a one-year holding period. (note: for simplicity, we assume unchanged base rates).

- In “Peak Valuation,” we assume stocks hit a 21x p/e multiple (roughly the multiple when the SPX peaked in 2021/22) on 2024 EPS estimates. Similarly we assume high yield hits prior cycle tights in spreads (275bp) and a fairly low default rate. In this scenario we get a ~15% return for the SPX and a 13% return for high yield.

- In “Sideways” we assume markets chop around for the next year with stocks and credit spreads unchanged, and a default rate roughly consistent with what Moody’s is forecasting a year from now. This scenario leads to an SPX return of 1.5% and a HY return of 6%.

- In “Retest” we assume stocks and credit spreads retest the 2022 lows/wides and a 7% default rate. This leads to a -19% return in the SPX and -2% in high yield.

Of course, these scenarios are overly simplistic, and obviously it can get a lot worse for either asset class in the bear case. Plus this analysis assumes a one-year holding period, when carry becomes a bigger factor. But our simple point is to show that given an 8.5% starting yield vs very rich equity valuations, high yield likely outperforms in both a sideways market or in the bear case by quite a bit. You need to bank on a dot-com-like melt-up to expect materially better equity returns going forward. (Sidenote: The historical beta between HY and SPX returns is about 0.5x, so HY should outperform in a selloff and underperform in a rally, if the historical relationship holds).

And although not the point of this report, we also think there is a growing long-term fundamental case for credit over equities. Very simply, with the all-in cost of debt having risen as much as it has (as well as tighter credit conditions) companies now have the incentive to reduce leverage. This is the exact opposite of the past decade, where companies were incentivized to reward equity at the expense of credit – by issuing cheap debt to buyback stock or levering up balance sheets in other ways (i.e., M&A/LBOs, etc…).

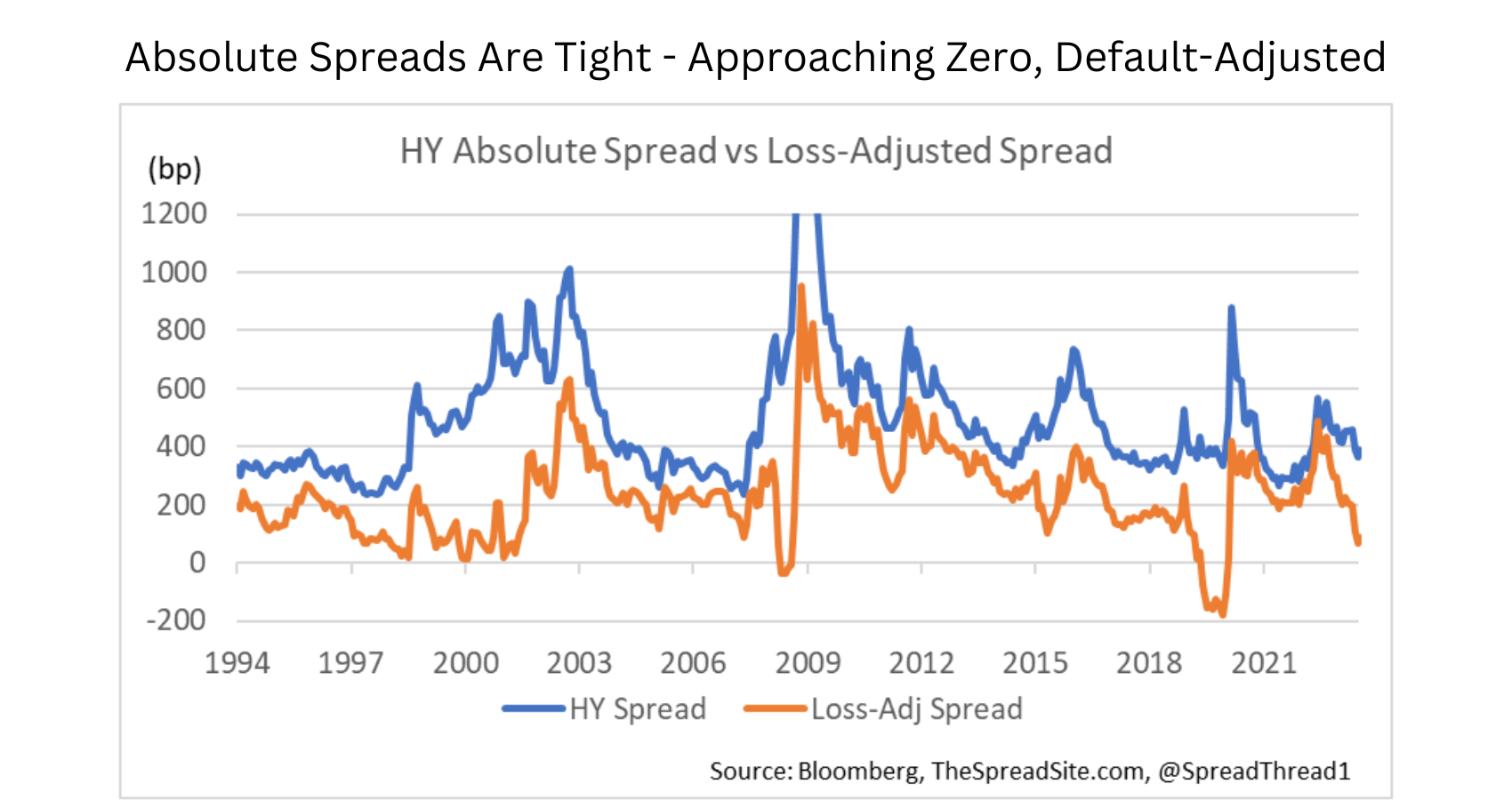

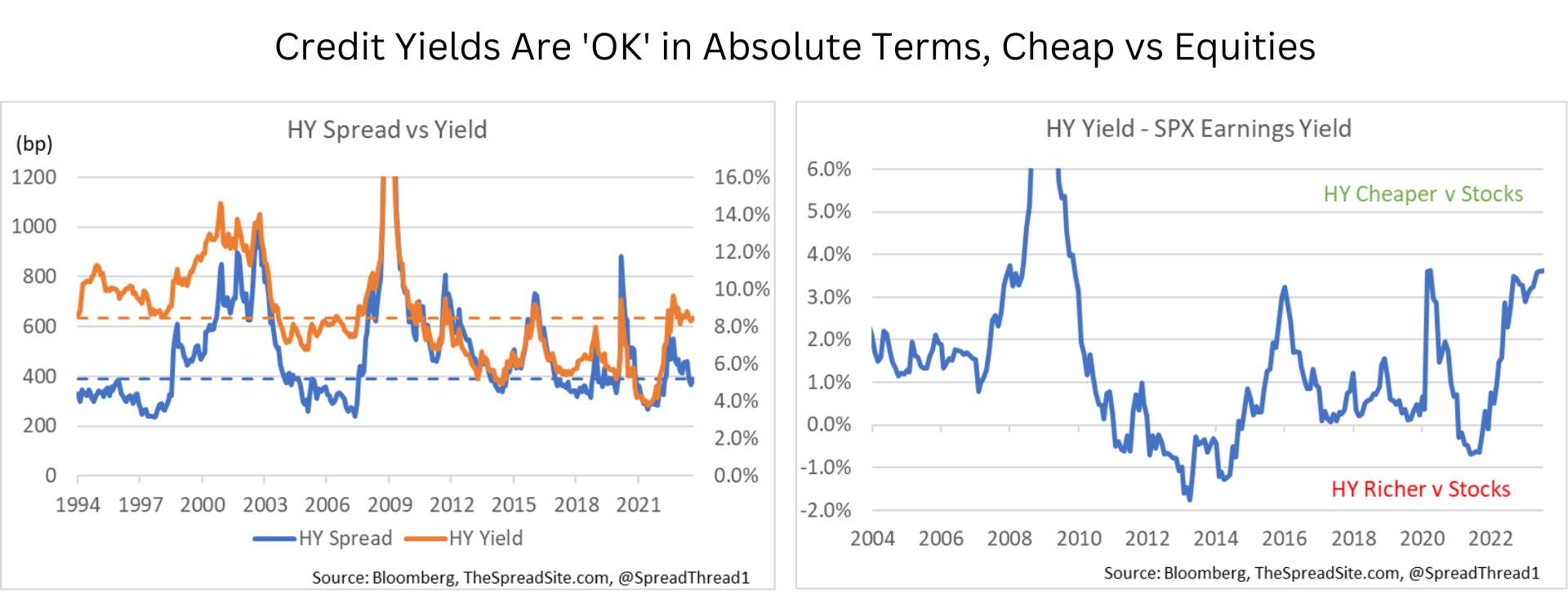

With that said, credit spreads are far from attractive in absolute terms. High yield spreads are now only ~125bp above 2021 tights. And if we assume spreads today are in part compensating you for defaults over the next year, and we plug in a 5% default rate (Moody’s forecast), loss-adjusted spreads are approaching zero, as we show in the chart below.

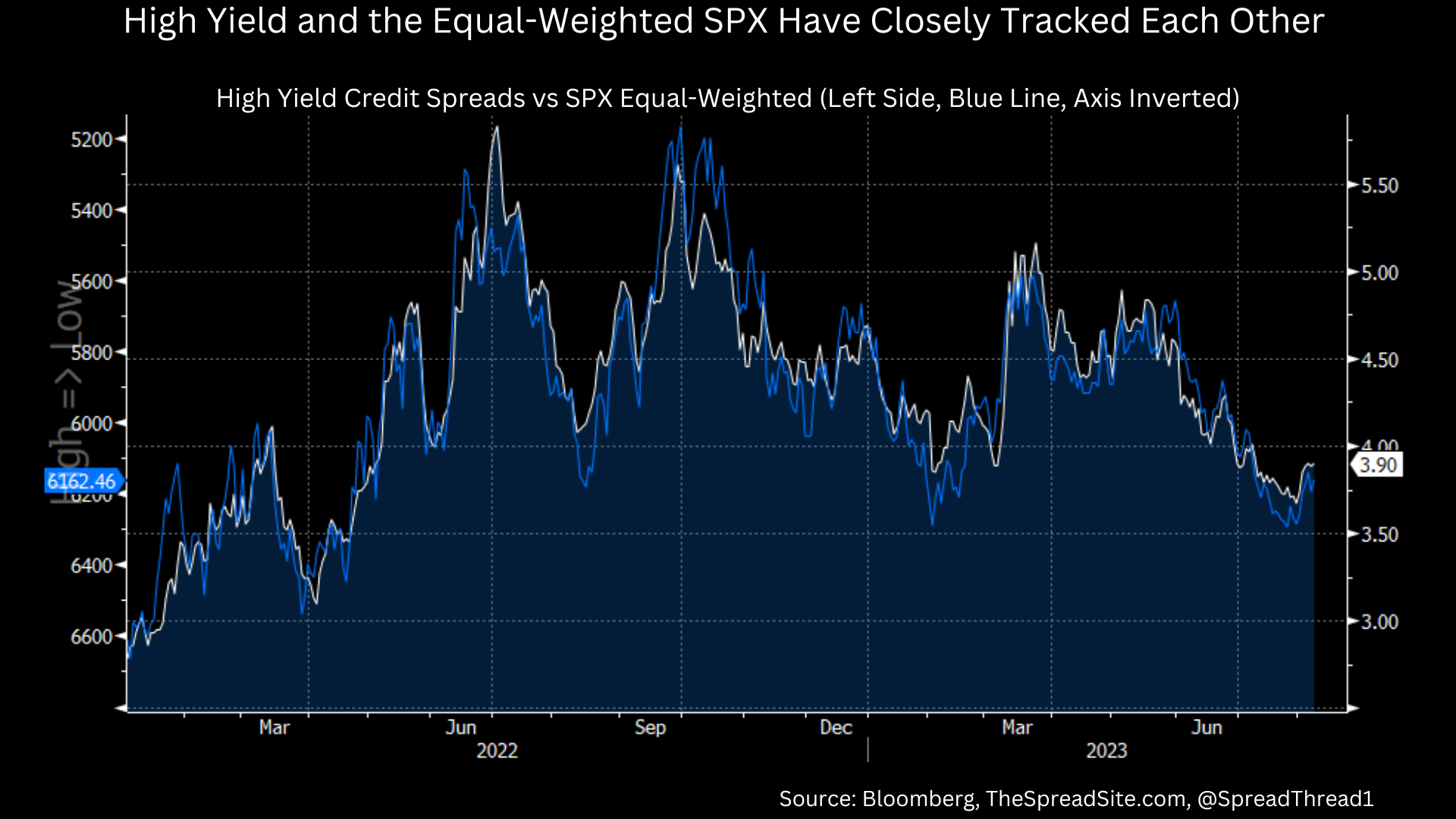

In fact, high yield spreads have been tracking the S&P 500 equal-weighted index fairly closely over the past few years. The compression in risk premium has not been unique to one asset class or the other.

Adding it up, spreads are very tight, but all-in yields in credit are reasonable, as we show below (left chart). They are far from pound-the-table cheap, but in a world where equity yields are very low, the RELATIVE value is becoming more notable (right chart).

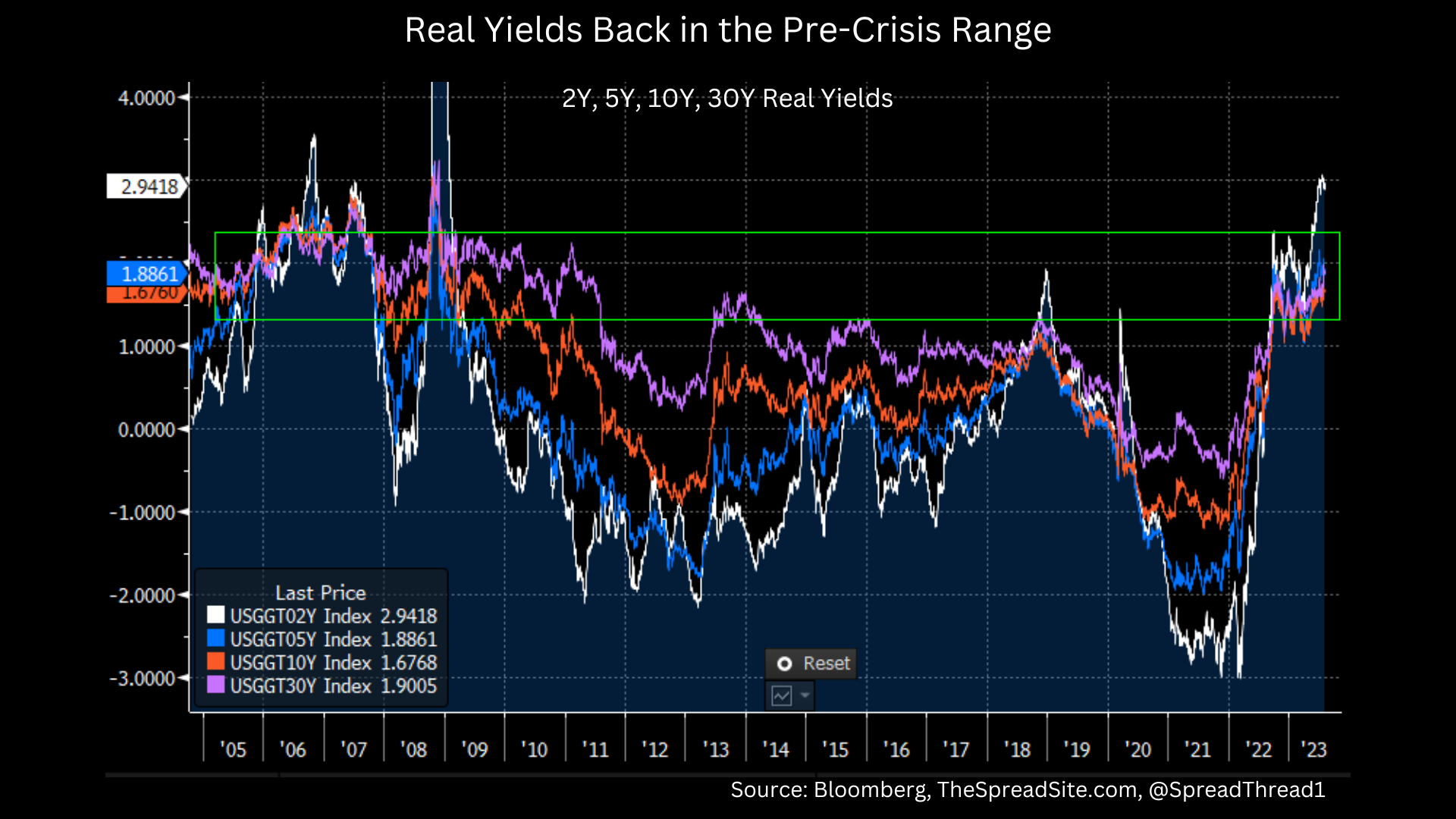

However, once again, the value in those yields is coming from elevated Treasury yields, in particular, elevated real yields, not from attractive credit spreads.

And yes, we understand that term premium is low, cuts are priced into the curve in 2024, and all the other arguments for higher Treasury yields going forward. But for longer-term investors that can’t simply sit in cash, it is hard to find too many asset classes that both look reasonably valued vs recent history and offer upside if the economy disappoints, as we expect. And so while we are respecting the technicals, as well as other recent drivers of higher bond yields, we are adding on pullbacks. In our view, the demand for long duration fixed income at current yields or higher, from the many investors who NEED yield, will be substantial, especially if the alternatives remain as richly valued as they are today. In short, our broad asset class preference over the next 6-12 months is Treasury bonds > Credit > Stocks.

Disclosures

Please click here to see our standard legal disclosures

The Spread Site Research

Receive our latest publications directly to your inbox. Its Free!.

{kind=link}